The political crisis surrounding Keir Starmer has become one of the key market drivers for the pound today. The situation is evolving rapidly and is having a direct impact on government bond yields and the value of the pound, with the markets closely monitoring the Prime Minister’s every word.

Internal party pressure

The scale of Starmer’s problem is best illustrated by a single figure: 42 Labour MPs had already officially called on him to resign by Sunday evening, whilst former Deputy Prime Minister Angela Rayner described the current situation as “Labour’s last chance” to change course. The emergence of potential challengers, such as Wes Streeting and Andy Burnham, means that the market now views the internal dispute within the Labour Party as a real risk, rather than mere political noise.

In his speech on Monday, Starmer focused on several key themes. Firstly, a firm defence of his own position: “I will fight in every internal vote.” Secondly, a political agenda aimed at closer ties with the EU, the nationalisation of British Steel and a new mobility agreement for young people with Europe. The market viewed this speech primarily through the prism of one question: will the Prime Minister stabilise his position sufficiently to halt the sell-off of gilts?

You can watch the UK Prime Minister’s live address here. Source: Sky News, YouTube

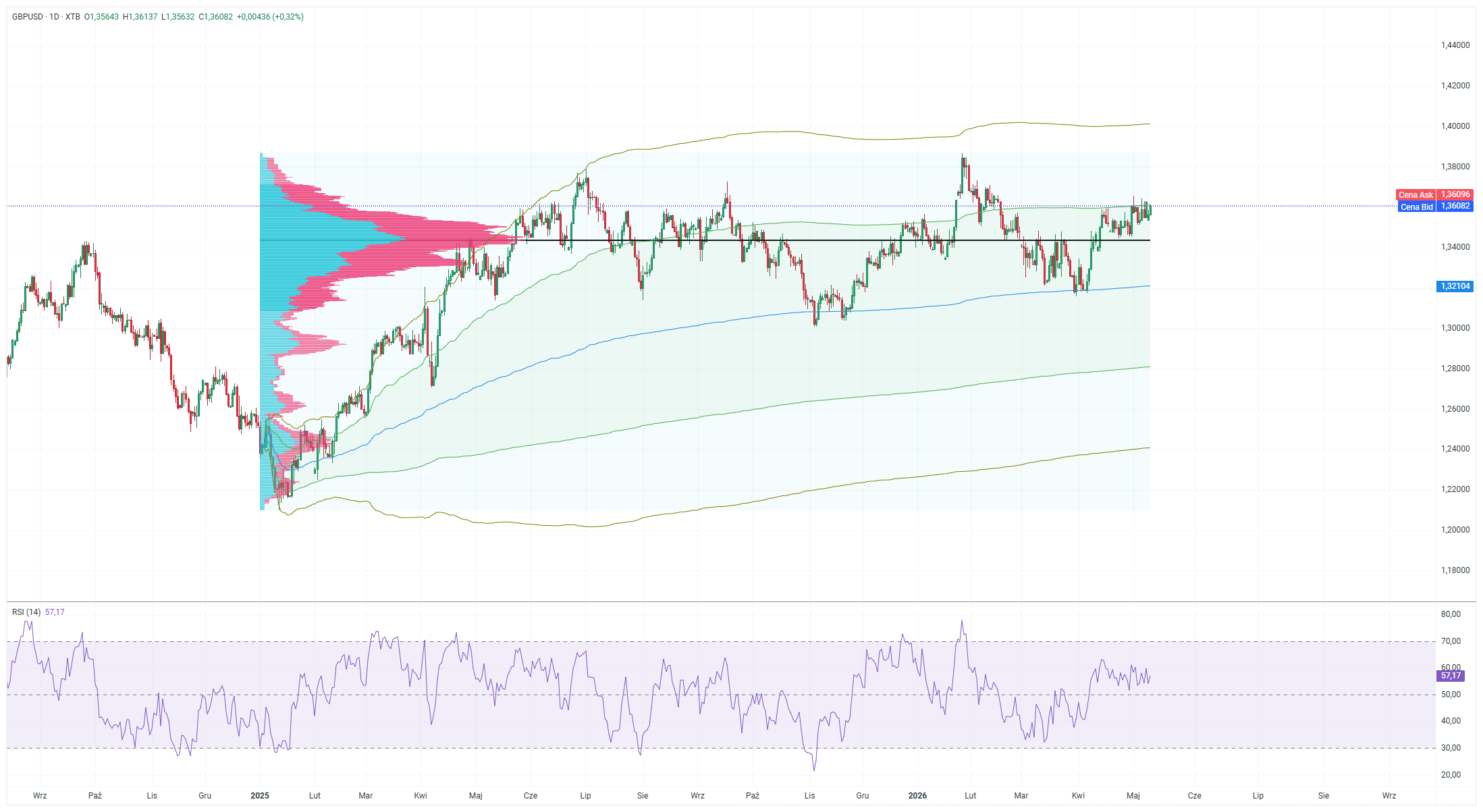

Starmer, gilts in pounds

The yield on 10-year gilts rose on Monday morning to 4.954%, an increase of 3 basis points from the previous close, when it stood at 4.904% immediately after Starmer refused to resign on Friday. Economists surveyed by Bloomberg say that were it not for the political component, yields would be 10–15 basis points lower. This shows just how much the market has already begun to price in the risk of political instability, rather than solely macroeconomic fundamentals.

The UK currently has the highest debt servicing costs of all G7 countries, a consequence of inflation remaining above target and weak economic growth. The situation is further complicated by the economic fallout from the armed conflict in Iran, which has led to higher energy prices and a further weakening of business activity. In such an environment, any political uncertainty acts as a risk multiplier for funds holding gilts.

Implications for the GBP

The pound finds itself in a difficult position, both technically and fundamentally. On the one hand, structural factors such as the Bank of England’s relatively high interest rates compared to the ECB and the marked inflationary divergence from the rest of Europe may continue to support it in the medium term. On the other hand, the political risk premium, which has just begun to be priced into gilt yields, is a factor that directly affects the currency’s valuation: higher bond yields against a backdrop of a weakening government is a scenario that has historically been negative for the pound, as it suggests a lack of a fiscal anchor.

If Starmer survives the coming weeks politically and manages to quell the internal rebellion, the risk premium should gradually decline, and the GBP/USD pair could test higher resistance levels once again. An alternative scenario, namely a genuine battle for party leadership, would, however, mean further rises in gilt yields and pressure on the pound, particularly as global markets are now highly sensitive to any signs of political fiscal instability following the experiences of the Truss era. For sterling traders, therefore, today is a test not so much of Starmer himself as of the resilience of the political risk premium that the market has already priced in.

GBP/USD is trading at 1.3608 on the daily chart, within an uptrend that has been in place since the low around 1.22 at the turn of 2024/2025, and the price remains above the anchored VWAP from early 2025, which runs in the 1.31–1.32 region. The volume profile indicates a Point of Control in the 1.3450–1.3480 zone, where a black horizontal line marks a key support level that has been tested repeatedly on both sides. The RSI(14) at 57.17 suggests neutral-bullish momentum with no signs of overbought conditions, which technically leaves room for further gains towards the 1.3800–1.3850 resistance zone, where the price reversed at the 2025 peak. Today’s speech by Starmer and his political survival are factors that will directly determine the short-term direction: government stability paves the way upwards, whilst an escalation of the crisis and a rise in gilt yields would push the pair back towards the POC zone at 1.3450, and, in the event of a deeper sell-off, even towards the VWAP. Technically, the bulls have the upper hand as long as the price remains above 1.34, and the bears will only regain the initiative after a break below this zone with volume.

Source: xStation

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!