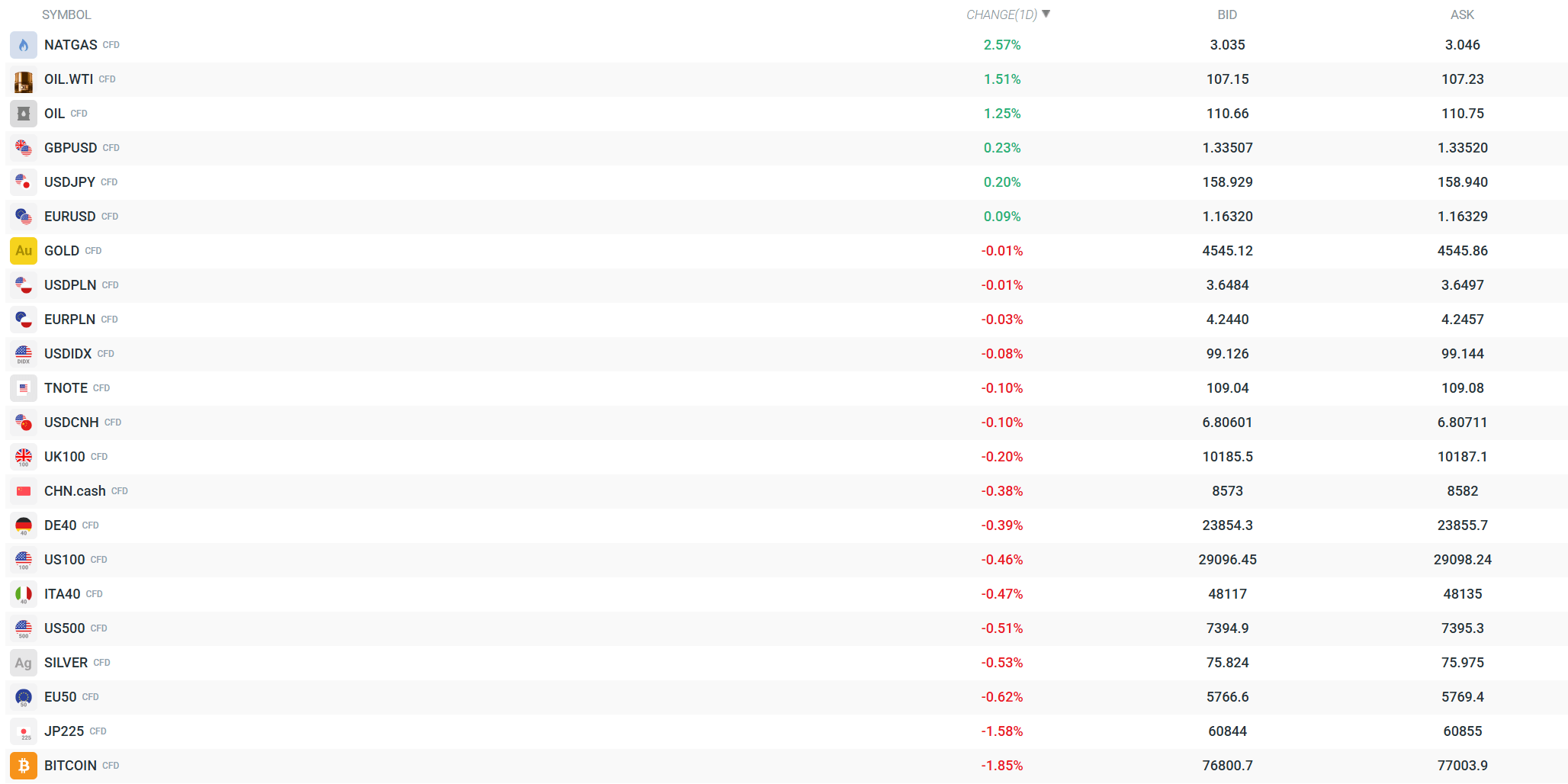

The opening minutes of Monday’s session on European markets have seen moderate declines across most stock indices — futures are clearly pointing in this direction. The German DE40 is down 0.39%, whilst the EU50 is down 0.62%. Investors are paying close attention to new developments regarding the conflict in the Middle East, which remains the main driver of volatility — Trump has warned Iran that “the clock is ticking”, and a Situation Room meeting is scheduled for Tuesday. In the background, the issue of the Q1 earnings season is also becoming increasingly prominent, with NVIDIA’s report set to take centre stage on Wednesday.

Current contract prices. Source: xStation

WHAT CAN WE EXPECT FROM TODAY’S SESSION AND THE REST OF THE WEEK?

-

Trump is convening a Situation Room meeting on Tuesday with his top national security advisers to assess the deadlock in negotiations with Iran and consider further military action. Any news from this meeting could send shockwaves through the markets — particularly oil, which is already up by nearly +1.9% to around $107.50/bbl for WTI.

