Thursday’s session begins amid a flood of important information, both from financial markets and the political world. Futures on the main U.S. indices ahead of the open point to significant uncertainty, but also moderate optimism. US2000 is gaining the most, up around 0.4%.

Despite a series of important market updates, the conflict and negotiations between the U.S. and Iran remain in focus. The situation is changing hour by hour. Despite a number of compromises being worked out, the status of key issues - stockpiles of enriched uranium and control over the Strait of Hormuz - remains unclear. Iran’s “Supreme Leader” reportedly personally forbade any attempts to hand over accumulated fissile materials.

SpaceX released its long-awaited IPO prospectus. Investors are excited, but many questions are emerging regarding the figures and statements included in the document.

Diplomatic messages from Iran and a series of new strikes on refineries in Russia are pushing oil prices higher. Brent is moving above $108 per barrel.

Macroeconomic data:

- The Philadelphia Fed index collapsed, falling to -0.4 versus expectations of 18.2, pointing to very weak business sentiment in one of the most important U.S. states.

- Building permits rose above expectations, reaching 1.44 million, which may indicate improving sentiment in the construction sector and rising investment nationwide.

- Jobless claims came in slightly below expectations of 210k, at 209k.

- PMI indices showed surprisingly strong momentum in U.S. manufacturing, with a reading above 55. Services, however, were weaker than expected, with the index falling to 50.9 points.

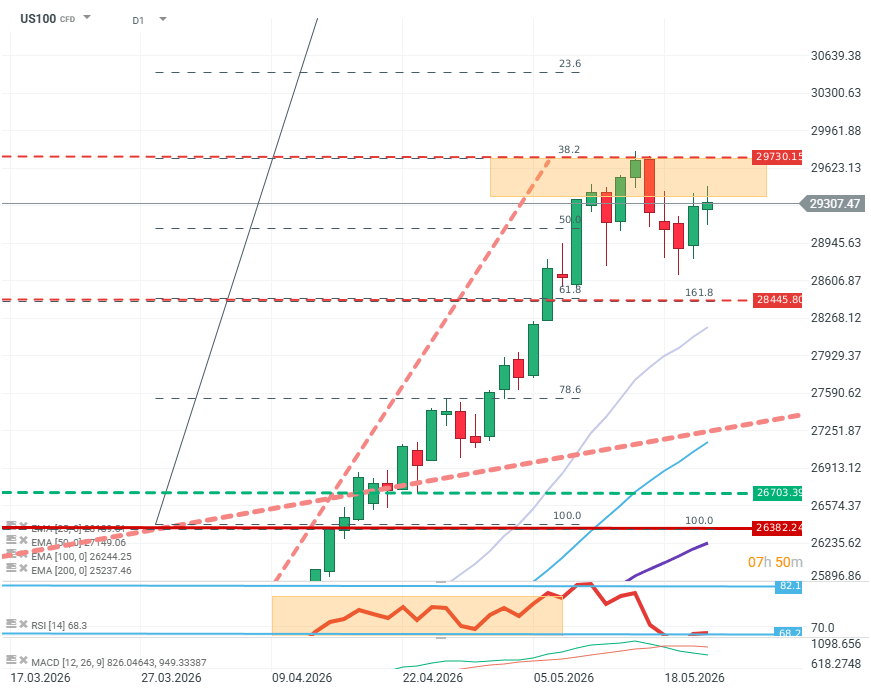

US100 (D1)

Buyers are trying to regain the initiative, retracing recent declines and attempting to return to the level of the last peak. The EMA averages maintain strong upward momentum, while RSI has dropped significantly but remains close to “overbought” levels. MACD, however, is sending a bearish signal. If sellers were to dominate direction on the index, the first target would be the 61.8% Fibonacci level (28,445). Source: xStation5

Company news:

- IBM (IBM.US): The stock is up about 4% at the open after it was made public that the company will receive around $1 billion in grants from the Department of Commerce to develop quantum computing technology. Smaller names such as Rigetti and D-Wave are also benefiting from the “quantum” spending wave, rising by double-digit percentages.

- Deere & Co. (DE.US): The farm machinery maker is down about 3% at the open despite excellent results, well above expectations. Investor pessimism stems from the company keeping its profit outlook for the current year unchanged despite improved profitability.

- Walmart (WMT.US): The largest supermarket chain in the U.S. is down about 2% after earnings, driven by EPS coming in below expectations.

- Intuit (INTU.US): The stock is plunging after earnings. The company plans to lay off 17% of its workforce while reporting results above expectations for both EPS and revenue. The share price is down about 20%. The main drivers are worse-than-expected results in selected business segments and negative sentiment toward SaaS stocks.

- Nvidia (NVDA.US): The world’s largest company and a leader among graphics card makers released another set of results that beat expectations. However, higher profitability and revenue did not translate into higher valuations, which may suggest the results were already priced in.

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound