The user wants to quickly identify the world's largest oil-producing countries and companies in one place. The article solves the need for a reliable, scannable reference - combining a country-level ranking with a company-level overview for readers researching global oil markets or considering investment exposure to theenergy sector.

The user wants to quickly identify the world's largest oil-producing countries and companies in one place. The article solves the need for a reliable, scannable reference - combining a country-level ranking with a company-level overview for readers researching global oil markets or considering investment exposure to theenergy sector.

The United States is the world's largest oil producer, pumping more crude than any other nation on Earth. With global energy markets shaped by a handful of dominant players, understanding who produces the most oil - and which companies sit behind that output - is essential context for any investor watching commodity markets. Below, we break down the top oil-producing countries and the biggest oil companies driving global supply.

Key Takeaways

- Global oil supply is concentrated, with the United States, Saudi Arabia, and Russia playing the most important roles in overall market balance.

- The sector is dominated by a mix of state-owned companies such as Saudi Aramco, ADNOC, and PetroChina, and publicly listed majors such as ExxonMobil, Shell, BP, Chevron, and TotalEnergies.

- Production profiles differ significantly: U.S. shale is flexible, while producers such as Canada, Iraq, and Iran are more constrained by capital intensity, fiscal dependence, or sanctions.

- Geopolitics remains central to oil markets, especially for exporters exposed to chokepoints, sanctions, and infrastructure disruption.

How Oil Production Shapes Gobal Markets

Global oil markets are heavily influenced by a small group of producing countries and energy companies that control a large share of the worldwide supply. Oil price impacts energy prices, inflation, transport costs and even investor sentiment. Because supply is concentrated among major producers such as the United States, Saudi Arabia and Russia even small changes in

output can affect fuel prices, industrial costs, and expectations for global economic growth. The market is also heavily influenced by large energy companies including Saudi Aramco,

ExxonMobil, Chevron, Shell and BP whose production decisions and investment strategies help shape global supply trends.

Supply uncertainty has the strongest market impact as OPEC+ cuts, sanctions, shipping-route conflicts or infrastructure disruptions can quickly reduce avaliable barrels and increase price

volatility. Because oil prices affect fuel, transport, manufacturing costs, inflation and consumer sentiments, production levels of the leading oil countries and producers are closely watched not only by energy investors, but also by airlines, shipping giants, industrial companies and central banks like Fed or ECB.

Which Countries Produce the Most Oil?

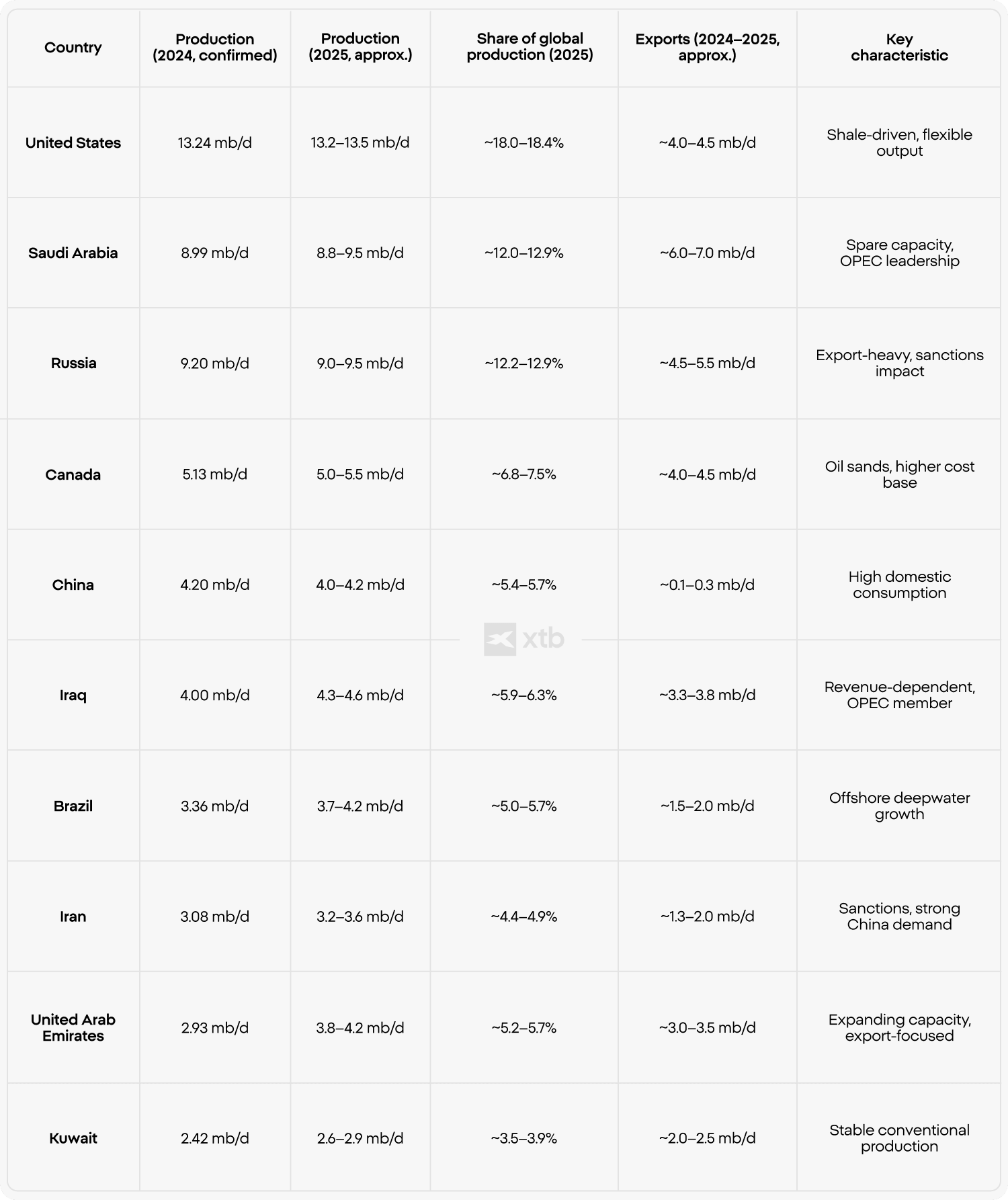

The ranking of the top oil producing countries is based on daily output measured in barrels per day (bbl/d), using estimates from sources such as the EIA, OPEC, and IEA. Here is the table

with both 2024 confirmed data and 2025 approximations, using consensus ranges from EIA, OPEC, and national sources. The shares for 2025 are calculated against an estimated ~73.5mb/d global crude supply baseline (rounded industry consensus for 2025). Oil exports by country differ. Sometimes countries producing less oil export more than bigger ones. Here is the breakdown of the world’s largest oil producers by share of global oil production:

- United States approx. 18.0 - 18.4%

- Saudi Arabia approx. 12 - 12.9%

- Russia approx. 12.0 - 12.9%

- Canada approx. 6.8 - 7.5%

- United Arab Emirates approx. 5.2 - 5.7%

- China approx. 5.4 - 5.7%

- Iraq approx. 5.9 - 6.3%

- Brazil approx. 5 - 5.7%

- Iran approx. 4.4 - 4.9%

- Kuwait approx. 3.5 - 3.9%

Identifying the largest oil producer in the world should always be understood as an approximation based on standardized reporting. Despite these nuances, global production

remains highly concentrated among a relatively small group of countries. For example the Middle Eastern countries produced appx. 32% of global crude oil in 2025.

A limited number of oil producing countries accounts for a substantial share of global supply, which increases the market impact of changes in their output. The United States, Saudi Arabia,

and Russia consistently dominate production volumes, while countries such as Canada, Iraq, and China add significant contributions.

The biggest oil producers: Breakdown by country

To better understand how these countries contribute to global supply, it is essential to examine their structural characteristics - and in doing so, approach how you invest in oil with a clearer

perspective.

