- US equity futures moved higher after Donald Trump announced an indefinite extension of the ceasefire with Iran, which the market interpreted as a signal of temporarily easing geopolitical tensions. After the US session, earnings from Tesla (TSLA.US) and IBM (IBM.US) are due, while today’s macro calendar remains relatively light.

- In practice, investors responded with a modest return of risk appetite. S&P 500 futures rose 0.2%, while Nasdaq 100 futures gained 0.3%, as markets began to price in a scenario where reduced tensions could ease pressure on oil prices and support economic growth prospects.

- At the same time, the US dollar weakened, which typically reflects a partial move away from safe-haven assets as markets shift from a defensive stance toward a more cautious risk-on environment.

- It is worth noting, however, that this rebound followed a weaker session. US benchmark indices declined for a second consecutive day on Tuesday, as uncertainty surrounding US-Iran negotiations continued to weigh on investor sentiment.

- In the commodities market, conditions remained tense. Brent crude hovered around $98 per barrel, indicating that despite the short-term improvement in sentiment, markets are still pricing in a significant geopolitical risk premium related to the Middle East.

- Sentiment in Asia remained subdued. The MSCI Asia Pacific Index fell 0.7% on Tuesday, following earlier losses on Wall Street, as investors assessed how long the Middle East conflict might last and its potential impact on the global economy.

- In Europe, the outlook for the session was also cautious. Despite gains in US markets, European equities were expected to open slightly lower, suggesting that global markets are not yet treating the situation as fully resolved.

- Trump’s announcement itself was both reassuring and ambiguous. On one hand, he confirmed an indefinite extension of the ceasefire with Iran; on the other, he blamed the lack of progress in talks on what he described as a “seriously fractured” leadership structure in Tehran.

- From a market perspective, it is important that the US plans to halt further military strikes while maintaining the blockade of the Strait of Hormuz, where shipping remains heavily disrupted. For investors, this means that while military risk has temporarily eased, supply risk in the oil market has by no means disappeared.

US100 (D1)

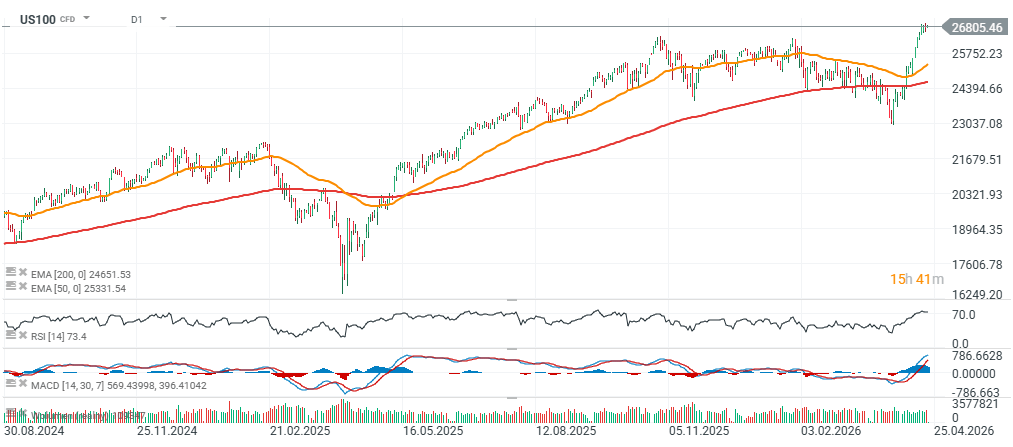

Technical indicators still point to a bullish bias, but the market has already entered overbought territory, so caution is warranted in the short term. Holding above the 9-day moving average suggests that the short-term trend remains positive. At the same time, a downside reversal signal on the daily chart slightly weakens the overall outlook. Despite this, the broader setup still favors further gains. The next upside target can be estimated around the 27,100 level. However, it is worth noting that the 9-day RSI has moved above 70, which typically signals overbought conditions and increases the risk of a correction. The nearest resistance zones are located around 26,930 and 27,100, while initial support is seen near 26,600, followed by a lower level around 26,400.

Source: xStation5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.