This month is a huge month for investors. From the first FOMC meeting with new chair Kevin Warsh at the helm, a crucial UK election and traders trying to fit in watching the football World Cup, there are several key themes that could spike volatility and make it an extremely interesting month from a trading perspective.

Below, we look at our top 5 stock picks for the month ahead:

This month is a huge month for investors. From the first FOMC meeting with new chair Kevin Warsh at the helm, a crucial UK election and traders trying to fit in watching the football World Cup, there are several key themes that could spike volatility and make it an extremely interesting month from a trading perspective.

Below, we look at our top 5 stock picks for the month ahead:

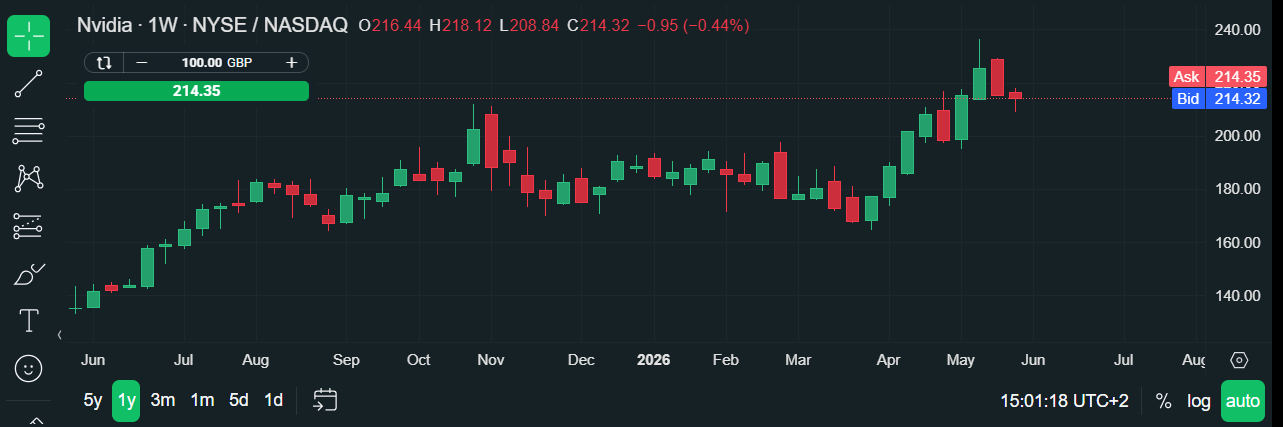

Nvidia

This is the defining AI stock going into June. Nvidia posted Q1 FY2027 revenue of $81.6 billion, up 85% year-on-year, smashing Wall Street estimates of $78.9 billion. The near-term catalyst is COMPUTEX 2026 on 2 June, where Jensen Huang is expected to showcase Vera CPU momentum and agentic AI developments. Huang also recently joined Trump's delegation to Beijing for a summit with Xi Jinping, sparking optimism about increased semiconductor sales in China, a major market for the industry, and one where export restrictions could potentially be eased or renegotiated. With a consensus "Strong Buy" and a mean analyst price target implying further upside is likely, it remains the central A trade as we head into summer. Added to this, in May, the stock rose just over 2%, and was a laggard compared to huge gains for other AI names like Micron, Qualcomm, SanDisk and AMD. This means that its valuation, currently has a P/E ratio of 32 times earnings, is less frothy than other AI names. Risks to watch out for include any breakdown in US-China trade relations or export restriction tightening, which could reverse sentiment sharply.

Chart 1: Nvidia 1-year chart

Source: XTB, Past performance is not a reliable indicator of future results.

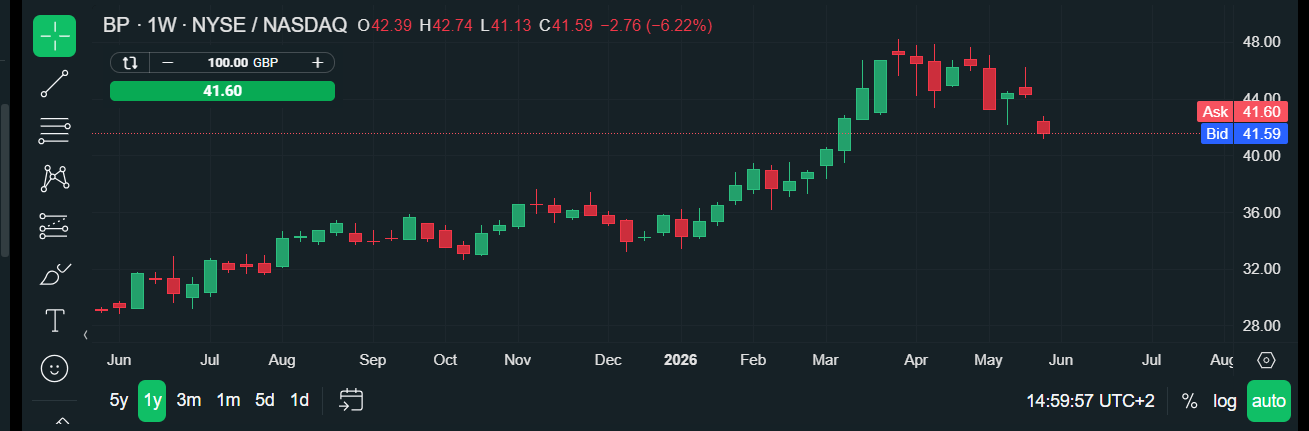

BP

As we move into June, BP bulls will be hoping the stock picks up after a torrid May, where a plunging oil price and problems with its chairman caused its share price to fall 10%. BP will be directly impacted by the oil price and the Strait of Hormuz ceasefire narrative. Q1 2026 underlying replacement cost profit came in at $3.2 billion, comfortably beating analyst expectations of $2.63 billion, with the analysts noting that "elevated oil prices tend to lift all boats in the energy sector, but being an integrated player means BP will see enhanced cash flow as oil prices remain elevated." Goldman Sachs flagged BP as having particularly strong upside, with its 2026 earnings forecast sitting around 82% above consensus estimates, even after the stock has already advanced significantly since Middle East tensions escalated.

The chief risk for BP’s share price in June would be a fall below $80 per barrel, which could dent Q3 profits.

Chart 2: BP 1-year chart

Source: XTB, Past performance is not a reliable indicator of future results.

Goldman Sachs

M&A activity is expected to surge to more than $3 trillion this year, led higher by mega cap deals of more than $10bn, including Uber’s recent multi billion dollar bid for German food delivery firm Delivery Hero. Goldman is the clearest beneficiary of a global M&A boom, and elevated market volatility is also helping to feed trading revenues. Goldman reported Q4 2025 investment banking fees up 25% and said its M&A backlog was at its highest level in four years, with CEO David Solomon pointing to significantly improved corporate optimism heading into 2026. Globally, M&A volumes were up 40% year-on-year with deals over $500m in EMEA up 150% and APAC up 300%. June brings continued dealmaking activity, elevated FICC and equity trading revenues from macro volatility, and a favourable regulatory backdrop. Q1 2026 saw 14% revenue growth and 19% net income growth, with equity trading revenue up 27%. These stellar results are one reason why Goldman’s stock price is at a record high, but if it can continue to deliver, then there could be further upside for the stock price to come. As Goldman works through its M&A backlog, this should continue to boost revenues in Q2 and beyond. The biggest risk to the upside for Goldman’s stock is that persistent inflation and higher-for-longer rates dampen the IPO pipeline and damage debt capital markets activity.

Chart 3: Goldman Sachs 1-year chart

M&A activity is expected to surge to more than $3 trillion this year, led higher by mega cap deals of more than $10bn, including Uber’s recent multi billion dollar bid for German food delivery firm Delivery Hero. Goldman is the clearest beneficiary of a global M&A boom, and elevated market volatility is also helping to feed trading revenues. Goldman reported Q4 2025 investment banking fees up 25% and said its M&A backlog was at its highest level in four years, with CEO David Solomon pointing to significantly improved corporate optimism heading into 2026. Globally, M&A volumes were up 40% year-on-year with deals over $500m in EMEA up 150% and APAC up 300%. June brings continued dealmaking activity, elevated FICC and equity trading revenues from macro volatility, and a favourable regulatory backdrop. Q1 2026 saw 14% revenue growth and 19% net income growth, with equity trading revenue up 27%. These stellar results are one reason why Goldman’s stock price is at a record high, but if it can continue to deliver, then there could be further upside for the stock price to come. As Goldman works through its M&A backlog, this should continue to boost revenues in Q2 and beyond. The biggest risk to the upside for Goldman’s stock is that persistent inflation and higher-for-longer rates dampen the IPO pipeline and damage debt capital markets activity.

Chart 3: Goldman Sachs 1-year chart

Source: XTB, Past performance is not a reliable indicator of future results.

