HSCEI futures managed to shake off early Asian session gloom, rallying by a bullish 1.5% despite the relentless conflict in the Middle East and surging energy costs. Market sentiment caught a second wind from the latest macro data which—persistent property sector woes aside—signals a surprisingly robust start to 2026.

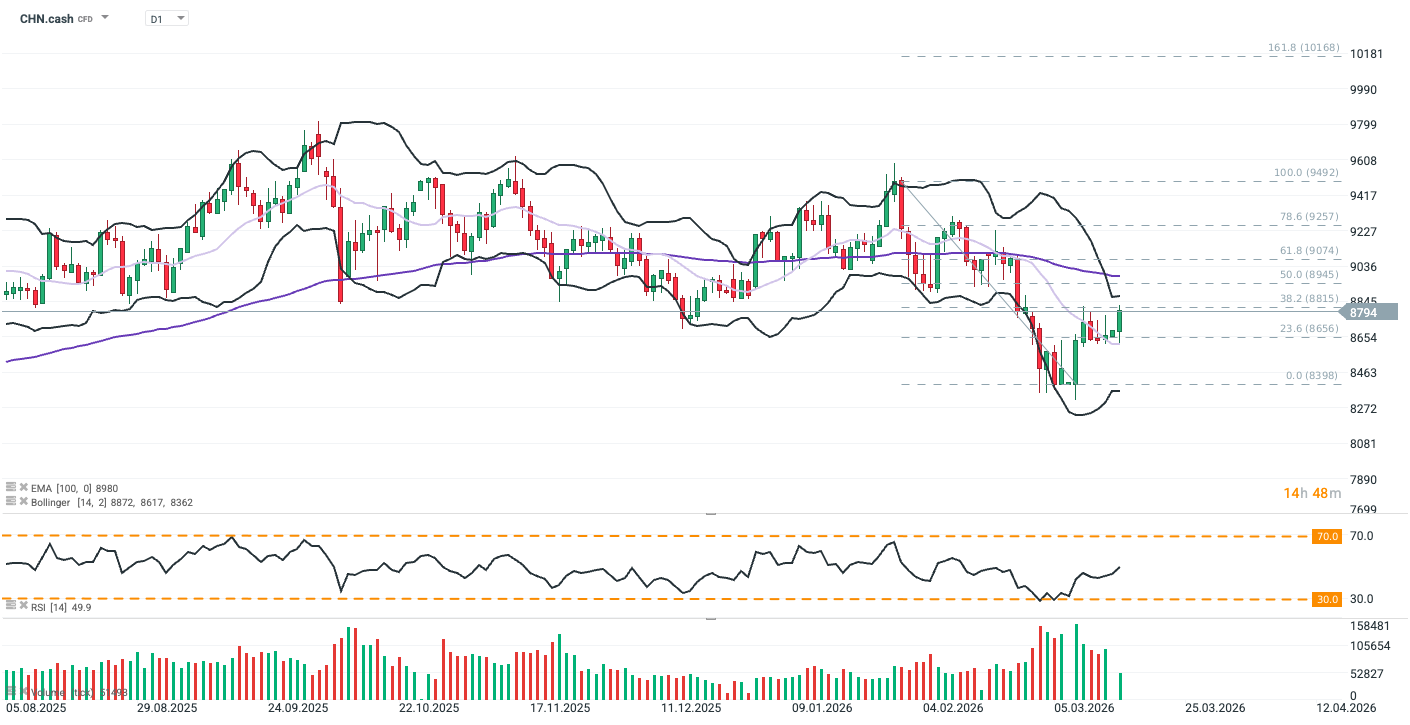

CHN.cash found solid support at the 14-day middle Bollinger Band (light purple) and rebounded towards the 38.2% Fibonacci level. While the bounce is an encouraging sign, a decisive breakout above the upper Bollinger Band (black) remains the critical hurdle for a true trend reversal. Source: xStation5

What is driving today CHN.cash?

-

Industrial Production Beats on "AI-Export" Engine: The 6.3% jump in industrial output (the fastest since September, 5,3% expected) was largely catalyzed by a surprising surge in exports and booming AI-related technology demand. This is a clear tailwind for the tech-heavy components of the HSCEI. However, a deeper look suggests a looming "margin squeeze" for these firms. With the war in Iran driving oil over $100 and disrupting the Strait of Hormuz, rising raw material and fuel costs are expected to eat into the profit margins of manufacturers who are already engaged in “cutthroat competition." The HSCEI may see a "volume up, profit down" scenario in the coming months.

-

Retail Rebound Masks Per-Trip Fragility: A 2.8% rise in retail sales masks significant domestic caution. Growth was skewed by a record-long Lunar New Year that boosted total tourism, yet spending per trip actually fell 0.2% and auto sales plunged 26%. With unemployment ticking up to 5.3%, HSCEI consumer and auto stocks may be riding a seasonal wave rather than a structural recovery.

-

The "Stimulus Delay" Risk: The 1.8% rebound in Fixed-Asset Investment—driven by an 11.4% surge in infrastructure—has effectively stalled hopes for an immediate March rate or RRR cut. This data gives Beijing breathing room to maintain a cautious stance amid Middle East tensions. HSCEI traders pricing in a liquidity injection must now re-calculate for a "higher-for-longer" environment as policymakers prioritize stability over easing.

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market