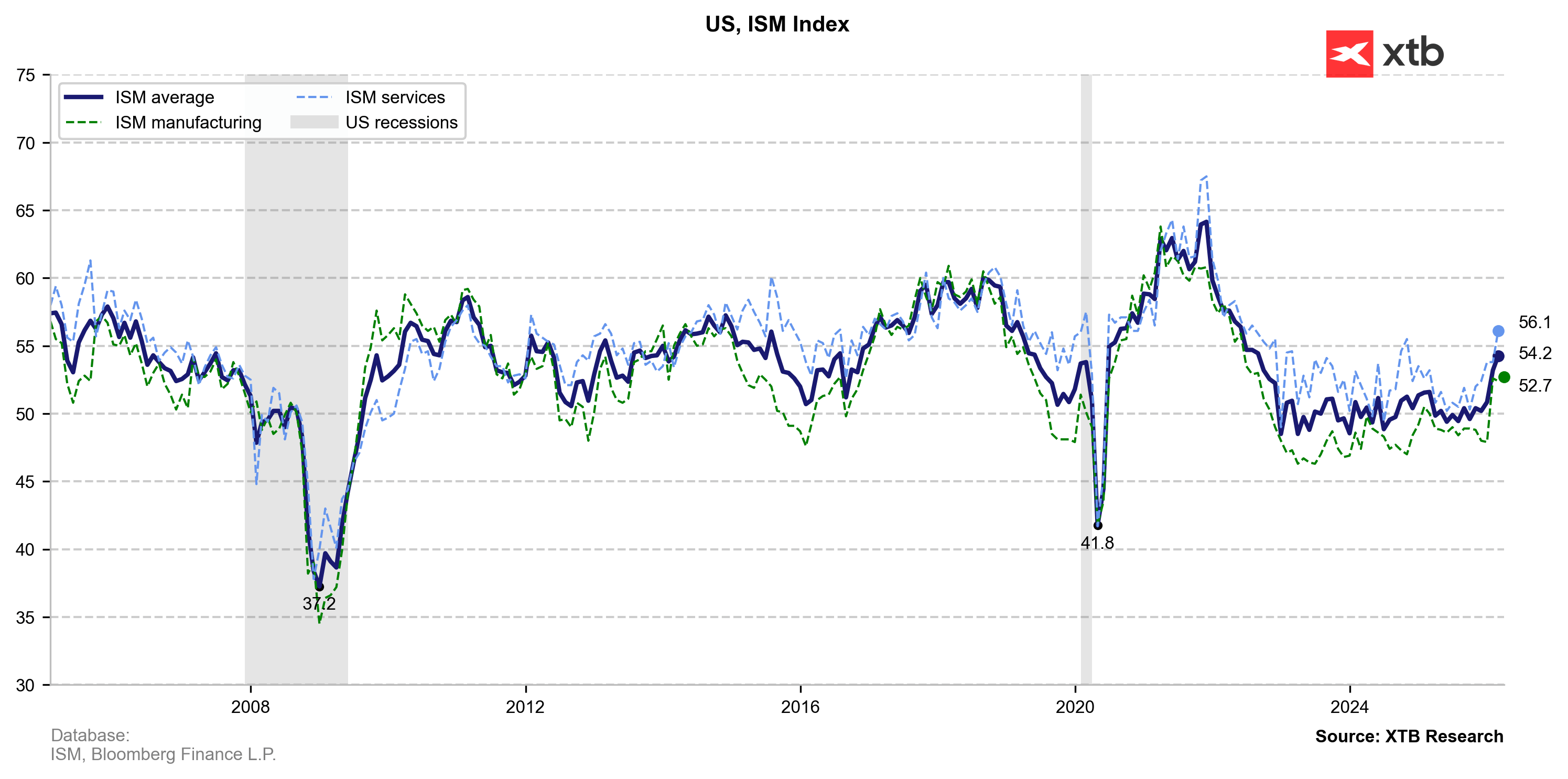

The headline index of 52.7 (vs. 52.5 expected and 52.4 previously) marks the third consecutive month of expansion, but the report’s internal details are cooling market enthusiasm.

-

Inflationary Shock (Prices Paid: 78.3 vs. 73.0): This is the report’s critical takeaway. Input costs are rising at their fastest pace since mid-2022. Such intense price pressure (commodities, tariffs) is a major "red flag" for the Fed, pushing back the timeline for potential rate cuts, altough the market is pricing only 20-30% probability of interest hike this year.

-

Sustained Recovery (Headline PMI: 52.7): Manufacturing has definitively moved past the 2025 slump. The U.S. economy's resilience provides the Fed with more room to maintain its restrictive monetary policy.

-

Waning Demand Momentum (New Orders: 53.5): While orders are still growing, the pace has decelerated compared to February (55.8). This suggests that the initial wave of New Year optimism and restocking is beginning to fade.

-

Weak Labor Demand (Employment: 48.7): Despite rising production, the sector remains in contraction territory regarding hiring (reading below 50). Firms may be pivoting toward automation or trimming labor costs to offset soaring material prices.

This report is decidedly hawkish, especially looking from the inflation side. The combination of robust growth and a massive spike in input costs should support the US Dollar and Treasury yields while weighing on tech valuations (US100). The "higher for longer" interest rate scenario has just become even more plausible.

Of course, EURUSD is responding to the hope that the conflict in the Middle East will end soon. Decreasing risk in negative for the US dollar and the EURUSD is once again above 1.16, breaking above the downward trend line.

Daily summary: Dollar rout after NFP, Gold back on the rise

The dollar sinks after labor market data💲📉

NFP much below expectations! 🚨EURUSD spikes 📈

Dollar and Nasdaq facing a key test