Alibaba

This is the most geopolitically sensitive stock pick for June, and it is likely to be extremely sensitive to any US-China trade progress. Alibaba has pledged $52.4 billion in AI and cloud infrastructure over the next three years, and the stock trades at roughly 22x earnings with $41 billion in net cash - a dramatic discount compared to US cloud and AI companies. Alibaba's Cloud Intelligence Group has delivered nine consecutive quarters of triple-digit year-on-year growth in AI-related product revenues. Jensen Huang's presence at the US-China Beijing summit has raised hopes of eased chip export restrictions, which would be transformative for Alibaba's AI buildout. However, if you are trading Alibaba this month, the downside risk is significant, any economic weakness in China caused by the energy price spike, and any trade truce breakdown with the US could hurt the stock. The stock has been under pressure in 2026, but a cheap AI play could be just what the market needs as we move towards the middle of the year.

Chart 4: Alibaba 1-year chart

Source: XTB, Past performance is not a reliable indicator of future results.

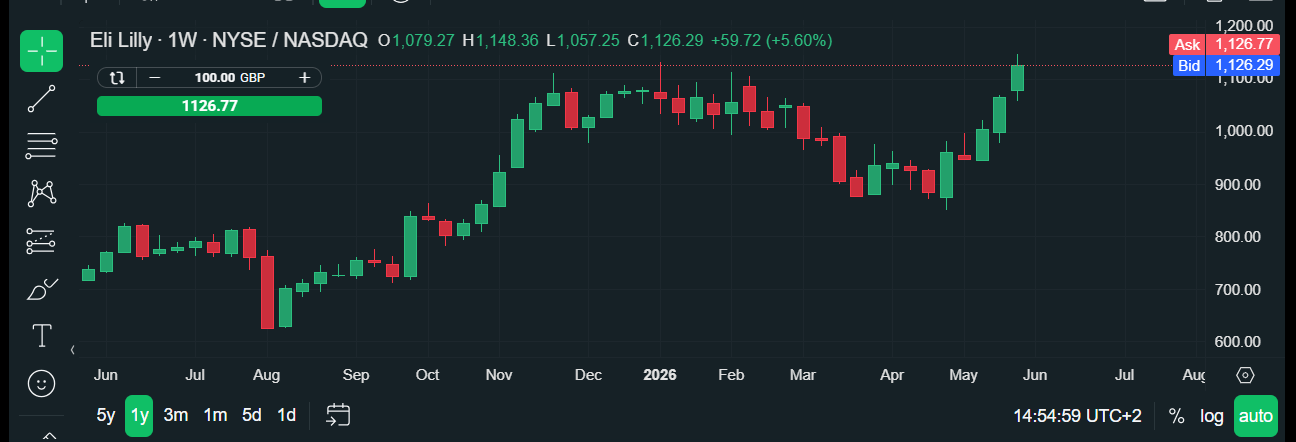

Eli Lily

With macro volatility elevated and inflation sticky, Lilly offers a counterweight - a high-conviction secular growth story largely insulated from rate decisions and oil prices. This is the beauty of healthcare stocks, and Lily could see further stock market gains this month. Last month, the stock price rose by 29%, however, YTD the stock is only higher by 4%, so even though the stock is at a record high, there is the potential for further upside. Analysts at CFRA point to ongoing demand for GLP-1 drugs and demographic longevity trends as sustaining long-term growth, with a "Strong Buy" rating and a $220 price target. In a June environment where investors may be rotating out of rate-sensitive names ahead of the FOMC meeting in the middle of this month, Lilly's defensive-growth profile with structural tailwinds, makes this stock a top pick for June. Risks to be aware of include any clinical setback or pricing pressure from US drug pricing legislation under the Trump administration.

Chart 5: Eli Lilly 1-year chart

Source: XTB, Past performance is not a reliable indicator of future results.

The common thread across these five stocks to watch is that they each represent a direct trade on one of June's dominant macro themes, AI capex, oil/geopolitics, capital markets activity, US-China relations, and the potential for higher interest rates in Europe and a tightening bias at the Fed. Worth watching as we move through this month is how the May CPI print on 10 June and the FOMC statement on 17 June shifts the relative appeal of the global stock market.

Taiwan Semiconductor Manufacturing Company (TSMC): A Global Semiconductor Powerhouse

5 Top Stocks to Watch out for Right Now

5 Top Dividend Stocks for 2025 - Strong Picks Amid Market Volatility

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.