-

The Iranian standoff is the main catalyst of the week — Trump wrote on Truth Social that “nothing will remain” if Iran does not act quickly, and peace talks have clearly reached an impasse. A drone attack on a nuclear facility in the UAE further drove up oil prices and bond yields. 10-year Treasuries climbed to 4.631% — their highest level since February 2025 — whilst 30-year bonds reached an annual high of 5.159%

-

Weak data from China for April is weighing on sentiment: retail sales rose by just 0.2% year-on-year (the weakest growth since December 2022), industrial production slowed to 4.1%, and fixed-asset investment contracted by 1.6% — all below forecasts. Beijing has not announced any new stimulus measures, which is disappointing for markets expecting a stronger fiscal response.

-

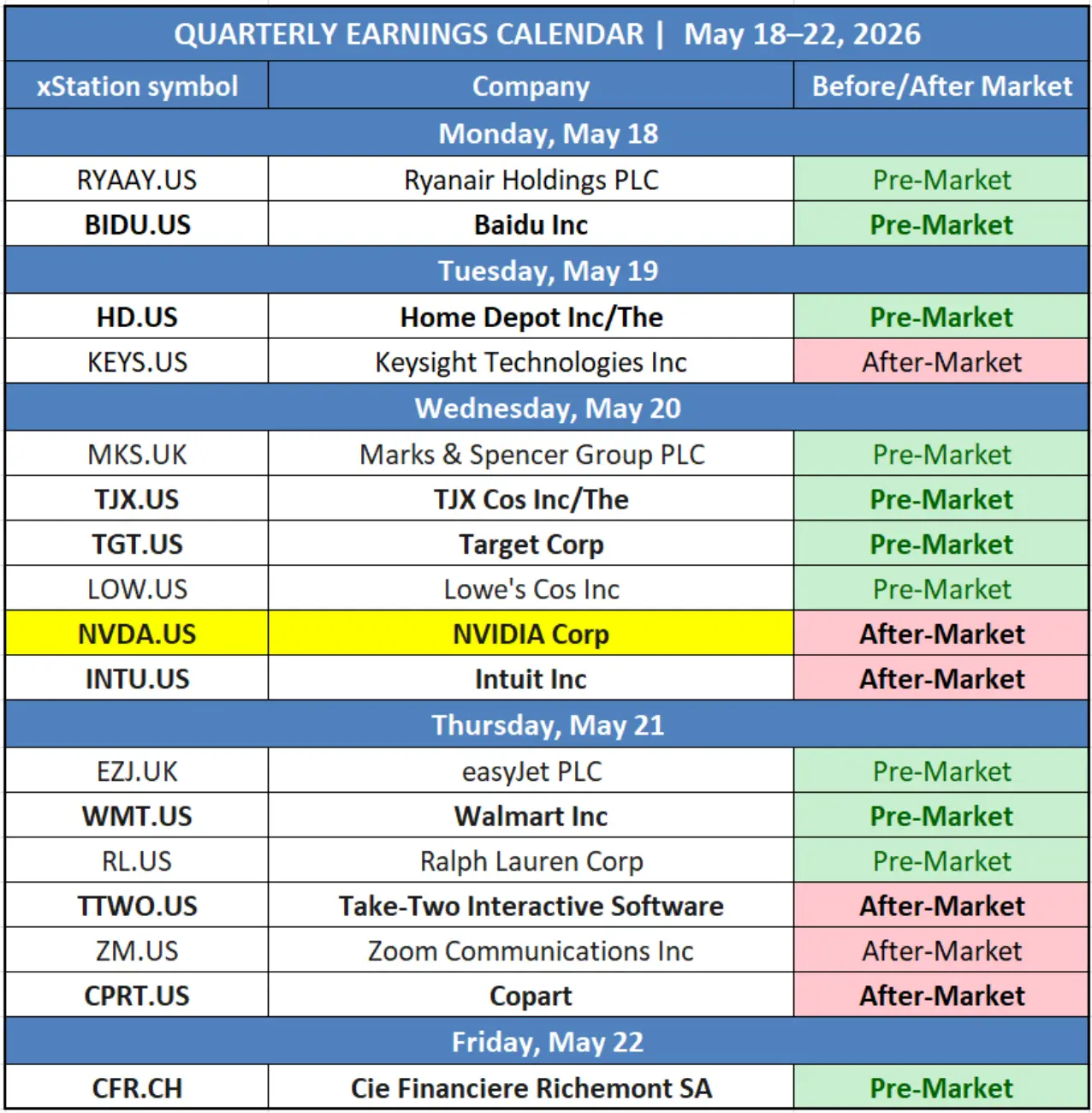

A key week for corporate earnings: NVIDIA is due to report its results on Wednesday after the market closes — the consensus forecast is for EPS of $1.78 and revenue of around $79 billion, with the share price at all-time highs (+26.5% YTD). On Wednesday before the market opens, TJX, Target and Lowe’s will report their results, followed by Walmart and Take-Two Interactive on Thursday — a comprehensive test of the health of the US consumer and the gaming industry.

-

Before the markets opened today, Ryanair (RYAAY) and Baidu (BIDU) reported their results — the latter serving as a barometer of Chinese digital consumption and advertising following weak macroeconomic data. At 2.00 pm, Poland’s core inflation figures for April will be released.

The key macroeconomic reports scheduled for this week are listed below ⬇️

Source: XTB

Company results calendar

Source: XTB

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

⬆️Oil back above $88

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)