Arabica coffee futures on ICE (COFFEE) are trading at their lowest levels since autumn 2024 as the market increasingly focuses on Brazil’s ongoing harvest and the prospect of rising supply from the world’s largest coffee producer. Ecom Group, one of the world’s largest coffee traders, has signaled that this year’s crop could reach a record high. Such an outcome would be fundamentally important for the market, as a large Brazilian harvest could help rebuild global coffee inventories. Arabica prices have already fallen more than 20% this year, mainly due to improving expectations for Brazilian production. However, to gain a clearer picture of market positioning, it is worth examining what large speculators and producers are pricing in through the CFTC Commitment of Traders report.

Is the risk of low inventories fading?

- Stocks in exchange-monitored warehouses have been shrinking for the past five years following several seasons affected by droughts and frosts. Gradually, the market is shifting away from the narrative of tight supply and structural deficits toward expectations of a potential surplus.

- In the short term, weather remains the key risk factor. Recent rainfall in Brazil has raised concerns about possible harvest disruptions and deteriorating bean quality in selected regions, including Minas Gerais. Climatempo meteorologists forecast heavy rainfall in the coming days, along with strong weather instability across major producing regions around São Paulo next weekend.

- So far, however, rainfall has not been significant enough to materially disrupt this year’s harvest. Rabobank estimates that unless a major weather event occurs, the market will gradually move into a large surplus phase, which should continue to pressure prices lower.

- On the other hand, a strong El Niño expected in the 2027 season could negatively impact next year’s Brazilian production. Another concern is the potential delay of rains in September and October, which are crucial months for flowering.

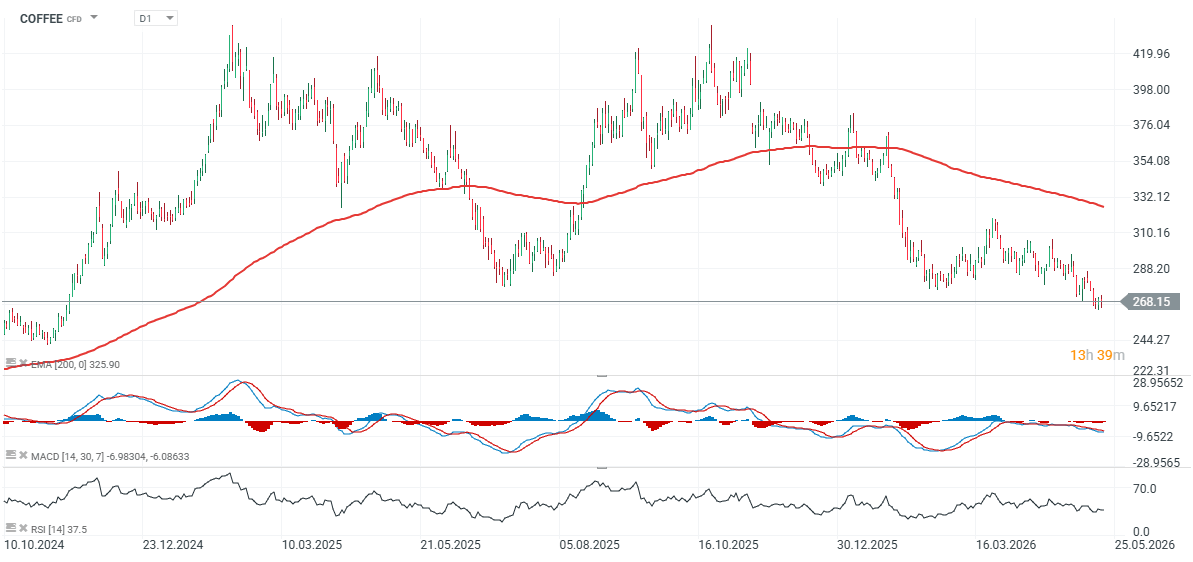

The current price decline is based mainly on very strong expectations for the ongoing season, but the coffee market reacts quickly to any signs of weather-related risks for future crops. At the same time, demand from Chinese buyers continues to grow steadily. In summary, the supply-driven scenario currently dominates and continues to pressure prices, but weather conditions in Brazil remain the key factor capable of rapidly shifting market dynamics. Looking at the chart, prices have fallen back to levels last seen in mid-November 2024.

COFFEE chart (D1)

For bulls, the key level is currently a move back above 280, where we can see important historical price reactions. Bears, meanwhile, may attempt to push prices toward 240, which represents another important price action zone marked by local lows from autumn 2024.

Source: xStation5

Are speculators aligning with producers?