United States: scale and flexibility define its dominance

The U.S. remains the world’s largest oil producer in the world with oil production output at ~13 million bbl/d. The production is led by the Permian Basin region and supported by Gulf

of Mexico output. The country is also one of the biggest oil exporters. Its shale model enables relatively fast supply responses due to shorter investment cycles and continuous drilling activity. In recent years, a renewed “drill baby drill” approach has supported production resilience, though within a more capital-disciplined framework focused on free cash flow and shareholder returns.

Geography further strengthens the U.S. position. Unlike Gulf producers, it faces no critical chokepoints such as Hormuz or Bab al-Mandeb, allowing more secure export routes. Access to

both the Atlantic and Pacific, supported by the Panama Canal, enhances logistical flexibility, particularly for flows to Asia. Major importers of U.S. crude include Europe, China, India, and

South Korea. As exports rise, the U.S. increasingly acts as a marginal supplier, partially offsetting disruptions from the Middle East.

Saudi Arabia: low-cost leader with strategic spare capacity

Producing ~10–11 million bbl/d, Saudi Arabia is the largest oil exporter in the world combining scale with some of the lowest lifting costs globally, supported by Saudi Aramco. Its key advantage is significant spare capacity, allowing it to actively manage supply within OPEC and influence global oil prices. As of 2026, the Iran-related tensions have increased the

strategic value of this flexibility. To hedge against disruption in the Strait of Hormuz, Saudi Arabia relies on the East–West pipeline, with capacity of ~7 million bbl/d, enabling crude transport to the Red Sea and bypassing regional chokepoints. The conflict in the Gulf will not last forever and any hit to infrastructure may be rebuilt over time. The country still has a potential to export more oil in the future.

Russia: large-scale producer reshaped by sanctions

Russia produces ~9.5–10.5 million bbl/d and remains central to OPEC+. Its main export blend, Urals, typically trades at a discount to Brent. After 2022 sanctions, exports shifted sharply

toward Asia. China now absorbs ~51% of Russian exports and accounted for ~17% of its oil imports in 2025. Russia also expanded flows to BRICS countries, while exports to Europe have

become marginal. Infrastructure risks persist, with Ukrainian drone attacks periodically disrupting Baltic export terminals.

Canada: high output with structural rigidity

At around 5.5 million bbl/d, Canada is one of the world’s biggest oil producers, with output largely driven by Alberta’s oil sands. That gives it a large and relatively stable production base, but also makes it less flexible than shale-focused producers like the United States. Oil sands projects need high upfront spending, long development periods, and constant infrastructure investment, so output cannot be raised or cut quickly when prices move. Because of that, Canada supports global supply mainly through long-term stability rather than rapid market response during disruptions or volatility.

Iraq: high production with fiscal dependence

Producing roughly 4.5 million bbl/d, Iraq remains one of the Middle East’s key oil suppliers. Output is concentrated in a small number of giant fields, which helps scale but also increases

reliance on infrastructure security, export routes, and political stability. That concentration means operational or geopolitical disruptions can have a disproportionate impact on production.

Iraq’s oil sector is also deeply tied to the state, with more than 90% of government revenue coming from oil. This leaves the country highly exposed both to supply interruptions and to

swings in crude prices. Iraq is therefore a major oil producer, but its market role is closely linked to fiscal fragility and regional risk.

China: large producer focused on domestic demand

China produces about 4.0 million bbl/d, making it one of the world’s largest producers in absolute terms. But unlike major exporters, most of this oil is used at home rather than sold

abroad. That limits China’s influence on the export side of the global market, even though it remains highly important through its import demand. Domestic production helps reduce reliance

on foreign suppliers and supports energy security, a core priority for Beijing. In this sense, China’s oil sector matters less as an export force and more as a stabilising part of domestic

economic and industrial policy.

