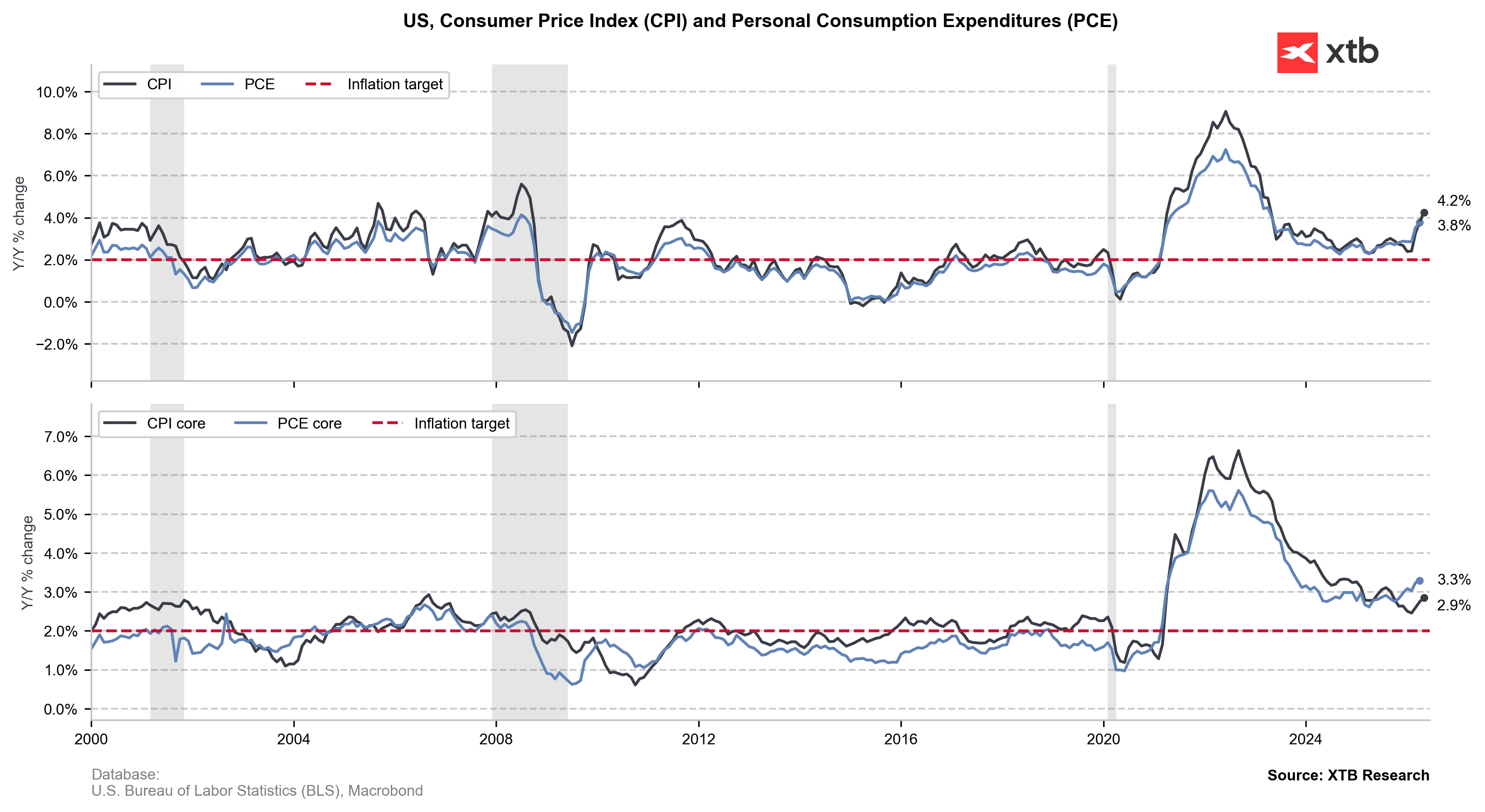

Consumer Inflation (CPI) – USA

-

CPI Inflation (m/m): 0,5%;forecast 0.5% (previously 0.6%)

-

Core CPI Inflation (m/m): 0,3% ;forecast 0.3% (previously 0.4%)

-

CPI Inflation (y/y): 4,2% ;forecast 4.2% (previously 3.8%)

-

Core CPI Inflation (y/y): 2,9%;forecast 2.9% (previously 2.8%)

Why is this data important?

Consumer inflation (CPI) is the most important indicator measuring the pace of price growth for goods and services from the consumer’s perspective. It shows how the cost of living for households is changing and serves as a key reference point for the monetary policy of the Federal Reserve (Fed).

A higher-than-expected CPI reading suggests persistent inflationary pressure in the economy, which may increase the likelihood of interest rates remaining higher for longer or even further monetary tightening. On the other hand, weaker data may support expectations for interest rate cuts and a more dovish Fed stance.

Particularly important is Core CPI inflation, which excludes the most volatile components such as food and energy. This provides a clearer picture of long-term inflation trends and is closely monitored by the central bank.

The CPI report has a major impact on financial markets. Higher inflation typically supports the U.S. dollar and pushes Treasury yields higher, as investors anticipate a more restrictive Fed policy. Conversely, lower-than-expected inflation data may weaken the dollar, support equity markets, and increase expectations for future rate cuts.

