As we start the second half of the year, the focus is switching to Q2 earnings season. Last quarter saw stunning results for the chip makers, the Dow Jones closed the quarter at a record high, and the Nasdaq had its fourth best quarterly performance ever. This was in contrast to the FTSE 100, which was a global laggard. As we move into July, the focus is on whether the rally can continue and if there anything that can trip up the AI trade.

Below, we look at 5 names that we think are worth watching in the coming weeks in both the US and the UK.

As we start the second half of the year, the focus is switching to Q2 earnings season. Last quarter saw stunning results for the chip makers, the Dow Jones closed the quarter at a record high, and the Nasdaq had its fourth best quarterly performance ever. This was in contrast to the FTSE 100, which was a global laggard. As we move into July, the focus is on whether the rally can continue and if there anything that can trip up the AI trade.

Below, we look at 5 names that we think are worth watching in the coming weeks in both the US and the UK.

Broadcom

AI custom-chip momentum is the story. Its accelerator chips undercut Nvidia and AMD on cost for specialised workloads, and rising XPU and networking demand should keep sales growing strongly over the next two years. The stock price has fallen by 26% in the past month, which has not been driven by fundamentals. Instead, the sell off means that the valuation is now looking attractive, at only 19 times future earnings. This is cheap for the fast-growing tech sector. Added to this, Broadcom does not report earnings until September 3rd. This means that it could rally on the back of strong results for its competitors, as the market prices in good news for Broadcom ahead of time.

Chart 1: Broadcom

Source: XTB

Tesla

Q2 deliveries for Tesla were stronger than expected at more than 480,000 vehicles for last quarter, vs. expectations of 410,000. European growth was up 25% compared to a year ago, and there are signs that demand is picking up in China, and stabilising in the US. Elon Musk’s distance from Washington seems to be boosting sentiment towards Tesla, along with growing demand for the refreshed Model Y. The company will report earnings on July 22nd. Stronger deliveries, which included a draw down on inventories built up during Q1, could boost the fundamental outlook for Tesla, after a torrid few years for the company.

The stock price sold off sharply on Thursday 2nd July, even though the delivery numbers were strong for Q2. The stock price was down 7%, as fears grew about margin since sales growth was achieved by large-scale discounting. However, we think it was classic ‘buy the rumour and sell the fact’. The stock price is still higher by more than 6% in the past week.

Tesla’s earnings will not just be about vehicle deliveries, it will also be about full driverless technology, and robotaxis. A ruling in the EU later this year could massively increase usage of Tesla’s driverless technology across the Continent, and robotaxi updates are also worth watching. Overall, deliveries are moving in the right direction for Tesla, so optimism may build ahead of the earnings report later this month.

Chart 1: Tesla 3-month chart

Source: XTB

JPMorgan / big US banks

Earnings season kicks off with banks on July 14–15, ahead of the wider “Magnificent 7” reports, and financials are flagged as a top earnings-growth driver this quarter, helped by strong investment-banking activity. The Fed’s July 28 rate decision is a second catalyst for the group. A scaling back of Fed rate hike expectations due to the much weaker than expected June payrolls report may be too hasty, since the Fed remains laser focused on inflation under the helm of new chair Kevin Warsh. If the Fed signals that rate hikes will remain elevated for the long term at their meeting at the end of July, this may boost the outlook for the US banking sector, as it would protect net interest income for the long term.

A strong run for US banks in recent months could be bolstered by a rotation into non-tech sectors of the US stock market. The Dow Jones hit a record at the end of June, which is a sign of demand for stocks outside of the tech sector and the AI trade, which could also increase the attractiveness of the banking sector in the second half of this year.