United Arab Emirates: expanding capacity for future growth

With production of roughly 3.5 to 4.0 million bbl/d, the UAE is positioning itself as one of the Gulf producers with the clearest long-term growth ambitions. Unlike countries mainly focused on

maintaining current output, the UAE continues to invest in expanding capacity to strengthen its future export role and increase its influence within OPEC. This is important because additional

UAE capacity can improve the group’s ability to respond to demand shifts or disruptions elsewhere. Combined with relatively low-cost production and an increasingly investment-led

energy strategy, the UAE is more than just a stable producer. Its growing importance reflects both current export potential and a long-term push for greater weight in global crude markets.

Brazil: offshore growth powered by pre-salt reserves

Brazil produces around 3.5–4.0 million bbl/d, with much of its growth coming from offshore pre- salt fields. These reserves have reshaped the country’s role in the oil market, making it one of

the most important non-OPEC growth stories in recent years. Offshore projects are technically complex and capital-intensive, but advances in drilling and efficiency have made deepwater

production more competitive. Brazil is not a fast-response producer like U.S. shale, yet it remains a meaningful source of long-term supply growth outside the traditional Middle Eastern

core. As pre-salt development continues, Brazil is playing a larger role in diversifying global oil supply.

Iran: geopolitical risk and China dependence

Iran produces ~3.0 million bbl/d, but export volumes fluctuate due to sanctions. China is by far its largest buyer, importing ~1.38 million bbl/d in 2025 (Kpler), or roughly 75–90% of Iran’s

exports. In early 2026, flows rose close to 2 million bbl/d. Discounted Iranian crude accounts for ~13% of China’s seaborne imports. However, export outlook remains uncertain due to the 2026 Strait of Hormuz tensions, naval disruptions, and damage to refining and export infrastructure

following Israeli and U.S. strikes.

Kuwait: producer aligned with OPEC policy

Kuwait produces roughly 2.5–3.0 million bbl/d from large conventional reserves and has historically aligned output closely with OPEC policy, reinforcing its status as a stable supplier.

As of April 2026, however, the Iran conflict has shifted the main risk from production to exports. OPEC+ had planned to raise output from April, but Hormuz disruptions forced Kuwait to cut

production as storage filled up, while force majeure was declared on some shipments. This shows how even reliable Gulf producers remain highly exposed to regional chokepoints and

war-driven logistics shocks.

Who Are the Largest Oil Companies in the World?

The largest oil companies are responsible for transforming underground resources into usable energy, and their scale can be assessed through revenue, production, and reserves. The

