-

Illusory Industrial Recovery: While PMI readings rose above 50, growth is driven by panic-stockpiling rather than genuine demand; in Germany, business sentiment has hit its lowest point in 18 months.

-

Stagflation Risks and the "Adverse Scenario": With oil prices near $110, the Eurozone is nearing the ECB’s stress-test model, which projects inflation spiking to 3.5% and necessitates a forceful monetary response.

-

Market Pricing in Hikes: Investors are nearly certain of a June rate hike and anticipate three total increases this year (to 2.75%), keeping German 2-year yields anchored around 2.67%.

-

Illusory Industrial Recovery: While PMI readings rose above 50, growth is driven by panic-stockpiling rather than genuine demand; in Germany, business sentiment has hit its lowest point in 18 months.

-

Stagflation Risks and the "Adverse Scenario": With oil prices near $110, the Eurozone is nearing the ECB’s stress-test model, which projects inflation spiking to 3.5% and necessitates a forceful monetary response.

-

Market Pricing in Hikes: Investors are nearly certain of a June rate hike and anticipate three total increases this year (to 2.75%), keeping German 2-year yields anchored around 2.67%.

The latest manufacturing data for April 2026 presents a deceptive veneer of health across the Eurozone. While headline figures suggest a long-awaited rebound, the underlying mechanics reveal a bloc struggling with deep structural fractures exacerbated by the ongoing Middle East conflict. The Eurozone Manufacturing PMI rose to 52.2, yet market participants are looking past the headline with growing trepidation.

A Two-Speed Bloc Driven by Pre-emptive Buying

For the first time in nearly four years, all eight monitored Eurozone economies have crossed into expansionary territory (above 50.0). However, the drivers of this growth are anything but organic:

-

France and the Periphery: France’s PMI climbed to 52.8, with notable momentum in Italy and Spain. Yet, this "growth" is largely the result of aggressive stockpiling. Faced with extreme uncertainty over future supply chains, firms are front-loading orders to hedge against anticipated price hikes and shortages.

-

The German Laggard: In Germany, the industrial heart of Europe, the situation is more precarious. While the PMI printed at 51.4, business confidence has plunged into negative territory for the first time in 18 months. The sector is being strangled by severe delivery delays and a relentless surge in input costs.

The continued closure of the Strait of Hormuz remains the primary choke point for the continent. Supply chain disruptions are now at their most acute since mid-2022. Input price inflation has hit a 46-month high, forcing manufacturers to pass these costs onto consumers at a record pace.

The ECB’s "Adverse Scenario" Becomes the Baseline

The simultaneous release of the ECB’s Survey of Professional Forecasters (SPF) confirms the hawkish shift, with 2026 inflation expectations revised upward to 2.7%. While ECB President Christine Lagarde has maintained a characteristic degree of ambiguity regarding the bank's internal modeling, the reality on the ground—with Brent crude trading just shy of $110 per barrel—places the Eurozone firmly within the ECB’s "adverse scenario."

Under this stress-test scenario, oil at $119 leads to an inflation spike of 3.5%, necessitating a forceful monetary response.

Monetary Policy and Sovereign Debt:

-

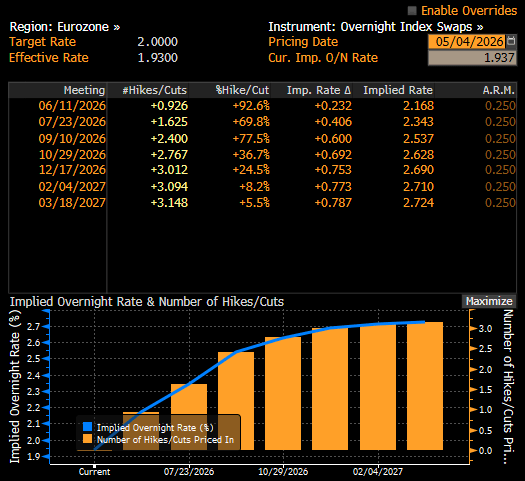

Rate Path Realignment: Swaps markets are now pricing in three 25-basis-point hikes this year with near-total certainty. Sentiment is coalescing around an initial move as early as June, which would lift the deposit rate to 2.75%.

-

Bund Yields: The front-end of the German curve appears to have found its footing. Two-year Bund yields at 2.67% now adequately reflect the market’s hawkish read of the OIS curve. Barring a move in crude toward the $120 mark, further upward pressure on yields may be capped in the short term.

