Let's take a break from the escalating conflict in the Middle East and turn our attention once again to macroeconomic data. The main topic of today's session will be US CPI data, which will be released at 1:30 p.m. GMT+1 .

What to expect from the data?

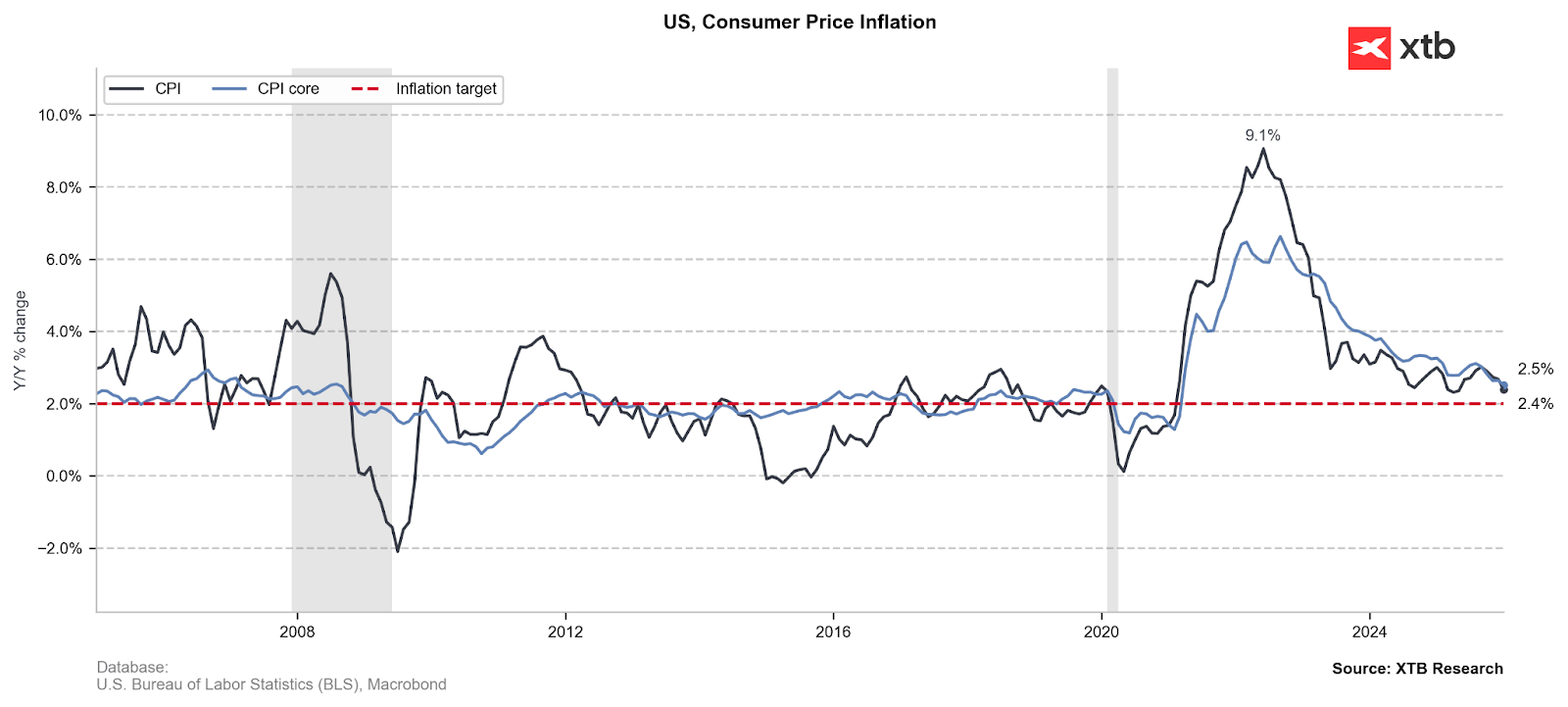

Analysts' consensus, which fluctuates around the latest reading, suggests relatively high uncertainty regarding price dynamics in the US, which still bears the statistical effects of the shutdown. Source: XTB Research, Macrobond data