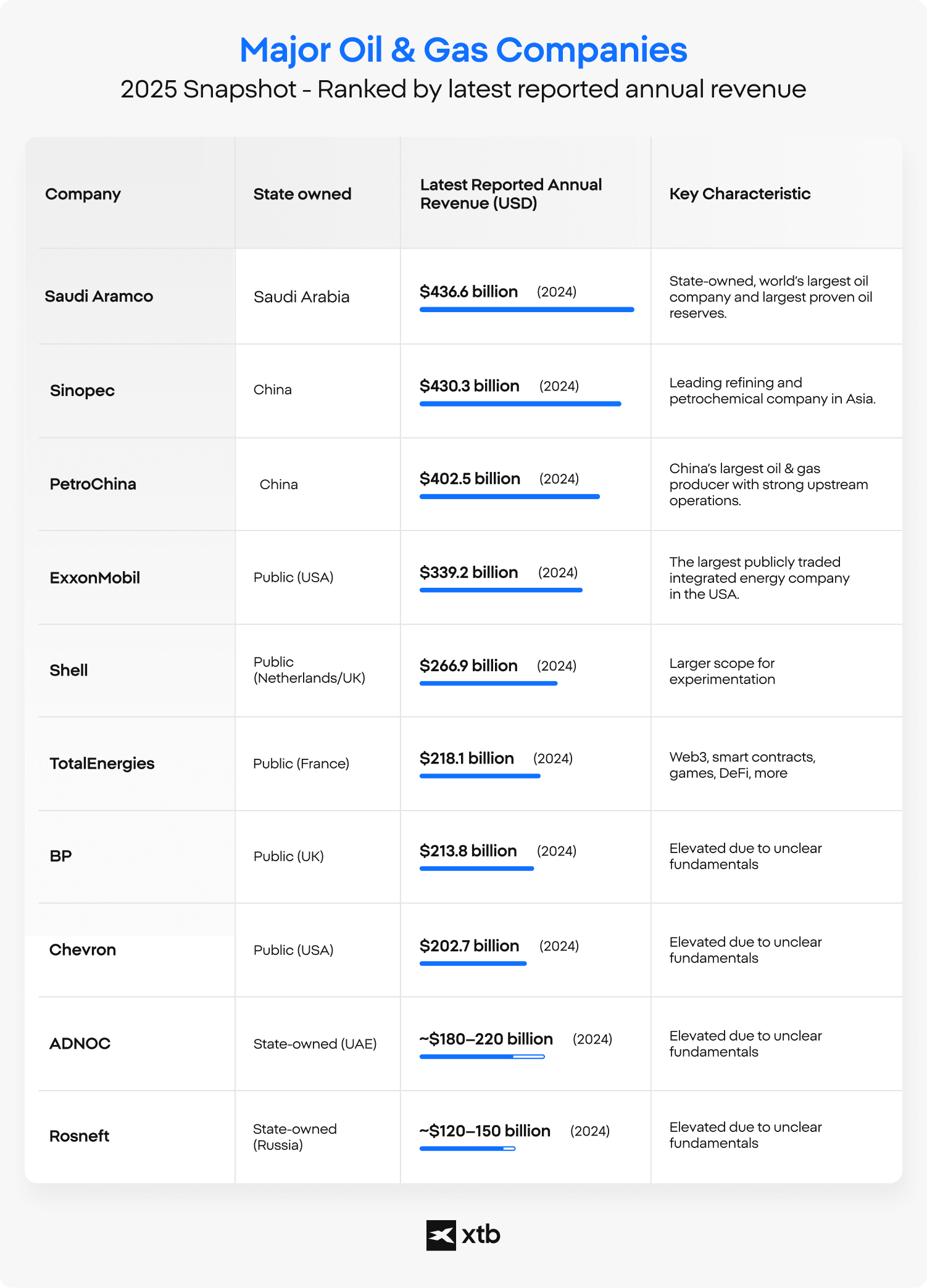

biggest oil producers at the corporate level include both state-owned companies and publicly listed firms, each operating under different strategic priorities. Below is a simplified comparison of major oil companies and their approximate annual revenues based on recent financial disclosures:

Source: Companies Annual Reports

While national companies often focus on resource management and long-term supply, listed companies balance production with financial performance and shareholder expectations. This distinction influences how companies respond to changes in oil prices and global demand. State-controlled firms dominate the upper end of the global ranking in terms of reserves and

production capacity, while international companies often lead in operational diversification and geographic reach.

Companies such as Saudi Aramco, ADNOC, and PetroChina are closely tied to national production strategies. In contrast, firms like ExxonMobil, Shell, BP, and Chevron operate across

multiple regions and segments of the energy value chain. Together, these entities form the backbone of global oil supply infrastructure.

Saudi Aramco

Saudi Aramco is the world’s largest oil producer and the backbone of Saudi Arabia’s economy, combining unmatched scale with some of the lowest production costs globally. Its upstream

dominance allows it to generate strong cash flows even in low-price environments, making it structurally different from Western majors that rely more on diversification.

The company is less exposed to shareholder pressure and energy transition risks, but more tied to geopolitical dynamics and OPEC+ policy decisions. Aramco’s downstream expansion and

investments in petrochemicals aim to extend the value chain and stabilize revenues. For investors, it represents a pure-play on global oil demand with sovereign backing, rather than a

balanced energy transition story.

ExxonMobil

ExxonMobil stands out for its disciplined capital allocation and strong focus on high-return upstream projects, particularly in Guyana and the Permian Basin. Unlike some peers, it has

taken a more measured approach to the energy transition, prioritizing profitability over aggressive renewables expansion. Its integrated mode - spanning upstream, refining, and chemicals provides resilience across different market cycles. Exxon’s scale and technical expertise allow it to execute complex, long- cycle projects with high efficiency. For investors, it is often seen as a “quality compounder” in the oil space, emphasizing returns and operational excellence over transformation narratives.

Shell

Shell differentiates itself through its aggressive pivot toward LNG and integrated gas, positioning it as a key player in the global energy transition. The company has also invested heavily in

renewables and power trading, although it has recently recalibrated its strategy toward higher returns. Compared to Exxon or Chevron, Shell has a more diversified energy mix and greater exposure to electricity markets. Its global trading arm is one of the strongest in the industry, providing additional earnings stability. For investors, Shell offers a hybrid profile - part traditional oil major, part evolving energy company.

PetroChina

PetroChina is one of China’s largest state-controlled oil and gas companies, focused on ensuring domestic energy security. Its strategy is closely aligned with government policy, which

can limit flexibility but ensures long-term demand stability. Compared to Western majors, it offers less transparency and is more exposed to regulatory and political influence.

Sinopec

Sinopec is primarily a downstream and refining giant, making it structurally different from upstream-heavy peers like Exxon or Aramco. Its earnings are more sensitive to refining margins

and domestic Chinese demand rather than global oil prices alone. Like other Chinese SOEs, it operates within a state-driven framework, prioritizing stability over shareholder returns.

BP

BP has positioned itself as one of the most transition-focused oil majors, with significant investments in renewables, hydrogen, and EV charging. This strategy differentiates it from more

hydrocarbon-focused peers but has also raised concerns about returns and execution risk.

BP’s portfolio is more balanced between upstream and downstream, though less dominant in either compared to Exxon or Shell. The company has undergone major restructuring since the

Deepwater Horizon spill, shaping a more cautious operational culture. For investors, BP represents a higher-risk, higher-transition exposure within the oil sector.

Chevron

Chevron is often seen as the most conservative and operationally disciplined of the US majors, with a strong focus on capital efficiency and shareholder returns. Its upstream portfolio is heavily weighted toward short-cycle assets like the Permian Basin, giving it flexibility in volatile markets.

Unlike BP or Shell, Chevron has taken a slower approach to energy transition investments, prioritizing core oil and gas profitability. The company’s balance sheet strength and consistent dividend policy make it attractive for income-focused investors. Chevron offers a more predictable, lower-volatility exposure compared to its peers.

TotalEnergies

TotalEnergies has emerged as Europe’s most balanced energy major, combining strong oil and gas operations with a rapidly growing renewables portfolio. It has a leading position in LNG,

similar to Shell, but with a more aggressive push into solar and wind. The company’s strategy aims to diversify revenue streams while maintaining profitability from hydrocarbons. Compared

to BP, TotalEnergies has been more disciplined in managing the pace of its transition. For investors, it offers a blend of income, growth, and exposure to the energy transition.

ADNOC

ADNOC is the UAE’s national oil company, combining low-cost upstream production with a rapidly expanding downstream and petrochemical footprint. Its strategy focuses on maximizing

value from hydrocarbons while selectively investing in future energy solutions. ADNOC benefits from strong state backing and access to some of the world’s most cost-efficient reserves. The

company has also become more investor-friendly through partial listings and partnerships. For investors, it represents a Middle Eastern growth story with increasing integration into global

capital markets.

Rosneft

Rosneft is Russia’s largest oil producer and a key pillar of the country’s energy sector. Its operations are heavily influenced by geopolitical factors and sanctions, which significantly

impact its investment profile. Compared to Western majors, it offers scale but comes with elevated political and regulatory risk.

