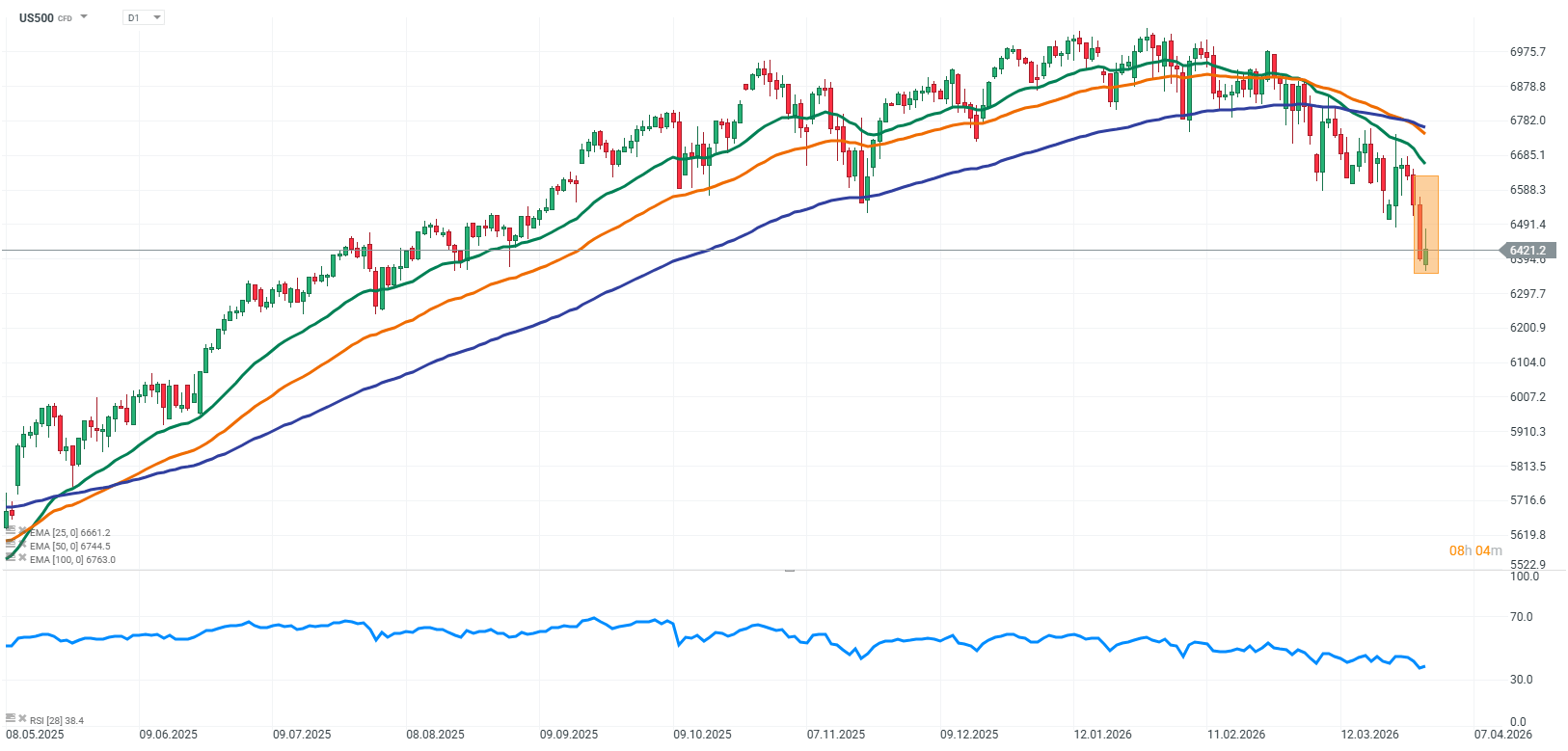

Wall Street is starting the new week on a clearly positive note. Major indexes are rising, and risk appetite is slowly returning after last week’s correction. There is a sense of relief after the weekend, as the conflict in the Middle East did not escalate further, although the situation in the region remains tense and uncertain.

Positive sentiment has been partly supported by comments from former President Donald Trump, who stated that negotiations with Iran are progressing well and that reaching an agreement is possible. At the same time, it is clear that the talks are still far from a breakthrough. Iran officially denies engaging in direct negotiations with the US, and key points of disagreement remain unresolved. While the market feels a temporary sense of relief, the potential for sudden changes and geopolitical risk remains high.

The threat of a possible ground operation still looms. US military forces are considering various scenarios, and Iran has declared its readiness to respond to any potential attack. This context keeps markets cautious regarding tensions around the Persian Gulf, and any new developments from the region could immediately influence market sentiment and index fluctuations.

The commodities market remains under geopolitical pressure. Brent crude is hovering around $110 per barrel, with energy prices reacting not only to current tensions but also to concerns about future supply and stability. Volatility in commodities highlights how strongly global events can impact asset valuations and overall market sentiment.

Another key focus today is the scheduled speech by Fed Chair Jerome Powell at 4:30 PM. Markets will be closely analyzing every word for insights on inflation outlooks and potential interest rate decisions. In the current environment, where economic growth and inflation control create a difficult dilemma, Powell’s remarks could set the tone for the entire week on Wall Street.

