-

Trump has launched Operation Project Freedom, announcing that from Monday onwards there will be a “humanitarian” evacuation of neutral vessels from the Gulf of Oman and the Strait of Hormuz, whilst warning that any attempt to disrupt the convoy will be met with a “forceful” response.

-

However, the WSJ and US officials clarify that this involves a mechanism for coordinating traffic and insurers, rather than traditional US Navy ship escorts, whilst CENTCOM is simultaneously deploying destroyers to the region, over 100 ships and aircraft, and 15,000 troops to the region, which effectively increases the risk of military confrontation.

-

Iran responds sharply: Azizi, head of the parliamentary security committee, describes Project Freedom as a breach of the ceasefire and warns that Tehran will not allow the US to dictate the rules of navigation in the Strait of Hormuz.

-

In the waters of the Oman–Hormuz route, an oil tanker is struck by unidentified projectiles approximately 78 miles north of Fujairah, and the UKMTO assesses the threat level in the strait as ‘critical’, even though the Americans are establishing a ‘reinforced safety zone’ south of the Iranian TSS.

-

Fed’s Kashkari stresses that a US–Iran war and the closure of the Strait of Hormuz are increasing the risk of persistent inflation, meaning he cannot signal rate cuts and is even allowing for the possibility of a rate hike.

-

Trading in Asia is exceptionally light due to public holidays in Japan and China, with major FX pairs trading within narrow ranges; following morning volatility, USD/JPY is slowly edging higher, reflecting the broader weakening of the yen despite the recent intervention worth around $35 billion.

-

Barclays believes that the yen’s strengthening following the intervention will be temporary, as the wide US–Japan interest rate differential and high fuel prices caused by the war in Iran continue to favour a weak JPY, whilst the risk of further intervention is rising as USD/JPY returns to around 160.

-

The RBA is set to announce its monetary policy decision tomorrow, with the market pricing in a more than 75% chance of a 25-basis-point hike to 4.35%; CBA highlights that, on the one hand, inflation and the labour market remain too hot, whilst on the other, soft data (including a lower trimmed mean CPI, weaker sentiment and a cooling property market) make the decision a close call.

-

Data from the Melbourne Institute show that CPI inflation slowed to 0.6% month-on-month in April, whilst remaining stable at 4.3% year-on-year, which may temper hawkish expectations somewhat; however, the sharp rise in energy prices following the closure of the Strait of Hormuz continues to push the RBA towards a restrictive stance.

-

In the FX market, the Antipodean currencies are standing out today in terms of relative strength: the NZD is the strongest in the G-10 basket, whilst the AUD remains weaker ahead of the RBA decision; the yen is recouping some of its losses following intervention, but remains under pressure in the broader picture, whilst the USD is edging higher on growing concerns over Fed rates.

-

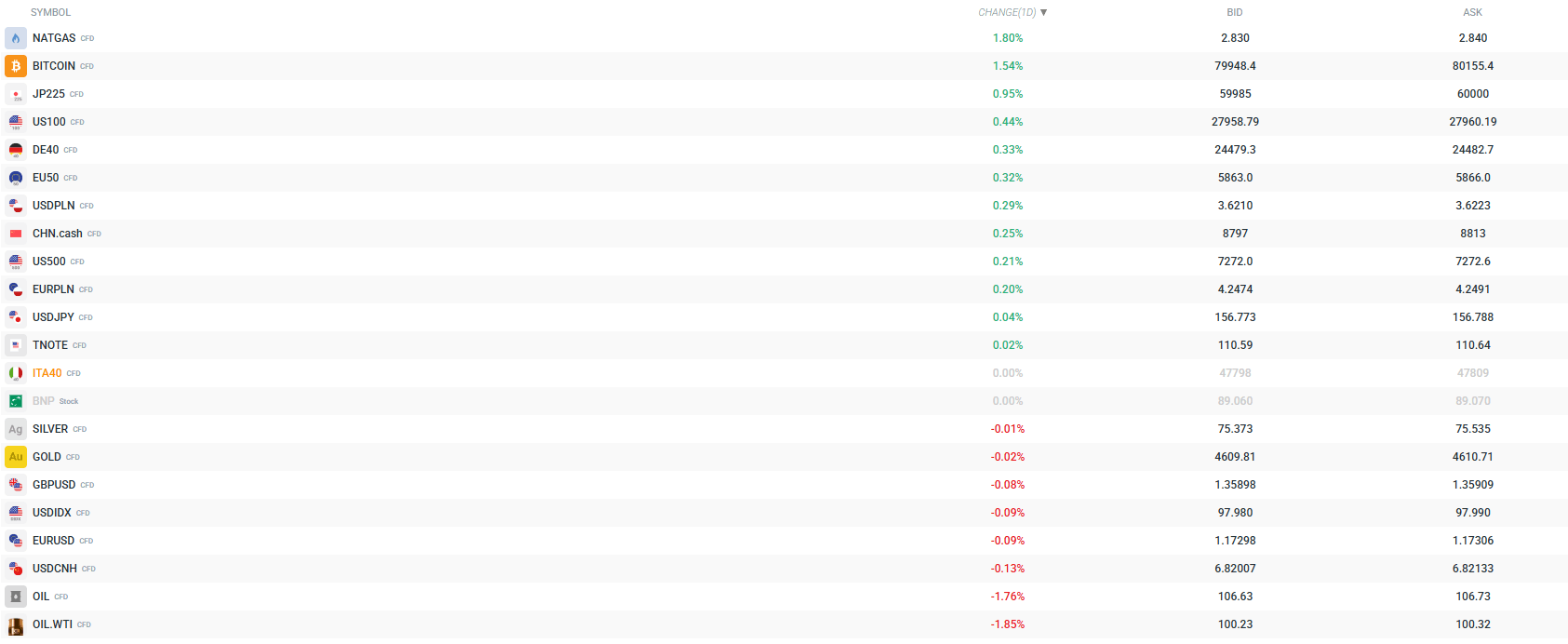

On Asian stock markets, the JP225 is up by around 0.8% amid low liquidity, whilst futures on the main US (US100, US500) and European (DE40, EU50) indices are rising slightly, signalling a cautious risk-on sentiment despite geopolitical tensions.

-

The energy market remains tense: Brent and WTI crude are edging lower following earlier gains, but the market is pricing in a high risk of further rises should Iran attempt to disrupt US convoys in the Strait of Hormuz; natural gas is up by over 2%, reflecting concerns over supply.

-

Among precious metals, gold is falling slightly and silver remains weaker, which could be interpreted as a temporary respite following the flight to ‘safe havens’, but the price trajectory will depend heavily on whether Project Freedom leads to further incidents in the strait.

-

Bitcoin has broken above $80,000 for the first time since late January, emerging as one of the few clear ‘risk-on’ signals of the session and attracting demand in a market environment where traditional asset classes are being held back by geopolitical risks and hawkish central banks.

-

At the start of the European session, the following factors will be key to market sentiment: the initial reaction of the oil market to the operational details of Project Freedom, any comments from Iran interpreting the plan as an actual breach of the ceasefire, and the final positioning ahead of tomorrow’s RBA decision, which could set a precedent for further decisions by central banks grappling with ‘war-driven’ inflation. On the macro data front, it is worth keeping an eye on the incoming PMI reports for manufacturing from the major European economies and durable goods orders from the US.

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.