Markets are now discounting a June hike with nearly 100% probability. Source: Bloomberg Finance LP

Markets are now discounting a June hike with nearly 100% probability. Source: Bloomberg Finance LP

Stagflation Looms Over the Common Currency

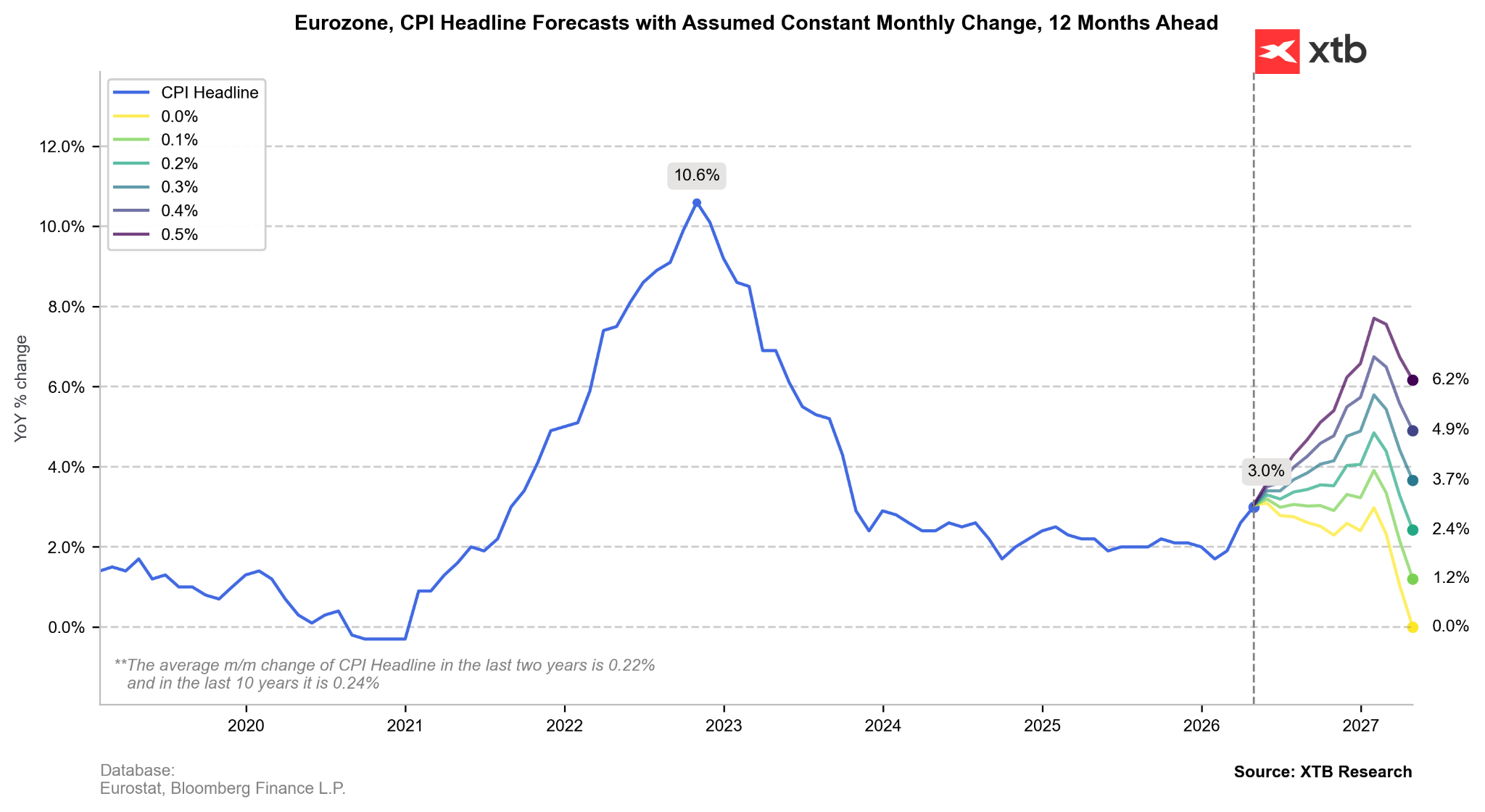

The reluctance of the ECB leadership to explicitly label the current environment as "stagflationary" has not deterred the markets from doing so. The central bank finds itself in the unenviable position of raising rates not to cool a red-hot economy, but to anchor expectations in the face of a supply-side shock. Should the "black swan" of 4% inflation materialize, the ECB will have little choice but to accelerate its tightening cycle.

Internal projections suggest inflation could breach the 4% mark by year-end before mean-reverting, provided energy markets stabilize. Source: Bloomberg Finance LP, XTB

Internal projections suggest inflation could breach the 4% mark by year-end before mean-reverting, provided energy markets stabilize. Source: Bloomberg Finance LP, XTB

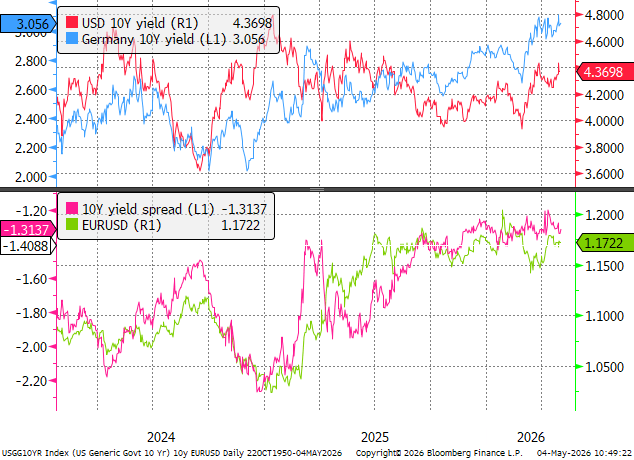

EURUSD: Yield Spreads vs. Reality

From a macro perspective, the Euro appears fairly valued against real interest rates. However, the currency’s trajectory remains tethered to the ECB's resolve. If the Governing Council delivers the three hikes now expected by the street, 10-year Bund yields will likely face significant upward revisions.

