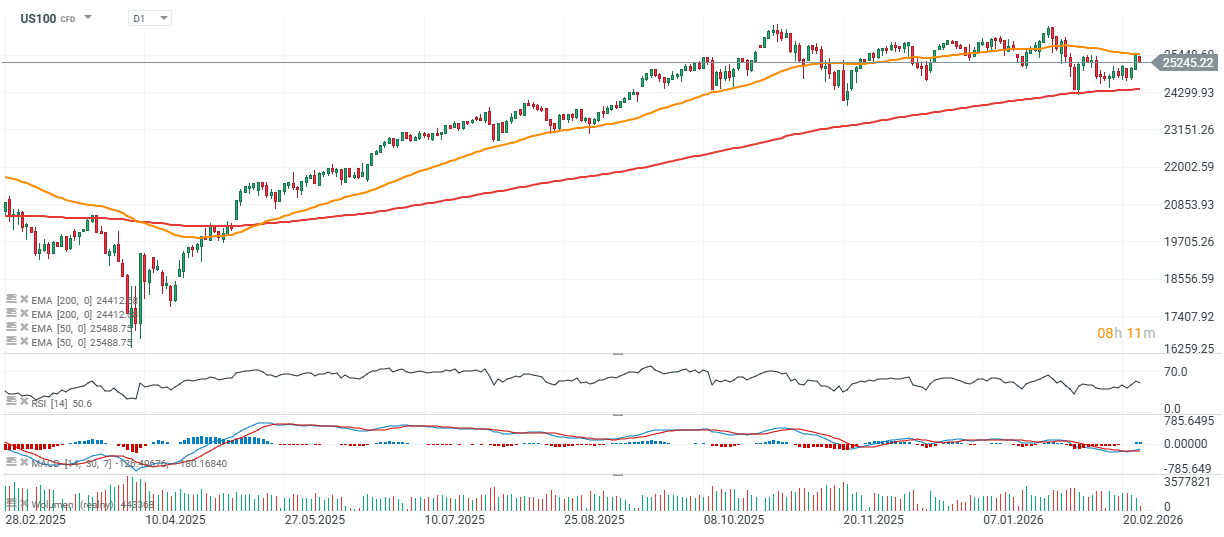

Wall Street sentiment is softening today, with the cash Nasdaq 100 down 0.7% and the S&P 500 slipping 0.3%, despite Nvidia’s record-breaking quarter released yesterday and the company’s very optimistic forward guidance. The Dow Jones Industrial Average and the Russell 2000 are outperforming slightly, both trading in a 0.15%–0.3% range. Initial jobless claims in the U.S. edged higher last week but remain within a historically low range, suggesting employers are still refraining from significant layoffs despite slower hiring momentum.

Seasonally adjusted initial claims totaled 212,000 for the week ending February 21, up 4,000 from the prior week’s upwardly revised reading but below the Dow Jones consensus of 215,000. The four-week moving average increased by just 750 to 220,250. Continuing claims, reported with a one-week lag, fell by 31,000 to 1.833 million. The data point to a likely extended pause in Fed policy easing. A more than 3% drop in Nvidia shares is weighing on broader market sentiment, while aerospace and defense company Heico (HEI.US) is down nearly 13%.

US100 (D1 interval)

Nvidia shares are losing momentum despite a strong quarterly report and robust expectations for the current quarter, falling below $190 per share.

Source: xStation5

Source: xStation5

Problems at Heico?

Shares of aerospace and defense company Heico (HEI.US) fell more than 12% following its earnings release, even though the company reported record first-quarter profit and maintained double-digit revenue growth. It is a classic case of “buy the rumor, sell the fact”: investors may have expected an even stronger margin profile, with attention shifting to product mix in the Electronic Technologies segment and higher financial leverage following a recent acquisition.

- Heico is a Florida-based family-controlled company that has spent decades acquiring healthy, profitable niche businesses in electronics and aircraft equipment (safety systems, cockpit components, etc.). It is now one of the largest providers of aftermarket replacement parts and repair services for commercial airlines, while also expanding into defense and space contracts. Given its secure supply chains and key role in domestic manufacturing, the company appears well positioned to benefit from ongoing industrial demand and its strong competitive position.

- Headline results were solid. Revenue rose 14% year over year to $1.18 billion, broadly in line with consensus, while diluted EPS came in at $1.35 versus $1.29 expected and about 13% higher than a year earlier. EBITDA increased 14% to $312 million, and operating income reached $259.9 million. Operating cash flow declined to $178.6 million, partly due to compensation-related distributions.

The Flight Support Group (FSG), closely tied to the civil aviation cycle and rising maintenance activity, remains the key growth driver. The segment delivered strong revenue growth and improved profitability. In contrast, the Electronic Technologies Group (ETG) grew sales but saw margin pressure due to a less favorable product mix, including weaker space-related sales and a softer defense mix. That margin compression likely tempered investor enthusiasm despite the EPS beat.