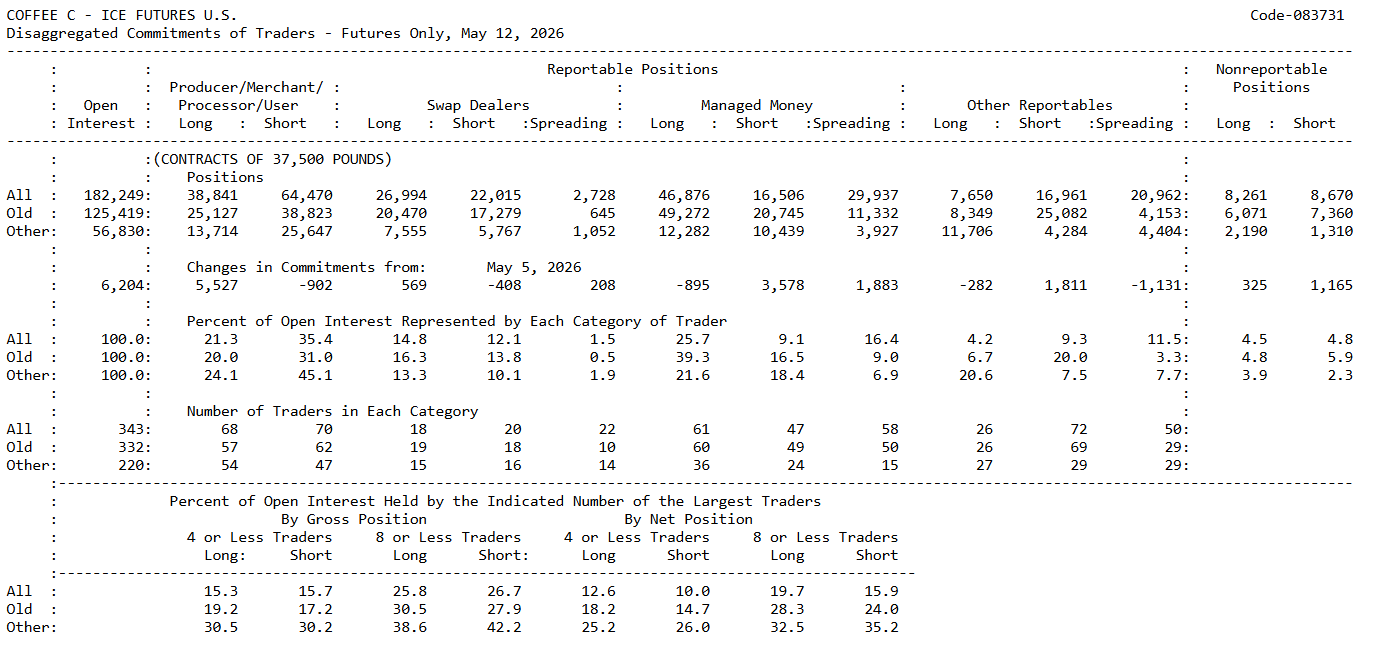

The latest CoT report for Arabica coffee (ICE, May 12, 2026) shows a market undergoing a clear narrative shift: from fears of supply shortages toward increasingly aggressive positioning for large Brazilian production and lower prices. The most important development is that Commercials (physically involved market participants hedging supply exposure) remain heavily net short, but their short exposure has started to decline, while Managed Money is aggressively reducing longs and increasing shorts. This relationship is particularly important because Commercials usually represent the physical coffee market: exporters, producers, and hedgers, while Managed Money consists mainly of speculative funds reacting to momentum and sentiment.

- Commercials currently hold 38,841 long contracts and 64,470 short contracts, leaving them net short by roughly 25.6 thousand contracts. They therefore remain clearly positioned to hedge sales at current price levels. However, the key detail is that Commercial long positions increased by 5,527 contracts, while shorts declined by 902 contracts. This suggests that the commercial sector is no longer hedging further downside as aggressively as before, is partially closing existing hedges, and may believe that a significant portion of the bearish move has already played out.

- Meanwhile, the Managed Money category has become noticeably more bearish compared to the previous week. Funds hold 46,876 longs and 16,506 shorts, for a net long position of around 30.4 thousand contracts. While the net position remains positive, the change in positioning is more important: longs fell by 895 contracts, while shorts surged by 3,578 contracts. This reflects a significant shift in speculative sentiment. Funds are gradually abandoning the narrative of a lasting structural deficit, the market is increasingly pricing in larger Brazilian supply, and more participants are actively positioning for further downside.

- The earlier weather-driven bull market narrative is fading, while the market transitions toward expectations of oversupply. Another interesting detail is the increase in Managed Money spreading positions by 1,883 contracts, suggesting more tactical relative-value strategies between contract months rather than simple directional longs.

- Open Interest rose to 182,249 contracts, up 6,204 contracts week-over-week. This is important because falling prices combined with rising open interest usually indicate new capital entering on the short side. Technically, this confirms the bearish trend.

- Commercials still account for a very large share of market shorts, representing 35.4% of total open interest on the short side. This continues to show that the physical market is using relatively elevated prices to hedge sales. At the same time, Managed Money’s share of long open interest fell sharply from 39.3% to 25.7%, marking a major shift from previously extremely bullish speculative positioning.

- The market currently looks as follows: Commercials remain structurally bearish, although less aggressively than before, while funds are only beginning to shift toward more bearish positioning. This often signals the middle phase of a broader downside move, where smart money from the physical market partially realizes earlier hedges while speculative positioning starts to reverse.

In the short term, the market remains vulnerable to technical rebounds because funds still maintain a sizable net long position, and any weather threat to Brazil could trigger short covering. Medium term, however, the report supports a scenario of larger supply, rebuilding inventories, and gradually lower Arabica prices, provided weather conditions in Brazil do not deteriorate significantly.

Source: CFTC, CoT

Eryk Szmyd Financial Markets Analyst, XTB

Silver breaks above $59 and attracts capital again. Gold remains in the shadow of its younger sibling

Healy makes first move as Chancellor, but bond market not impressed

Chart of the day 🔼Nasdaq gains 1.2% as semiconductors rebound (21.07.2026)

Daily Summary: China Shows Its Teeth on AI; The U.K. Sees a Government Revolution 🏛️

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.