Actual Data

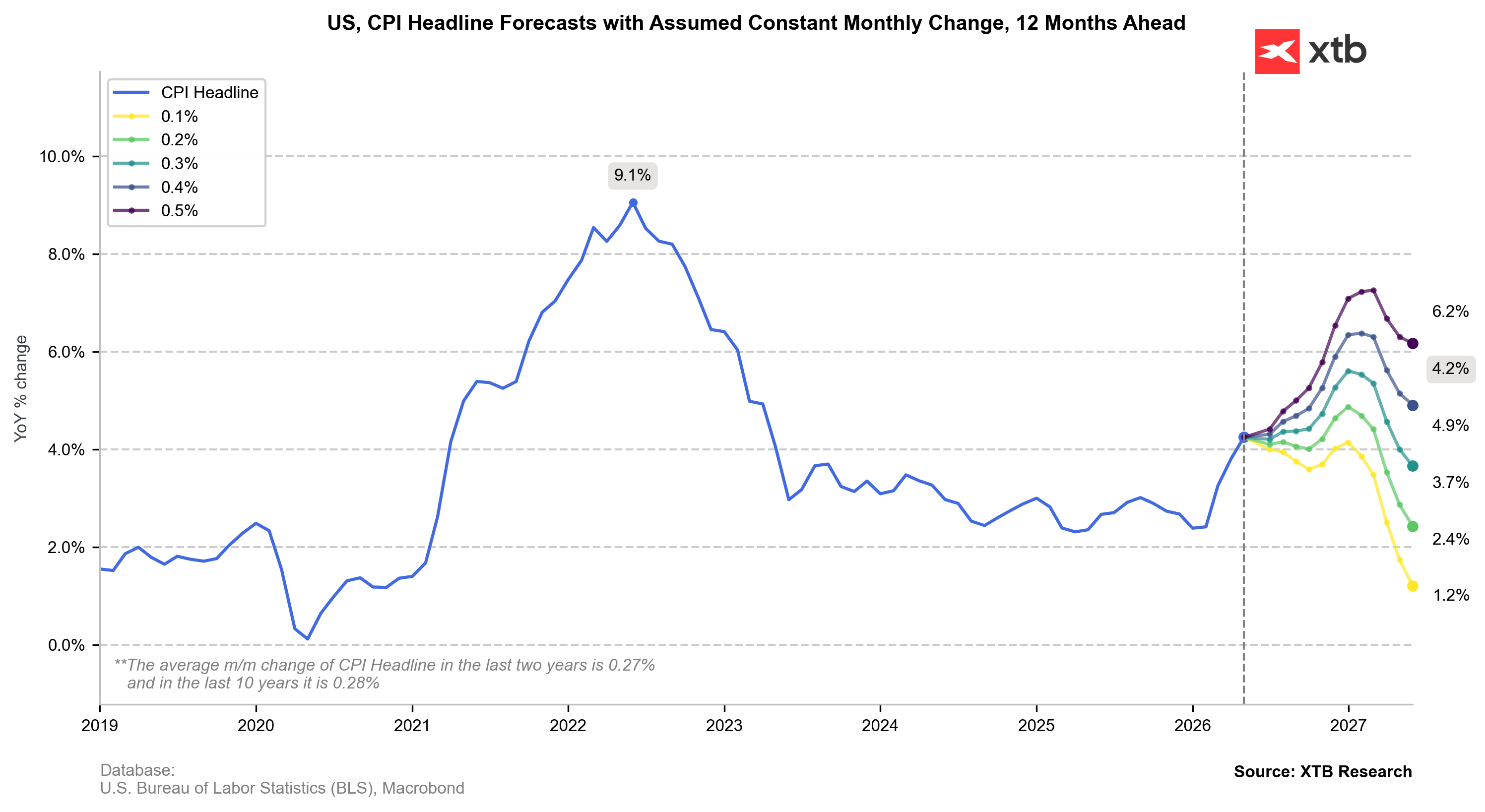

The US CPI data confirms that inflation remains relatively elevated and continues to sit well above levels consistent with a comfortable policy easing cycle from the Federal Reserve.

Headline CPI came in at 0.5% m/m, in line with expectations but still reflecting persistent short-term price pressures. While the reading did not come as a surprise versus consensus, it reinforces the fact that inflation momentum remains firm and is not meaningfully cooling on a monthly basis.

On a year-on-year basis, CPI accelerated to 4.2% from 3.8% previously, highlighting that base effects are no longer providing disinflationary support. Instead, inflation is stabilising at an elevated level, which stands in clear contrast to any narrative suggesting a rapid return towards the Fed’s 2% target.

Core CPI also remains sticky. Monthly core inflation printed at 0.3%, fully in line with expectations, but still consistent with an underlying pace that is too high to justify near-term rate cuts. On a yearly basis, Core CPI rose to 2.9% from 2.8%, signalling a modest re-acceleration in underlying price dynamics.

The key takeaway for markets is not the absence of a surprise versus consensus, but the absolute level of inflation. Price pressures remain too high to justify any credible expectation of imminent interest rate cuts from the Federal Reserve.

Source: xStation5

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR