1. Bank of Japan: Ueda’s Hawkish Signal Bolsters Yen Despite Energy Shock

The Governor of the Bank of Japan (BoJ), Kazuo Ueda, surprised markets with a hawkish tone, leaving the door open for an interest rate hike as early as April. Although the BoJ held its benchmark rate at 0.75% today, Ueda’s remarks—suggesting that the economic impact of the war might be transitory and unlikely to derail the inflation trajectory—pushed market expectations for a hike to approximately 60%.

This rhetoric triggered an immediate appreciation of the Yen. However, a critical question remains: can the Japanese currency sustain gains in the face of a drastic surge in commodity prices? As a net energy importer, Japan is extremely vulnerable to the record-high gasoline prices triggered by the conflict in Iran. While a hawkish BoJ supports the Yen, a deteriorating trade balance (driven by costlier oil) and the risk of an economic slowdown could effectively cap the currency's appreciation, placing the central bank in a precarious position.

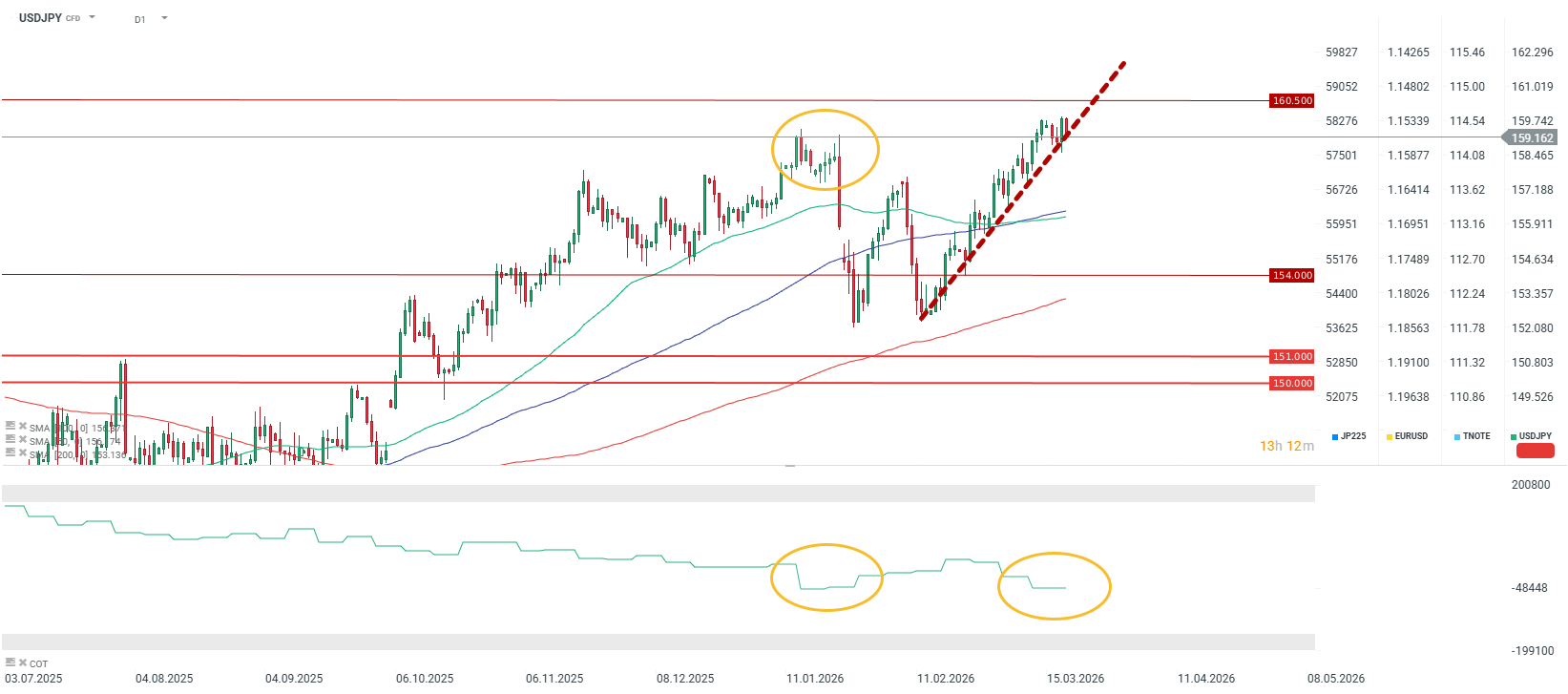

USDJPY is retreating today but remains within its long-term upward trend line. Source: USDJPY

USDJPY is retreating today but remains within its long-term upward trend line. Source: USDJPY

2. SNB: The Franc as a Safe Haven Amid Deflationary Battles

The Swiss National Bank (SNB) kept interest rates unchanged at 0%, in line with market consensus. However, the bank signaled its readiness to intervene in the foreign exchange market to curb excessive appreciation of the Swiss Franc. The currency has gained over 11% against the dollar over the past year, becoming a primary target for capital seeking safety amid the war in Iran and escalating trade tensions.

While the SNB fears that a strong Franc could suppress inflation below its target (deflation risk), the market is beginning to price in a shift in the central bank's stance. Due to inflationary pressures emanating from external markets, investors now assign a high probability to at least one rate hike in Switzerland before year-end. Goldman Sachs forecasts that even in a pessimistic war scenario, Swiss inflation should not exceed 1.9%, providing the SNB with some breathing room, though not eliminating the need to align policy with global trends.

