Sentiment during Friday’s session is clearly more constructive. The VIX volatility index has corrected nearly 10% from its local highs and is down roughly 5% since midnight. US500 futures are up more than 0.7%, while US100 is gaining about 1.3%.

- Asian markets regained stability after early declines on Friday, although investors remained notably cautious toward the technology sector. Amazon shares initially dropped around 11% in US after-hours trading, but the decline has since narrowed to roughly 7%. The company plans to spend $200 billion on artificial intelligence this year and delivered an earnings and revenue outlook that investors found underwhelming.

- Geopolitics also seems to be giving markets some breathing room. The United States continued negotiations with Iran in Oman, and investors are treating the very fact that talks are ongoing as an encouraging signal—reducing aggressive positioning around the risk of a US–Tehran military confrontation.

- On the European front, the Kremlin indicated that recent discussions involving Ukraine and Russia were meaningful and constructive. President Zelensky said the next round of negotiations could take place in the United States, which may suggest the two sides are moving closer to a compromise, maybe at least on one key issue.

US500 and VIX (D1)

S&P 500 futures have pulled back to roughly 100 points below the 50-day EMA (orange line). The drawdown from the highs is still relatively modest, and the index remains about 300 points below record levels.

Source: xStation5

Source: xStation5

US earnings season (FactSet data as of February 4)

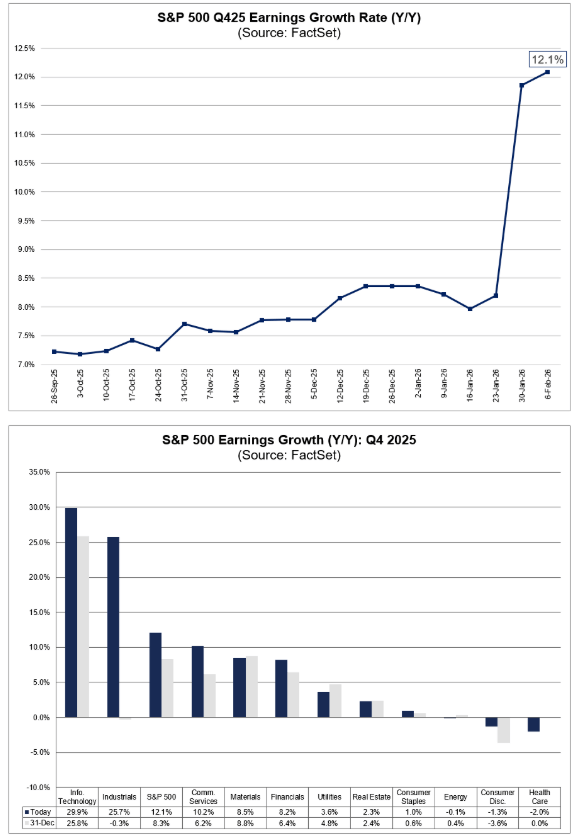

Despite the recent pullback, the S&P 500 is still delivering what typically underpins a bull market: double-digit earnings growth, now on track for a fifth straight quarter (so far). Over the past week alone, blended Q4 EPS growth jumped from 8.2% to 11.9%. If that figure holds, it would mark the first time since Q4 2017–Q4 2018 that the index has posted five consecutive quarters of double-digit year-over-year earnings growth.

Importantly, this improvement has been building for months:

-

On September 30, Q4 earnings growth was estimated at about 7.2%

-

On December 31, it was 8.3%

-

Today, the blended rate stands at 11.9%

In other words, the season has consistently raised the bar for the index.

Where the earnings upside is coming from

The acceleration in earnings growth is concentrated in three high-impact sectors:

Information Technology, Industrials, and Communication Services — the main drivers of the upgrade since year-end.

-

Industrials: the biggest narrative shift, but with a meaningful one-off component.

The sector’s blended earnings growth has swung from -0.3% to +25.6% since December 31, largely driven by two headline surprises:-

Boeing: $9.92 vs -$0.44 expected

-

GE Vernova: $13.48 vs $2.93 expected

A key nuance: both prints were heavily influenced by one-time items (a major gain on an asset sale for Boeing and a sizeable tax-related benefit for GE Vernova). This boosts the season’s stats, but doesn’t fully translate into underlying run-rate strength.

-

-

Information Technology: high-quality support for the index.

Tech has lifted blended earnings growth from 25.8% to 29.8% year over year, with major contributions from:-

Apple: $2.84 vs $2.67

-

Microsoft: $4.14 vs $3.91

-

-

Communication Services: Meta is once again moving the needle.

The sector’s growth rate has improved from 6.2% to 10.2%, led by:-

Meta Platforms: $8.88 vs $8.21

-

Looking ahead

Markets are still pricing in continued double-digit earnings growth beyond Q4. Consensus projections for the next four quarters remain ambitious, reinforcing the idea that fundamentals—at least on earnings—are still doing the heavy lifting for valuations. So far, the Q4 season is delivering.

-

Q1 2026: 11.7%

-

Q2 2026: 14.9%

-

Q3 2026: 15.2%

-

Q4 2026: 15.4%

Source: FactSet Research Systems

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

🔼 Gold gains 1.7%