Just days after the August non-farm payrolls (NFP) report, the Bureau of Labor Statistics (BLS) is set to release its annual revision of employment growth for the period from April 2024 to March 2025. This revision will cover only two months of Donald Trump’s presidency. The report could further intensify expectations for a rate cut, with some even pointing to the possibility of a 50-basis-point (bp) reduction. Initial economist expectations suggest one of the largest declines in employment compared to original estimates, although it is likely to be a smaller drop than last year.

The mechanism and scale of the expected revision

The annual NFP revision is a standard process in which the BLS validates its monthly estimates against more complete data from the Quarterly Census of Employment and Wages (QCEW), which is derived from unemployment insurance records and covers over 95% of all jobs. This process allows for the inclusion of more accurate data on new business formations and closures, which are not available when the monthly reports are first published.

Economists forecast a significant downward revision in employment for the April 2024 to March 2025 period. According to a Bloomberg Intelligence report, market expectations range from approximately 500,000 to 800,000 jobs, though some forecasts even suggest a downward revision of 1 million jobs. Bloomberg Economics suggests a slightly smaller correction.

Market Expectations:

-

Bloomberg Economics: -555,000 jobs (range of -475,000 to -714,000)

-

Wells Fargo: -475,000 to -790,000 jobs

-

Nomura Securities: -600,000 to -900,000 jobs

-

Bank of America and Royal Bank of Canada: Up to -1 million jobs

An analysis by Bloomberg Economics indicates that the first quarter of 2025 saw an improvement, with a reduction in business closures and an increase in new business formations. This accounts for the more moderate downward forecast compared to some market consensus figures.

What's behind the employment revision?

Reasons for the revision: The main reason for the predicted correction is the BLS's "birth-death" model, which likely overestimated the number of jobs created by new businesses. High-frequency indicators suggest that the rate of new business creation hit its lowest point in the second quarter of 2024 before improving in the first quarter of 2025.

Improvement in Q1 2025: A key takeaway is that data for the first quarter of 2025 may show a stabilization of the labor market. Bloomberg Economics expects that QCEW employment growth in Q1 2025 (relative to Q4 2024) will not be significantly slower than the CES survey, which explains their more moderate revision forecast compared to the market consensus.

Historical implications: After the revision, employment in October 2024 may have actually fallen by 3k jobs, which, in retrospect, would justify the Fed's decision to cut rates by 50 basis points in September 2024.

A repeat of 2024?

In August 2024, the BLS published a revision showing that the economy had created 818,000 fewer jobs than originally estimated for the April 2023 to March 2024 period. The final revision, released in February 2025, was lowered to 598,000 jobs. In response to this revision and other weakening labor market data, the Fed opted for a 50-basis-point rate cut in September 2024. However, it is important to note that the revision at the time did not lead to significant recessionary fears, as a downward revision of over 1 million jobs had been anticipated.

Current market expectations for a rate cut

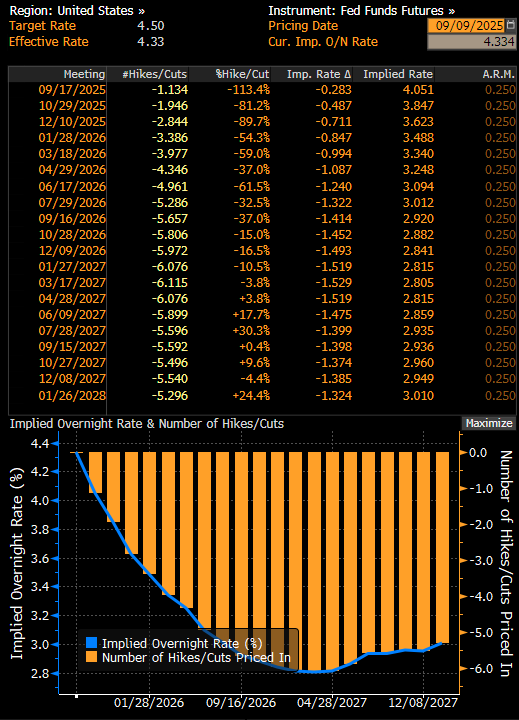

Following a weak August 2025 NFP report, which showed an increase of only 22,000 jobs—well below the already low expectation of 75,000—markets are fully pricing in a rate cut at the Fed's meeting next week. The unemployment rate has risen to 4.3%.

The market is currently pricing in not only a full 25-bp cut on September 17, but also a 13% chance of a 50-bp cut. Another full cut is expected in October, with a third nearly fully priced in for December. Standard Chartered anticipates that a significant negative NFP revision could tip the scales toward a larger 50-basis-point cut.

Source: Bloomberg Finance LP

Sectors most affected by the revision

Based on analyst expectations and the precedent from 2024, the largest negative revisions are expected in professional and business services, where last year's revision reached almost 360,000 jobs. The next key sector is leisure and hospitality, which saw a revision of 150,000 jobs last year. On the other hand, positive revisions are anticipated in private education, healthcare, and even government employment.

What about the markets?

A significant negative NFP revision would strengthen the narrative of a weakening labor market. However, Bloomberg Economics' analysis suggests a more moderate view. If the data confirms improvement in the first quarter of 2025, the Fed may interpret the situation as a temporary softening that is nearing its end. On the other hand, the latest data from recent months has already been revised significantly downward, and we experienced a decline in employment in June.

For markets, a strong revision, larger than last year's, could mean a clear weakening of the dollar, a drop in yields, and a continued rise in gold prices. The reaction in the stock market is not as clear-cut; while a decline in employment would mean rate cuts—which are good for stocks—recessionary signals are not as positive for the market.

Gold has reached historical highs due to rising expectations for cuts. Source: xStation5

Gold has reached historical highs due to rising expectations for cuts. Source: xStation5

Political context and data credibility

The revision also has a political dimension. President Trump has previously questioned the credibility of BLS data, and in August 2025, he fired BLS commissioner Erika McEntarfer following the release of weak data for July. Trump accused the BLS of "falsifying" the data, though economists emphasize that revisions are a normal part of the process of refining economic data.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.