Today, after the close of trading on Wall Street, we begin the Q2 2023 earnings season among the companies with the largest market capitalisation (the companies that make up the so-called "Magnificent 7"). On target for investors are: Tesla (TSLA.US) and Netflix (NFLX.US). You can read about Netlix's results preview themselves here, while we will focus on what Elon Musk's company may present tonight.

Tesla (TSLA.US), starting late last year, has been waging a kind of price war to boost demand and stifle competition from other carmakers such as Ford Motor (F.US).

What aspects will investors be paying particular attention to?

-

How is the company performing in an environment of increasing competition?

-

Will the reported strong car sales manage to meet investors' expectations?

-

How will Tesla's declining margins affect all of this?

-

Will the company manage to increase revenue diversification opportunities by activating in the electric car charger market?

What do we know after the Q2 car sales report?

Price cuts on Tesla's most popular models, according to the company's introduced plan, were expected to increase car sales. This has also happened, as confirmed by the reported sub-data. At the moment, the analyst consensus assumes that this trend will be maintained over the next two quarters. However, on the other hand, the emerging surplus of production over reported sales could be an element of risk in the future due to the reported lower consumer activity in the US. Source: XTB, Bloomberg

What are the consensus earnings assumptions?

-

Adjusted EPS: $0.82 (+8.23% YoY; - 3.66% QoQ)

-

Revenue: USD 24.67bn (+45.66% YoY; 5.73% QoQ)

-

Net profit: US$2.89 billion (+10% YoY; -1.7% QoQ)

-

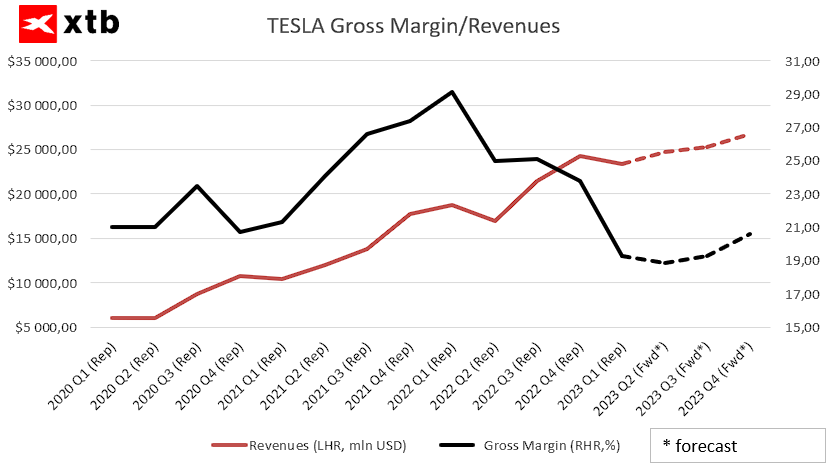

Gross margin: 18.85% (19.3% in Q1 2023; 25% in Q2 2022)

The main focus of today's report will be on margins, which have been declining on a wave of increased production and price reductions for individual Tesla car models. However, this trend is expected to change in the next quarters. Source: XTB, Bloomberg

Diversification in the charger market a long-term opportunity for Tesla?

As EV sales are declining, Tesla is taking aggressive steps to capture a larger share of the US charging market in order to diversify revenue. To this end, the company has entered into partnerships with Ford Motor (F.US) and General Motors (GM.US).

The market rejoiced at this news. Nevertheless, it is worth remembering that in the short term, the established partnerships will not drive Tesla's performance. In the long term, however, these agreements could translate into an additional USD 9.65 billion in revenue (Piper Sandler forecast for 2032). Source: Refinitiv

Current valuation:

Although Tesla (TSLA.US) shares have gained more than 138.51% this year, a multiples analysis does not indicate that Elon Musk's company shares are extremely overvalued. The EV/EBITDA (NTM) and P/E (NTM) ratios oscillate around the 3-year average. Of course, in nominal terms, these indications are very large, but for a company that maintains a long-term listing with such large multiples, we prefer an analysis relative to historical indications.

EV/EBITDA (NTM) multiplier for Tesla with standard deviations highlighted (for the 3-year period). Source: Koyfin

P/E multiplier (NTM) for Tesla with standard deviations highlighted (for a 3-year period). Source: Koyfin

Tesla share chart

The company's shares are currently moving in a dynamic uptrend recorded continuously since mid-May this year. The reaction to today's results could lead to a test of the upper or lower limits of this technical structure. Moreover, the shares of Elon Musk's company remain in a resistance zone, defined by the 61.8% Fibo retracement of the downward wave initiated in November 2021. Source: xStation 5

The company's shares are currently moving in a dynamic uptrend recorded continuously since mid-May this year. The reaction to today's results could lead to a test of the upper or lower limits of this technical structure. Moreover, the shares of Elon Musk's company remain in a resistance zone, defined by the 61.8% Fibo retracement of the downward wave initiated in November 2021. Source: xStation 5

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season