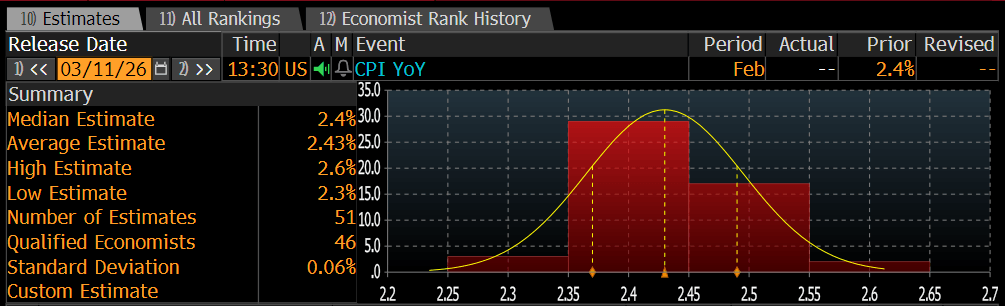

Analysts surveyed by Bloomberg indicate that the risk of price pressure in the US economy has increased again, with a chance of a year-on-year reading of 2.5%. It should be noted that these figures do not include energy price increases resulting from military action in the Persian Gulf.

Breakdown of analysts' expectations for today's CPI report. Source: Bloomberg Financial No.

What did the latest data show?

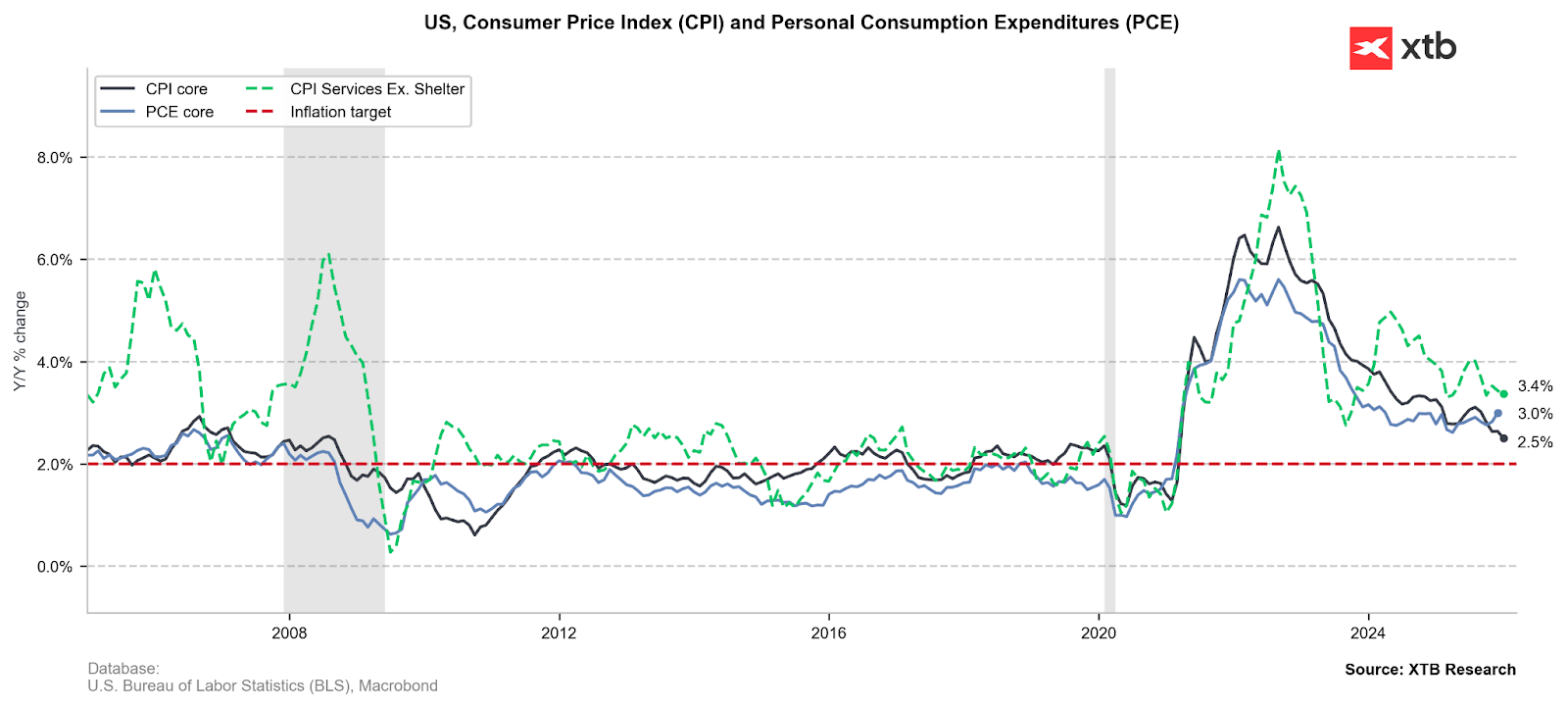

The latest exceptionally low CPI reading in the US lulled investors into complacency ahead of the recent rebound in the PCE base to a symbolic 3% (December data), which points to continued strong price pressure in non-discretionary spending (especially healthcare). Since PCE is the last and therefore the easiest to forecast inflation reading in the US, the surprise of higher-than-expected data for December tipped the balance of concerns about inflation picking up again even before the risks associated with energy prices.

Source: XTB Research, Macrobond data

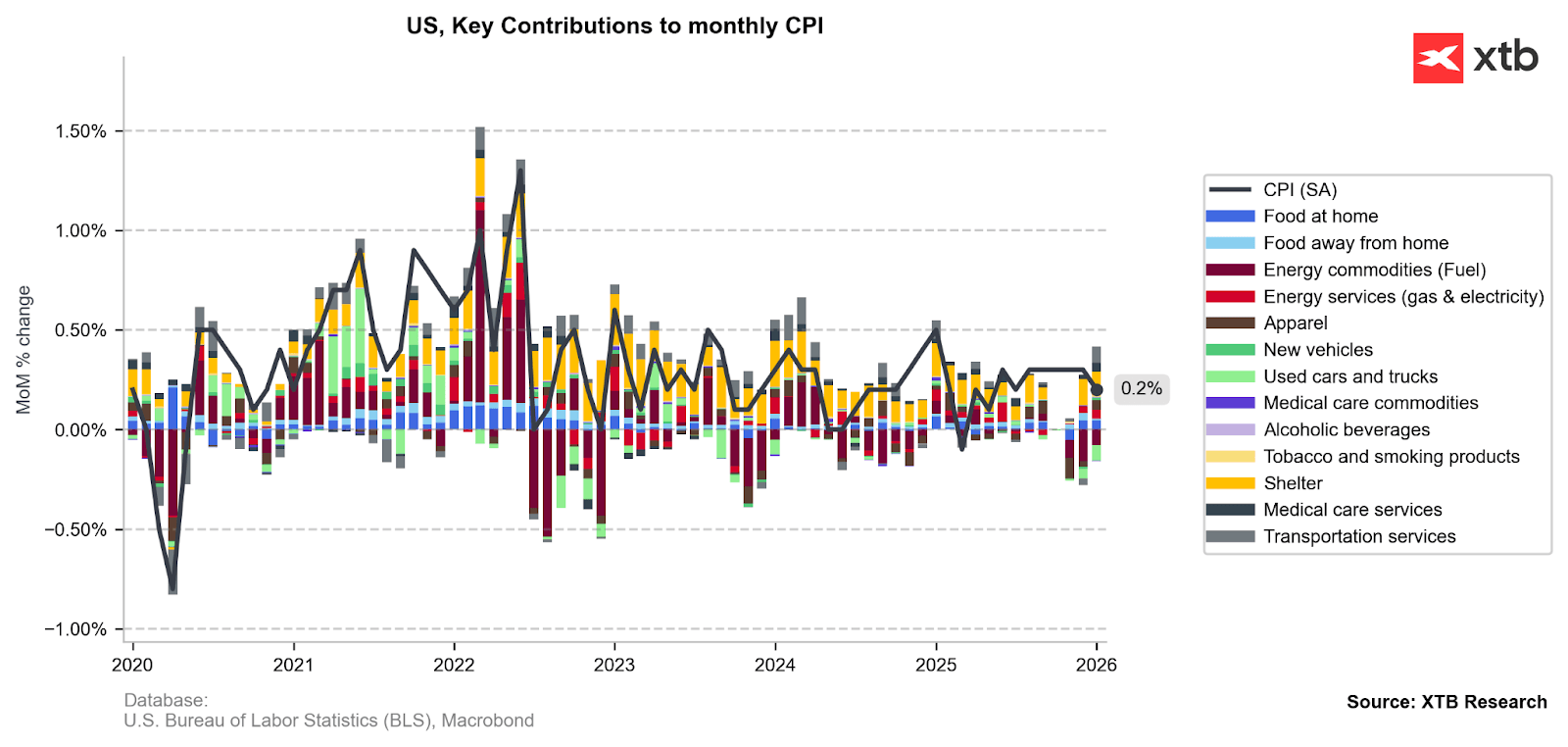

The uncertainty surrounding the upcoming reading is also due to the inflation dynamics in the last month. Declines in energy commodity prices were largely responsible for the lower-than-expected reading, so even if pre-war data show a continuation of the trend, it will be treated as a temporary relief and a basis for a strong rebound in the coming months. Rent inflation (Shelter) should remain on a downward trend, although relief may be limited by rising medical costs and goods exposed to aluminum price increases.

The month-on-month decline in energy commodity and used car prices has been the main source of price relief in the US in recent months. Source: XTB Research, Macrobond data.