Despite its safe-haven status, the CHF is beginning to lose ground against the USD. However, the pair faces significant resistance at 0.80. Source: xStation5

Despite its safe-haven status, the CHF is beginning to lose ground against the USD. However, the pair faces significant resistance at 0.80. Source: xStation5

3. Riksbank: A Cautious Hold with a Hawkish Bias

Sweden’s Riksbank also opted to leave interest rates unchanged at 1.75%. While the decision matched the consensus, the accompanying communication was pivotal: the war in Iran has significantly clouded the economic outlook. The bank acknowledged that inflation risks are currently asymmetric and tilted to the upside, primarily due to rising oil prices and a weak Swedish Krona.

Expectations for rate hikes in Sweden are rising (with the market pricing in a move by Q3 2026), yet they remain less aggressive than those for the ECB. The Riksbank must strike a balance between combating energy-driven inflation and avoiding the stifling of an economic recovery that has already been revised downward (GDP growth forecasts dropped from 2.9% to 2.5%). However, if Brent crude prices remain elevated, the Riksbank may be forced to accelerate the policy tightening originally slated for late 2027.

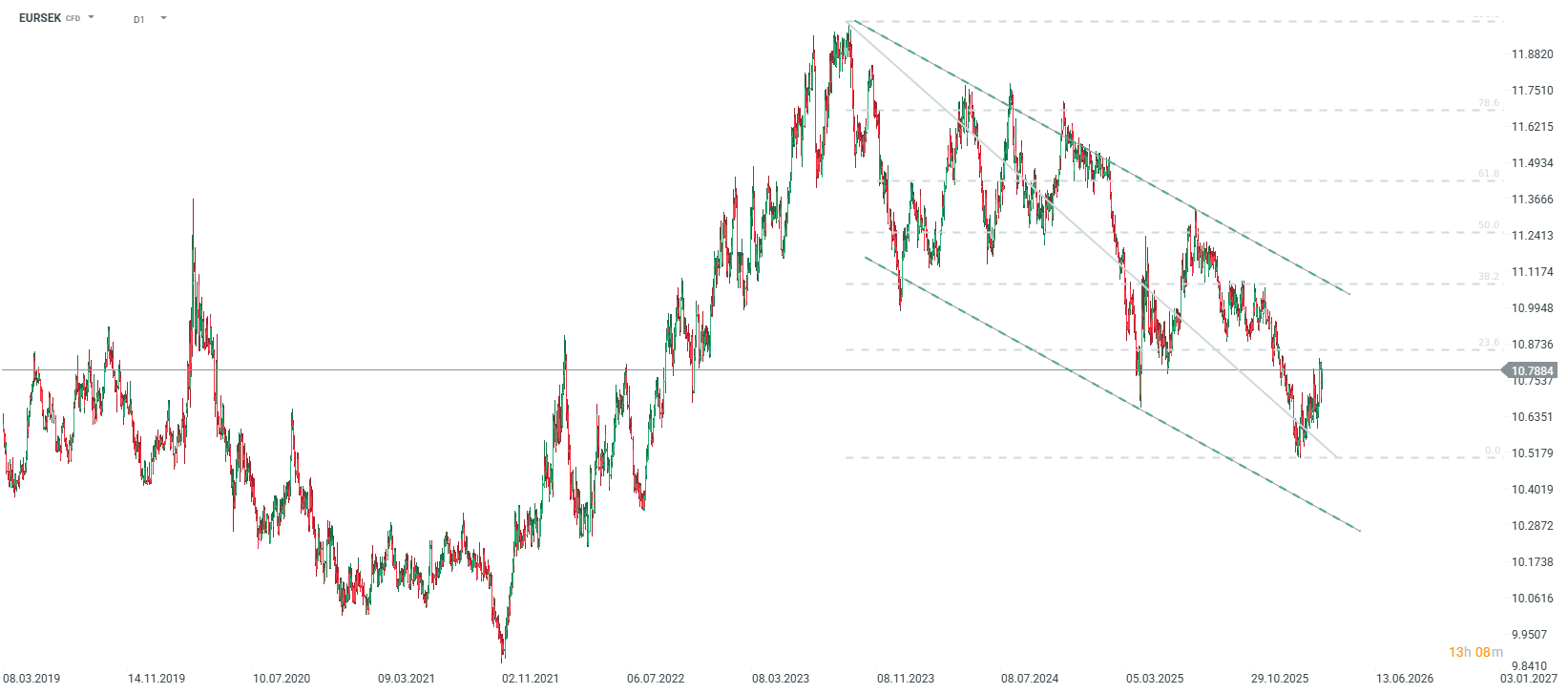

EURSEK remains relatively low, but 2022 marked the beginning of a wave of SEK weakness against the Euro during the high oil and gas price shock. Potentially, the ECB could raise rates faster than the Riksbank, which may shift the bias toward the upside. Source: xStation5

EURSEK remains relatively low, but 2022 marked the beginning of a wave of SEK weakness against the Euro during the high oil and gas price shock. Potentially, the ECB could raise rates faster than the Riksbank, which may shift the bias toward the upside. Source: xStation5

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)