In light of the latest escalation in the Middle East, many investors still remember the years 2022–2023 and the persistent fears of rising fuel prices, especially in Europe. It is no coincidence that many market participants and observers see a scenario of another wave of fuel shortages and a rise in inflation that would bury hopes of a continued recovery in the economies of the European Union.

However, the Europe entering 2026 is not the same Europe as in 2020 or 2022. The economies and markets of developed countries have learned a painful lesson about import dependence. That lesson has not been absorbed in full, but it has been absorbed to a large extent.

The situation of each country in Europe is different, yet despite significant market destabilization, none of them is currently in a situation that could be described as difficult.

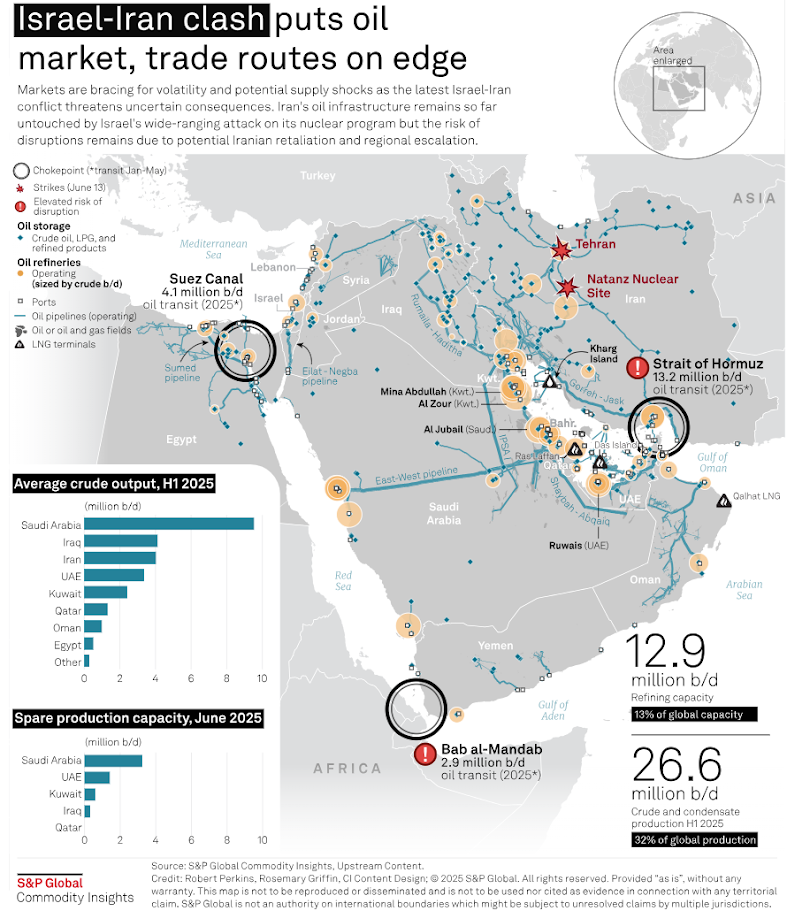

The Middle East is associated by most people with crude oil; however, oil from the Arabian Peninsula goes mainly to Asia rather than to Europe. Europe remains critically dependent on hydrocarbon imports, but it meets a large share of its energy needs through supplies from Norway and the United States.

The Middle East itself has not remained passive, waiting for an inevitable U.S. war with Iran. The “East–West” pipeline currently runs across the Arabian Desert and is capable of pumping between 5 and as much as 7 million barrels of oil per day to ports on the Red Sea, completely bypassing the Strait of Hormuz. Meanwhile, along the Tigris River in Iraq runs the “Al Haditha–Rumalia” pipeline, which then connects to the “Kirkuk–Ceyhan” pipeline, through which an additional 1.5 million barrels per day can be delivered to Turkey.

Source: S&P Global

The situation looks worse when it comes to LNG gas, where import dependence is greater, more concentrated, and offers no easy way to bypass the currently “hot” Strait of Hormuz. Still, this is not a reason to panic. Foremost, it is worth looking at the calendar: peak demand for LNG occurs in winter and summer, when heating and cooling are necessary. But it is early March, winter is over, and the arrival of summer heat is at least two months away.

Those two months matter because, regardless of one’s views on the conflict, there is currently no scenario in which Iran emerges victorious from the present confrontation; its defeat, collapse of state structures, or near-total erosion of its ability to continue fighting is now a matter of weeks rather than months. This time “buffer” is reinforced by the fact that after the outbreak of the war in Ukraine, Europe undertook the construction and filling of countless natural gas storage facilities.

The military operations currently underway in the Middle East are a challenge for markets, traders, economies, and central banks to the same extent as for command staffs. However, they are nothing on the scale of what Europe and the world have had to deal with over the past few years.

Yet despite these facts, there are gaps in supply chains that cannot be patched either easily or quickly. That gap is jet fuel. Europe is closing or converting a large portion of its refineries, while demand for passenger flights is hitting record highs. If Europe does not quickly find a way to diversify in this narrow segment of the hydrocarbon market, the consequences for the valuations of European airlines could be dramatic.

LHA.DE (D1)

Source: xStation5

Lufthansa's valuations reflect the combination of strong demand in the passenger flight segment and a number of challenges facing the European economy, such as rising fuel and labor costs. A shortage of aviation fuel could prove fatal for many companies without renewed government intervention.

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

Berkshire earnings: What do the reports say about the market’s direction?

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Intel Needs $15 Billion. Is It a Financial Problem or the Price of an Ambitious Expansion?