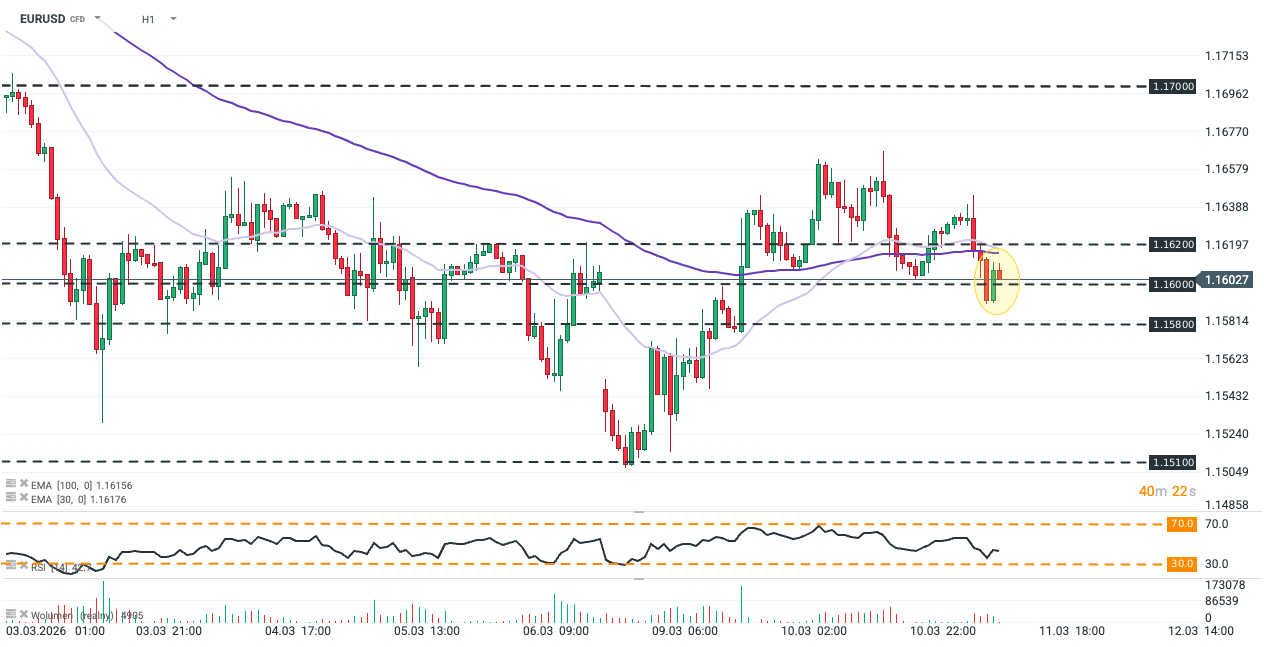

EURUSD chart, D1 interval

EURUSD plunged below the key support level of 1.16 again today, ignoring the rapidly rising swap market valuations of interest rate hikes in the Eurozone. Higher-than-expected inflation in the US could dash hopes of a rebound above 1.162 and push the exchange rate back below 1.158. On the other hand, a neutral reading would favor further consolidation between these levels, reinforced by uncertainty about future data.

Source: xStation5

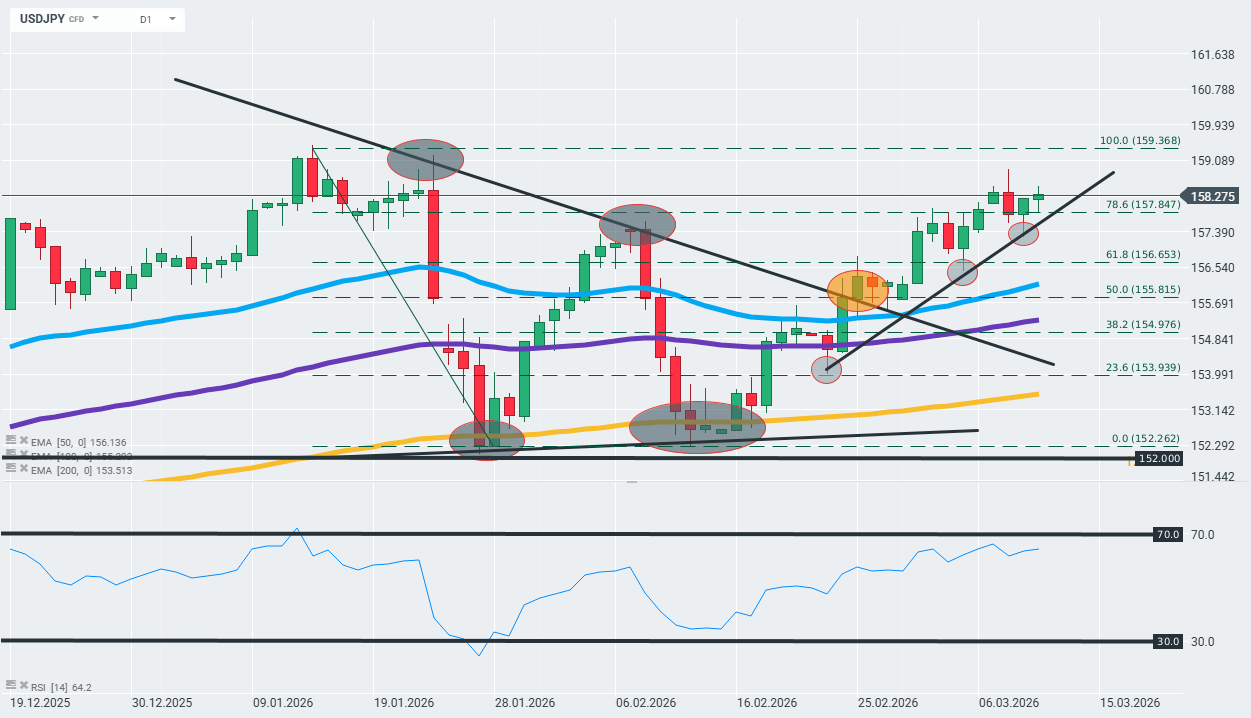

USDJPY chart, D1 interval

The USDJPY pair continues its upward trend ahead of the US inflation reading and continues to defend the key support zone marked by the lower limit of the upward channel that began at the end of February and the 50-day EMA. Stronger price growth in the US could theoretically push the pair even higher, to around 159.37 yen, where this year's highs are located. Conversely, any declines could bring USDJPY back to the aforementioned technical support levels.

Source: xStation5

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.