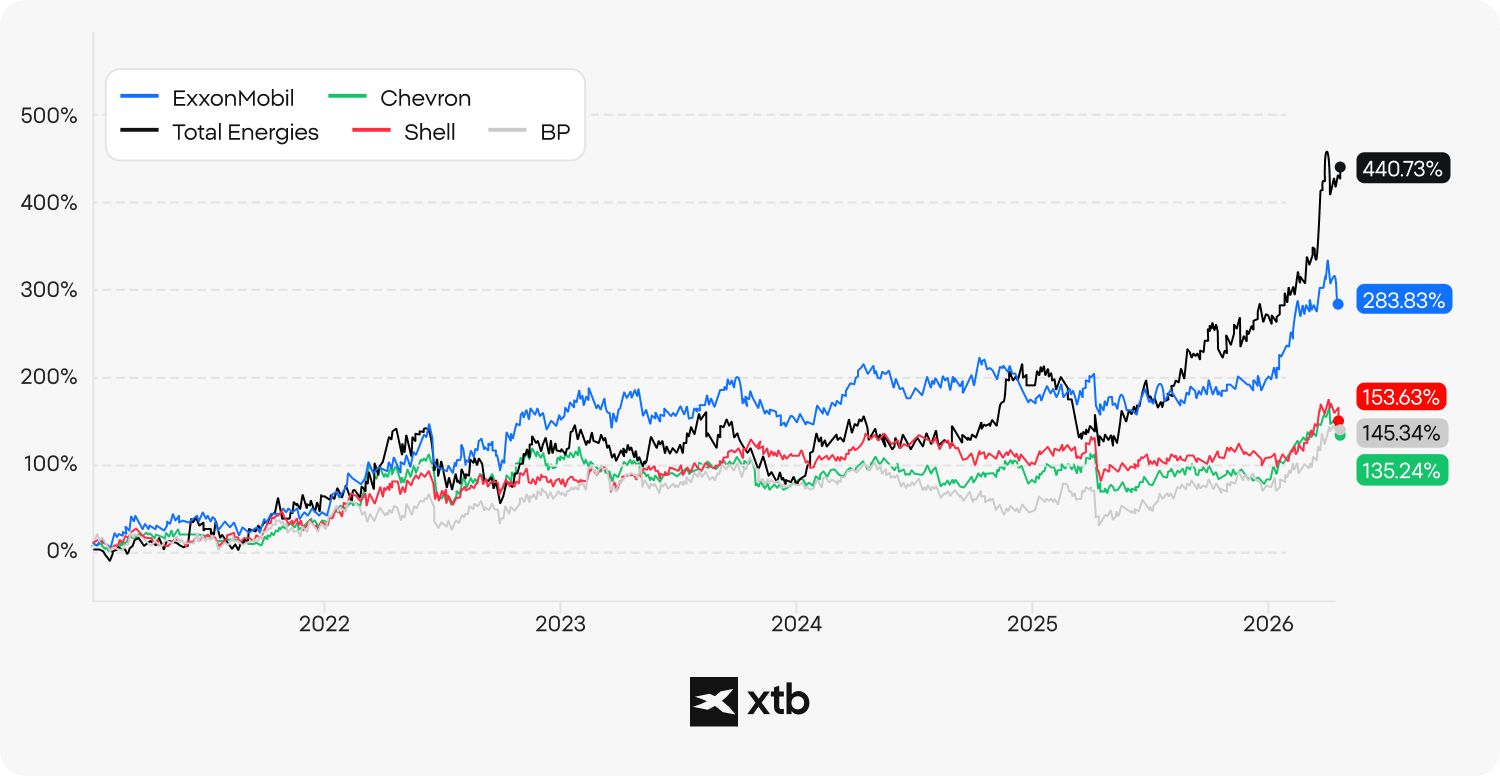

As we can see on the chart below as of April 2026, each oil company surged from 135% for Chevron to almost 440% for Total Energies in the last 5 years. Each of those stocks significantly

outperformed S&P 500 and Nasdaq 100 return on investment in a given period.