- Supply fundamentals remain heavily concentrated in West Africa, which accounts for a significant share of global cocoa production. As a result, any deterioration in weather conditions across the region quickly translates into a higher risk premium embedded in cocoa futures prices.

- At the same time, the price correction observed over recent months had started to improve demand signals, while the supply-sensitive nature of the market reacted rapidly to renewed weather concerns and the need for funds to reduce short exposure. The current price action highlights how vulnerable cocoa remains to sharp swings given the tight supply backdrop. As long as production risks in West Africa remain elevated, volatility is likely to persist, favoring bullish momentum in the short term.

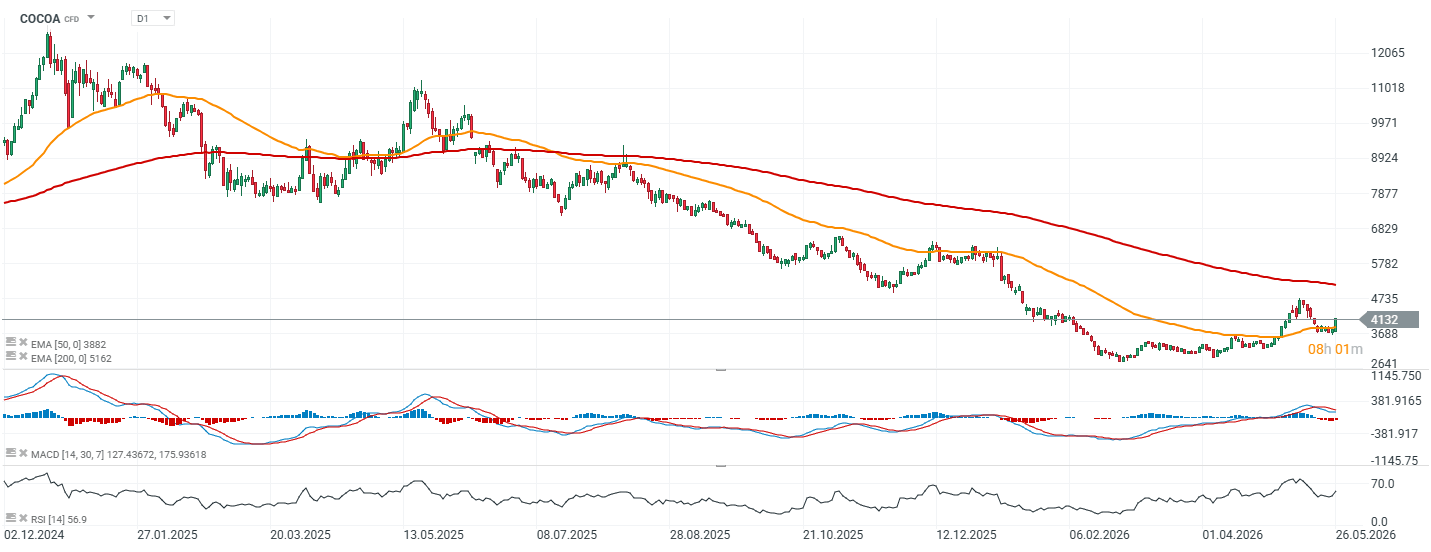

COCOA chart (D1 interval)