EURUSD remains tightly correlated with the 10-year yield spread. Source: Bloomberg Finance LP, XTB

EURUSD remains tightly correlated with the 10-year yield spread. Source: Bloomberg Finance LP, XTB

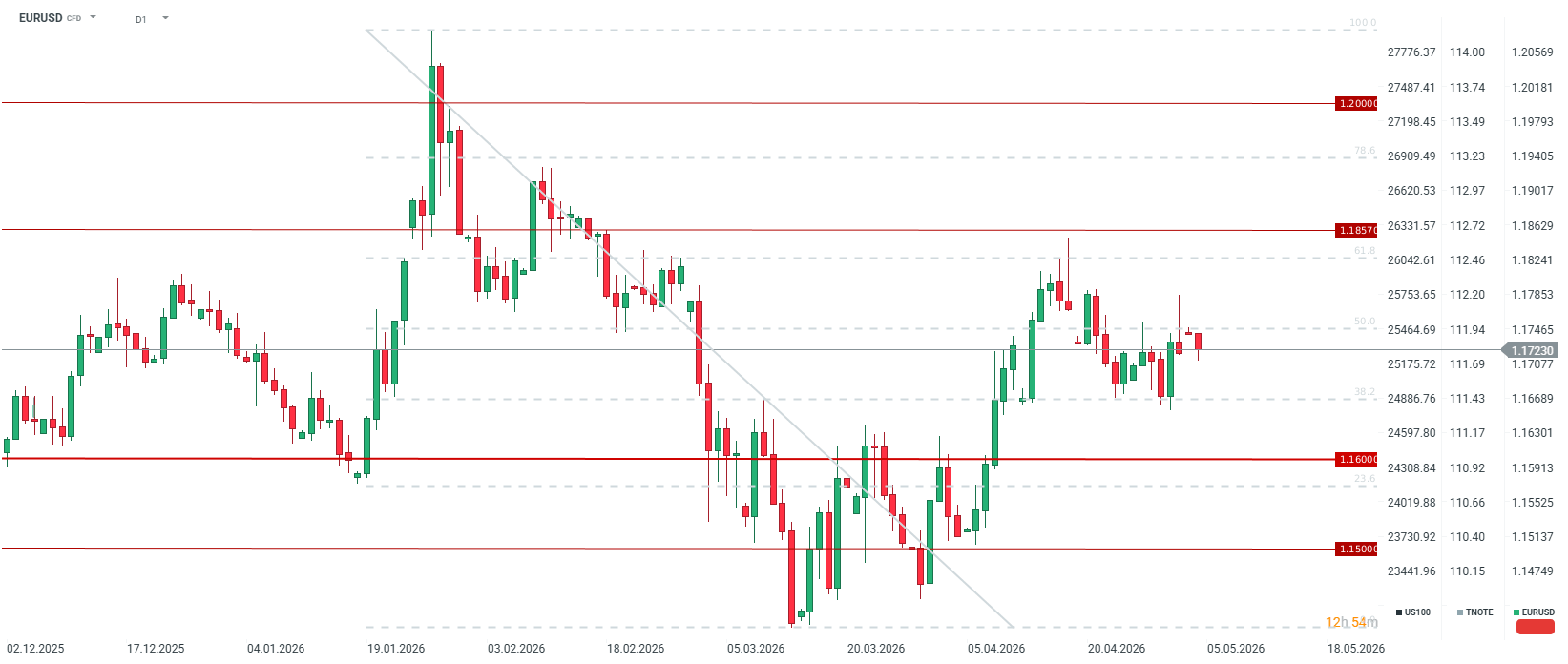

Technically, the pair has softened following a brief foray toward the 1.1800 handle last Friday. In the absence of a fresh geopolitical or macro catalyst, the euro is expected to consolidate between the 38.2% and 50.0% Fibonacci retracement levels, as traders weigh the risk of an ECB-induced slowdown against persistent price pressures. Source: xStation5

Technically, the pair has softened following a brief foray toward the 1.1800 handle last Friday. In the absence of a fresh geopolitical or macro catalyst, the euro is expected to consolidate between the 38.2% and 50.0% Fibonacci retracement levels, as traders weigh the risk of an ECB-induced slowdown against persistent price pressures. Source: xStation5

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.