Today’s rebound in the indexes shows that the market can respond to a brief pause in tension, even as global fundamentals remain uncertain.

Source: xStation5

US500 (S&P 500) futures are rising strongly today, supported by improving sentiment amid prospects for stabilization in the Middle East. Market optimism is fueled by reports of ongoing talks between the US and Iran, which, although still far from a breakthrough, give some reason to hope for easing tensions in the region.

Source: xStation5

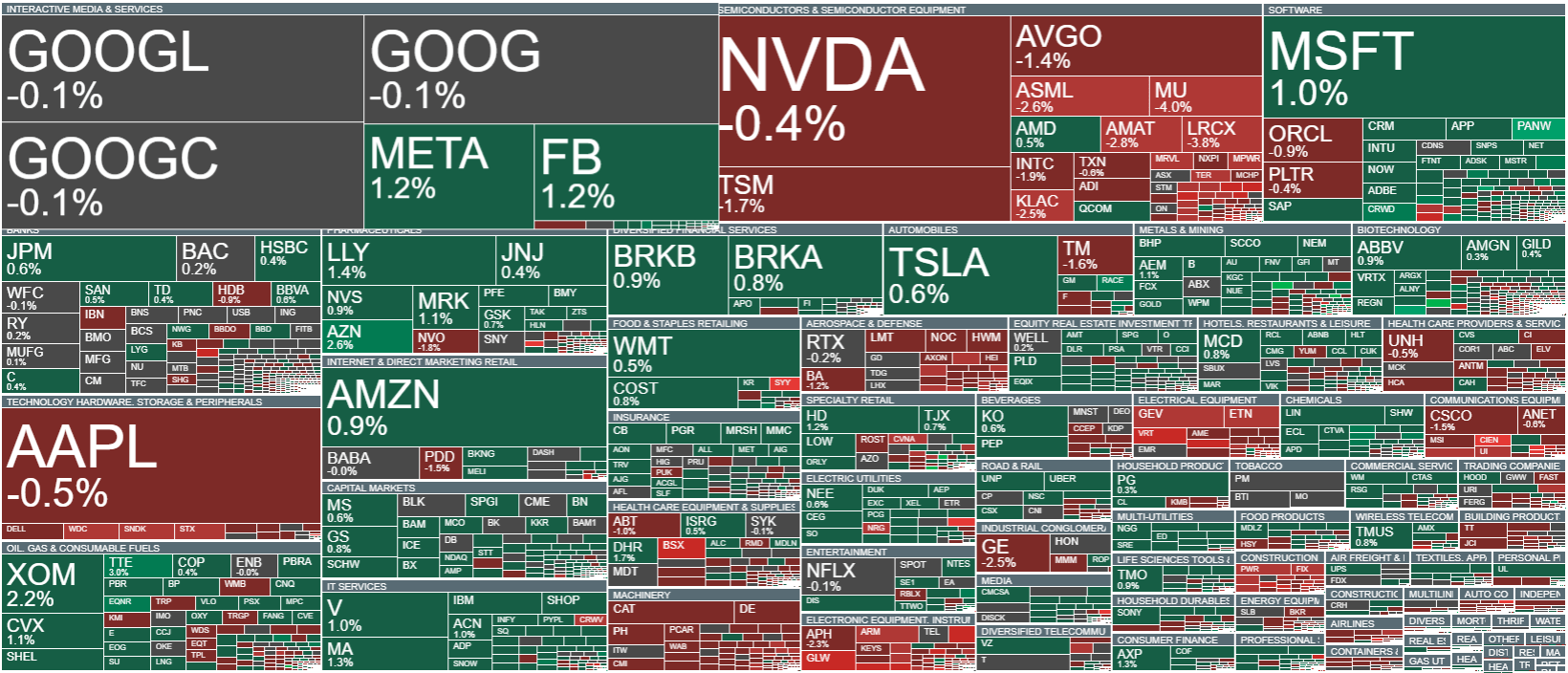

Company News

CrowdStrike (CRWD.US) shares are climbing today after an upgrade in the company’s rating. Analysts note that the upcoming AI model from Anthropic could boost demand for cybersecurity services and revenue growth. The move upward reflects expectations that AI development will increase demand for advanced protection tools.

Sysco (SYY.US) shares are down more than 10% today following the announcement of the Jetro Restaurant Depot acquisition. The deal is valued at $29.1 billion, with Jetro shareholders set to receive $21.6 billion in cash and 91.5 million Sysco shares. The drop reflects the high cost of the acquisition and potential challenges in integrating the two companies.

Palo Alto Networks (PANW.US) shares are rising in response to comments from the CEO emphasizing the need to use AI to combat cyber threats as frontier models expand. The remarks suggest the company may increase its focus on AI-based solutions, strengthening its position in the cybersecurity sector and improving growth prospects.

MicroStrategy (MSTR.US) reported that it did not purchase any bitcoin last week, which may indicate a temporary pause in demand or increased caution amid cryptocurrency market volatility. The lack of new purchases suggests that institutional players are holding back from expanding BTC positions.

AMD Did Everything Right… But Only Right

SpaceX Shares Drop 6% After Earnings 🚩 Is Space No Longer Enough for Wall Street?

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%