Source: xStation5

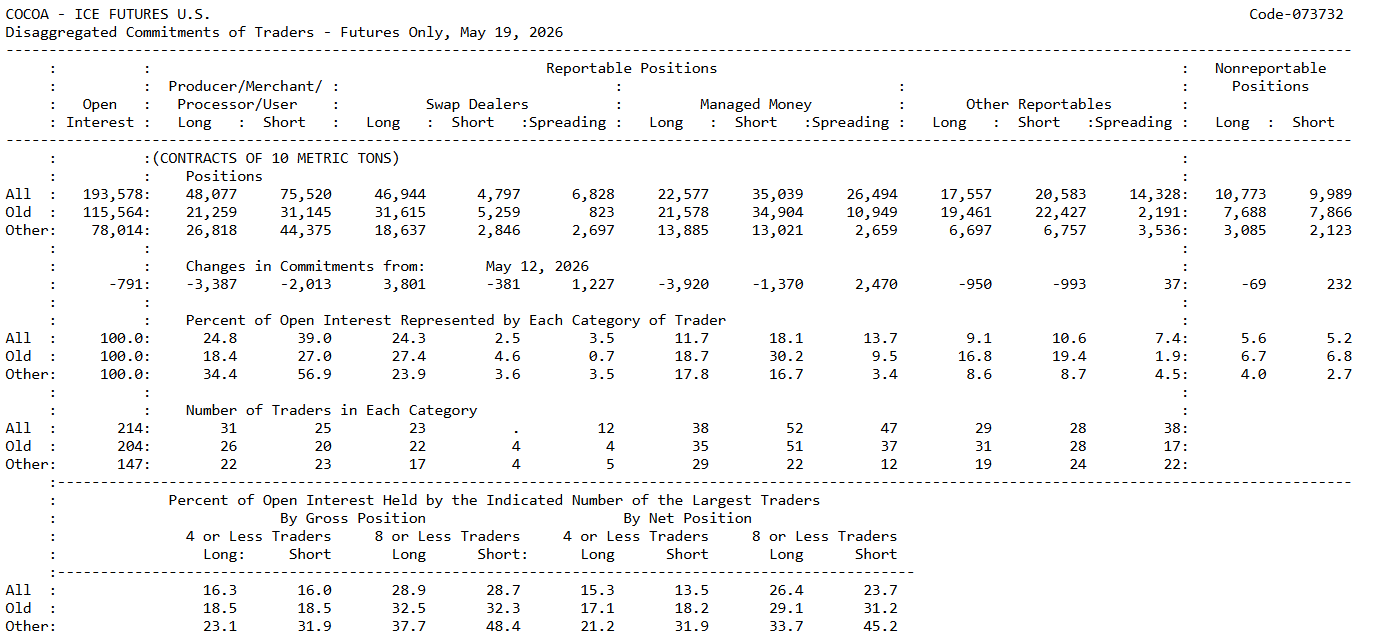

CFTC "Commitment of Traders" Analysis

General CoT picture

The latest CoT report for cocoa shows a positioning structure that could support a short squeeze scenario, although it does not yet resemble a full capitulation of bearish positioning. Rather, this appears to be an early-to-mid-stage process in which the market is beginning to force short covering, while funds still remain meaningfully positioned on the short side.

Most importantly, Managed Money remains net short. Funds currently hold 22,577 long positions against 35,039 shorts, leaving the category net short by roughly 12.5k contracts. This suggests that despite the recent rebound in cocoa prices, a large portion of speculative capital is still positioned for further downside.

Commercials are not aggressively increasing hedges

Commercials 0 including producers, merchants, processors, and users remain net short, with 48,077 longs versus 75,520 shorts, or roughly 27.4k contracts net short. This is not unusual in cocoa, as physical market participants typically hedge future production through short futures exposure.

What is more interesting, however, is that commercials are not aggressively adding short hedges into the rally. On the contrary, their gross short exposure declined by roughly 2,000 contracts week-over-week. This suggests that the physical side of the market does not view current prices as an obvious opportunity to significantly increase forward hedging activity.

Managed Money as fuel for a squeeze

The strongest short squeeze potential comes from speculative positioning. Managed Money remains clearly net short while cocoa prices have started to rebound aggressively. This creates a classic setup in which every additional upside impulse can force further short covering.

It is also notable that funds reduced long exposure aggressively over the past week, while only partially reducing short exposure. This implies that positioning remains defensively skewed relative to current price action. If the market continues to move higher, this group may be forced into faster buybacks of short contracts.

Open interest confirms the nature of the move

Open interest declined by 791 contracts while cocoa prices moved higher. Such a combination typically suggests that the rally is not yet being driven primarily by fresh long positioning, but rather by the closing of existing shorts.

This distinction is important. Rising prices combined with rising open interest would point toward fresh bullish capital entering the market and the formation of a new structural uptrend. In this case, however, the picture still looks more consistent with a short-covering rally.

Is this already a short squeeze?

Yes, but not yet in its most aggressive phase. The overall market structure has squeeze-like characteristics: funds remain net short, prices are rebounding, open interest is declining, and the market has a strong weather catalyst tied to El Niño risks and West African production concerns.

At the same time, the scale of Managed Money short exposure does not yet appear historically extreme. There are no clear signs of panic liquidation among shorts so far. Instead, the market currently looks like it has sufficient fuel for a more extended squeeze should another negative supply-side catalyst emerge.

Trading conclusion

The current CoT positioning supports the thesis that the recent rebound in cocoa prices contains a meaningful short-covering component. Commercials are not aggressively offsetting the rally with additional hedging activity, while Managed Money still holds a sufficiently large net short position for further upside to force additional buybacks. If cocoa prices continue to rise while open interest keeps falling and Managed Money rapidly reduces short exposure in upcoming CoT reports, this could confirm that the market is transitioning into a more mature phase of a short squeeze.

Source: CFTC

Eryk Szmyd XTB Financial Markets Analyst

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)