Chart 1: JP Morgan

Source: XTB

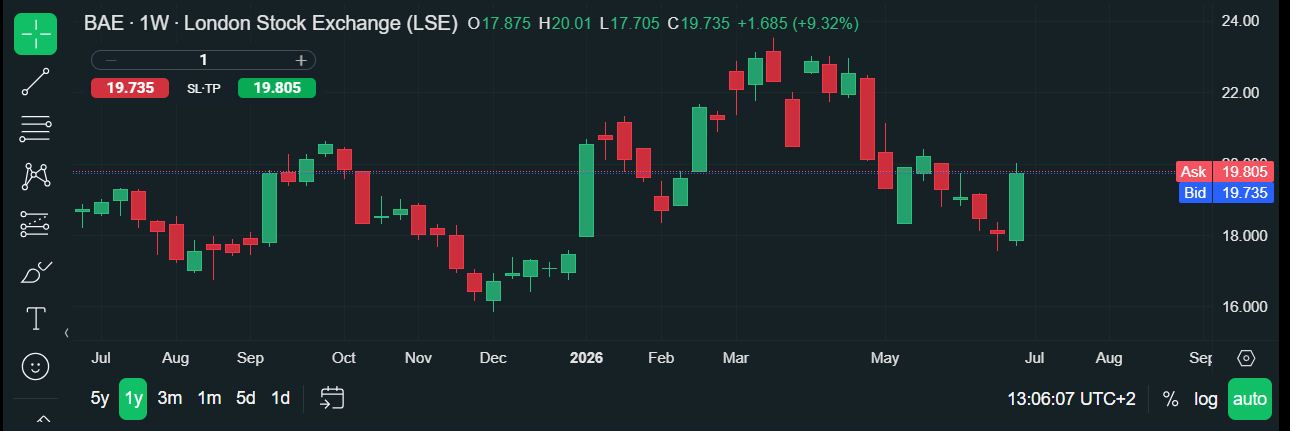

BAE Systems

Switching attention to the UK, defence is a major theme as the UK bulks up its defence spending over the coming years. BAE guided for 7–9% sales growth and 9–11% EPS growth in 2026, with European defence spending accelerating and a new AI-related partnership with Scale AI, however the risks are to the upside. Shares are already up more than 15% year-to-date, and it has had a good week, rising 10% in the first week of July. Its next generation combat jet is seen as being a major beneficiary of the UK government’s new defence spending plan. With defence spending expected to grow across the West in the coming months and years, we think that BAE Systems is poised to extend its recent rally, especially if stock market demand broadens out. BAE Systems is a good momentum play as we move into the second half of the year.

Chart 4: BAE Systems 1-year chart

Source: XTB

Lloyds Banking Group

Lloyds will release its latest earnings report on July 30th, which will be an important read on UK domestic health. Lloyds stock price has had a stunning 54% rise YTD, as the European banking sector has a strong run. Lloyds was caught up in the motor finance scheme that could lead to a total compensation bill for the sector of £9.1bn; the latest details on the case suggests that Lloyds is not required to pay scheme compensation, but does need to handle individual complaints. We think that this crisis is mostly behind the bank and this is a big reason for its outperformance this year. Looking ahead to the second half of the year, we think that fundamentals will come back into play.

Rate cut expectations from the BOE remain on the backburner ever since the energy price spike, however, rate hikes have now been priced out, with the market expecting rates to remain on hold for the rest of this year. Lloyds is the most rate-sensitive of the big four banks in the UK, given its mortgage-heavy book, so the August BoE decision and any further gilt-market moves matter for Lloyds. The next major challenge for the Gilt market will be Andy Burnham’s choice of Chancellor when he becomes PM later this month. If his pick is considered negative for the UK’s fiscal outlook, UK bond yields could surge, which would be bad news for UK banks.

Alternatively, a market-friendly pick could boost UK Gilts, which is good news for the banking sector, as banks have been rallying alongside Gilts so far this year. A back-track on rate hikes from the BOE is also good for Lloyds’ net interest income going forward, and we could see positive forward profit guidance when they report results later this month.

Chart 1: Lloyds Banking Group, 1-year chart

Source: XTB

5 Top Stocks to Watch out for Right Now

5 Top Dividend Stocks for 2025 - Strong Picks Amid Market Volatility

How to Choose the Best Stock Broker in the UK

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.