Key figures:

- Revenue: $1.18 billion, +14% YoY

- Net income: $190.2 million (quarterly record)

- Diluted EPS: $1.35 vs $1.29 expected

- EBITDA: $312 million, +14% YoY

- Operating cash flow: $178.6 million

Flight Support Group (FSG)

Revenue: $820 million, +15% YoY

- Organic growth: ~12%

- Operating income: $200.7 million, +21% YoY

- Operating margin: 24.5%

Electronic Technologies Group (ETG)

Revenue: $370.7 million, +12% YoY

- Organic growth: ~6%

- Operating income: $73.2 million (slight decline)

- Operating margin: 19.8%

Balance sheet:

Net debt/EBITDA: 1.79x (higher following acquisition)

Management emphasizes that the increase in leverage reflects the recently completed acquisition and remains at a comfortable level. However, markets often reward not just growth, but the quality and sustainability of margins. While FSG continues to shine, ETG’s margin pressure (including a more than 4% YoY decline in segment profit) raises questions about near-term profitability stability. In the coming quarters, the key issues will be whether ETG returns to a more favorable mix—particularly in space and defense—and whether FSG can maintain elevated margins as volumes continue to grow. Management remains optimistic about fiscal 2026, pointing to sustained sales momentum supported by organic demand and acquisitions, though no specific quantitative guidance was provided.

Source: xStation5

Corporate news highlights

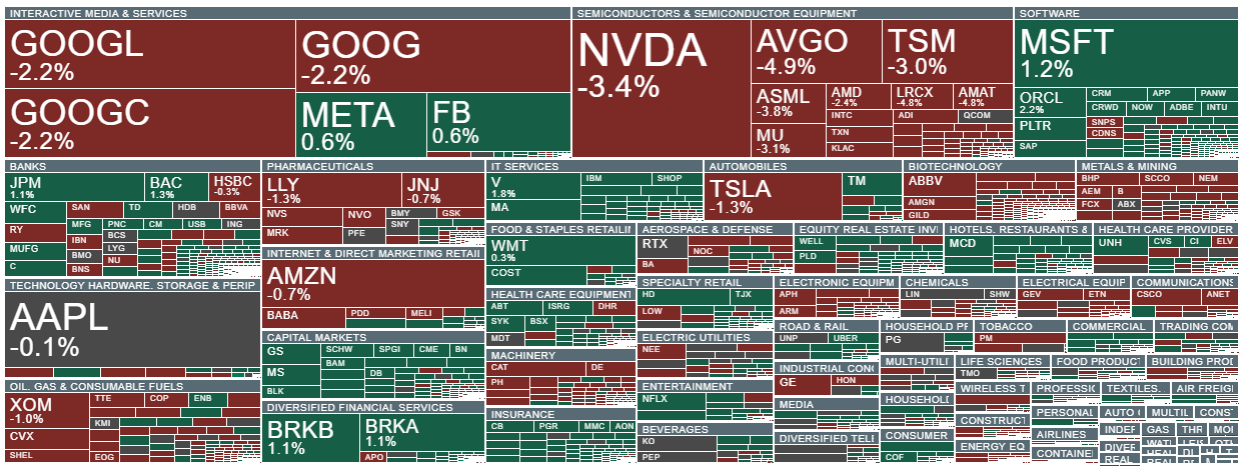

J.M. Smucker is up nearly 5% after posting better-than-expected fiscal third-quarter results, with adjusted EPS of $2.38 on revenue of $2.34 billion versus FactSet consensus of $2.27 and $2.32 billion.

Lantheus Holdings is down almost 5% after issuing weaker-than-expected full-year guidance, forecasting EPS of $5.00–$5.25 versus the $5.51 consensus.

Array (ARRY) plunges 25% after its 2026 adjusted EBITDA guidance missed expectations.

C3.ai (AI) drops more than 25% after cutting full-year revenue guidance below consensus.

Celsius Holdings (CELH) gains 12% after beating fourth-quarter revenue and earnings estimates.

Driven Brands (DRVN) falls 3% after Wednesday’s 30% plunge, as Piper Sandler downgraded the stock following accounting errors requiring restatements and a delayed quarterly report.

GoodRx (GDRX) slides 15% on weak 2026 revenue and EBITDA outlook.

IonQ (IONQ) rises 13% after beating fourth-quarter expectations.

Mosaic (MOS) declines 3% after JPMorgan downgraded the fertilizer producer on cost concerns.

Nubank (NU) drops 5.1% as higher costs and provisions offset net income growth.

Nutanix (NTNX) jumps 15% after AMD announced a $150 million equity investment as part of a new partnership.

Papa John’s (PZZA) falls 3.4% on weaker-than-expected sales amid a challenging consumer backdrop.

Perrigo (PRGO) loses 7.6% after missing profit and margin estimates and issuing disappointing full-year guidance.

Trade Desk (TTD) tumbles 16% on weak first-quarter guidance, heightening concerns over Amazon competition and AI-driven disruption.

Salesforce (CRM) gains 2% after providing moderate but stabilizing sales growth guidance, easing fears of competitive pressure in the AI era.

Source: xStation5

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

Berkshire earnings: What do the reports say about the market’s direction?

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Intel Needs $15 Billion. Is It a Financial Problem or the Price of an Ambitious Expansion?