Economy and Currencies

-

Eurozone: Q4 2025 GDP grew 0.3% q/q and 1.3% y/y, matching preliminary data and market expectations. The foreign trade balance rose for the first time in three months to €11.6 billion (forecast: €11.7 billion; seasonally adjusted).

-

Poland: Consumer inflation (CPI) fell less than expected, moving from 2.4% to 2.2% (forecast: 1.9%). The slowdown was primarily driven by cheaper fuel and transport, while upward pressure came from excise goods (tobacco, alcohol). The reading remains below the NBP's target midpoint of 2.5% (+/- 1 pp).

-

US Dollar: The Dollar Index is gaining for the third consecutive day (USDIDX: +0.15%), still supported by the strong NFP report despite anticipation of the upcoming CPI report (forecast: 2.5%, previous: 2.7%). A tight labor market and solid business activity data suggest a risk of "sticky" inflation; dollar gains may reflect positioning for a potential upside surprise.

-

FX Moves: The Australian dollar (AUDUSD: -0.5%) and yen (USDJPY: +0.5%) are seeing the largest corrections. EURUSD has retreated 0.1% to 1.186, while USDPLN is gaining 0.1% to 3.553.

Indices

-

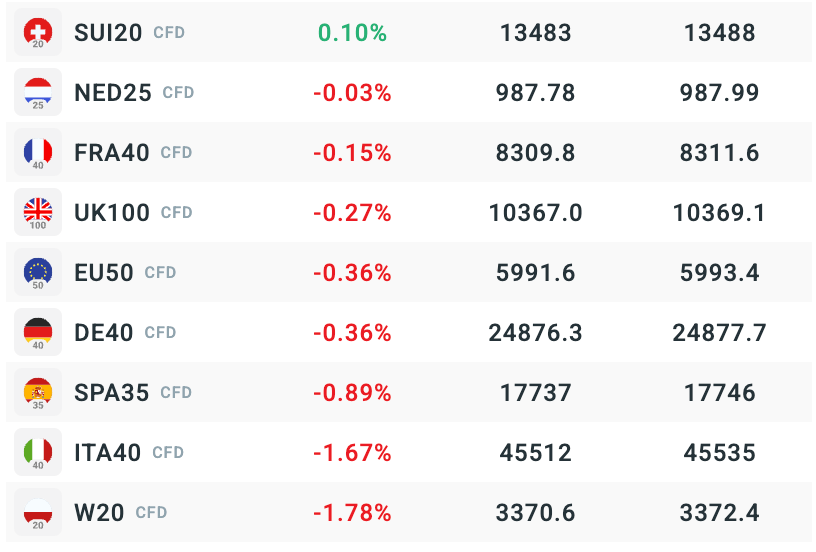

Market Sentiment: European index futures are trading mostly in the red, extending losses from yesterday's Wall Street sell-off (EU50 & DE40: -0.35%).

-

Sectors: declines are concentrated in financials, materials, energy and utilities. These are being partially offset by gains in major pharmaceutical, industrial and technology firms.

-

W20 (Poland): Leading losses at -1.8%.

-

SUI20 (Switzerland): The lone "green" exception at +0.1%.

The changes in stock index futures. Source: xStation5

Individual Stock Highlights

-

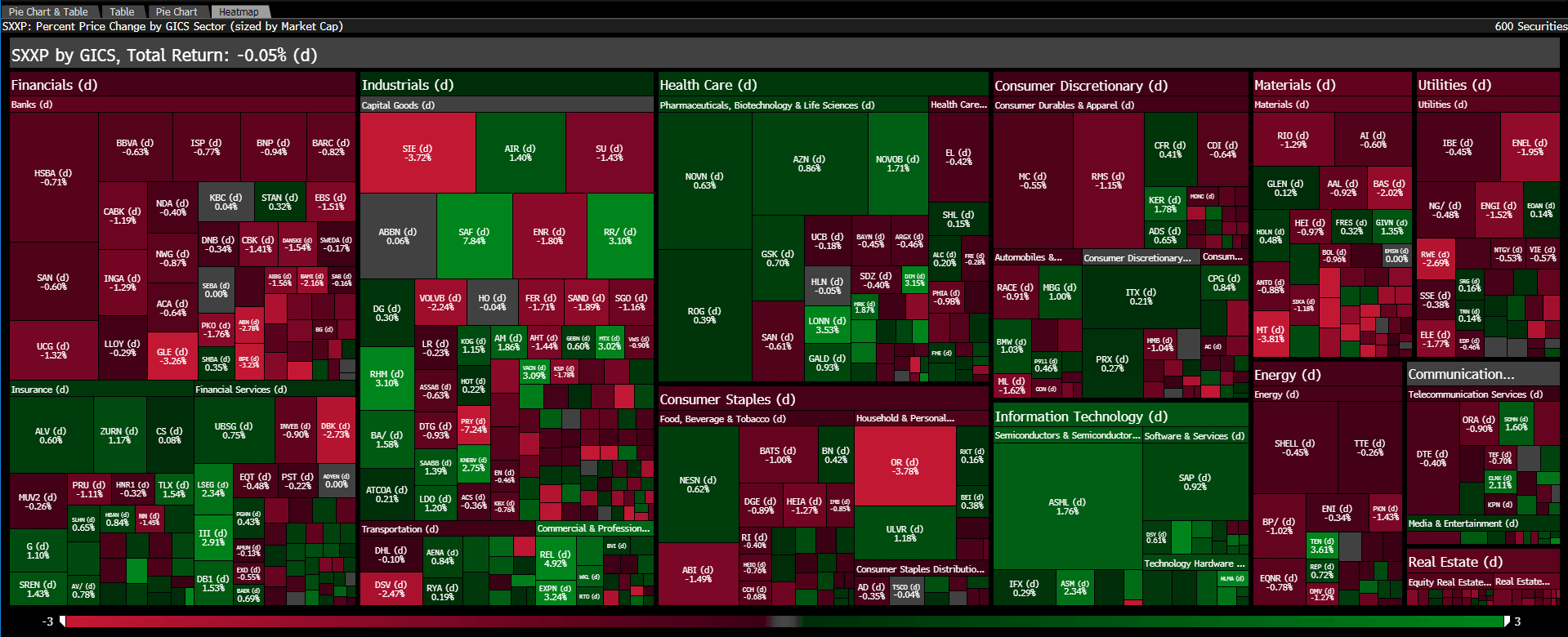

Siemens (-3.7%): Undergoing a sharp correction, completely erasing gains made after yesterday's initial positive reception of its financial results.

-

L’Oreal (-3.6%): Sliding after Q4 results showed marginal sales growth in China (0.6% vs. 5.6% forecast). Strong demand in North America and Europe (6% total growth) was not enough to satisfy investors.

-

Safran (+8.5%): Soaring after H2 2025 revenue hit €16.6 billion (+16% y/y). While EPS was softer, Free Cash Flow (€2.1 billion) significantly beat consensus. The market reacted positively to significantly raised 2028 targets.

-

Capgemini (+4.4%): Beat its 2025 revenue target (€22.47 billion) with strong Q4 growth (+10.6%) fueled by the WNS acquisition. AI-driven solutions remain the primary engine of growth, with a major restructuring planned to pivot fully toward AI services.

Today's performance of stocks and sectors of Stoxx 600 index. Source: Bloomberg Finance LP

Today's performance of stocks and sectors of Stoxx 600 index. Source: Bloomberg Finance LP

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.