-

Strong labour market data is supporting the dollar.

-

The market is fully pricing in an ECB rate hike this week.

-

The situation in the Middle East remains uncertain

-

USDJPY breaks through the 160 barrier, increasing the likelihood of BoJ intervention.

-

The Colombian peso gains ground following the election, whilst the won falls sharply amid a sell-off on the KOSPI.

-

Strong labour market data is supporting the dollar.

-

The market is fully pricing in an ECB rate hike this week.

-

The situation in the Middle East remains uncertain

-

USDJPY breaks through the 160 barrier, increasing the likelihood of BoJ intervention.

-

The Colombian peso gains ground following the election, whilst the won falls sharply amid a sell-off on the KOSPI.

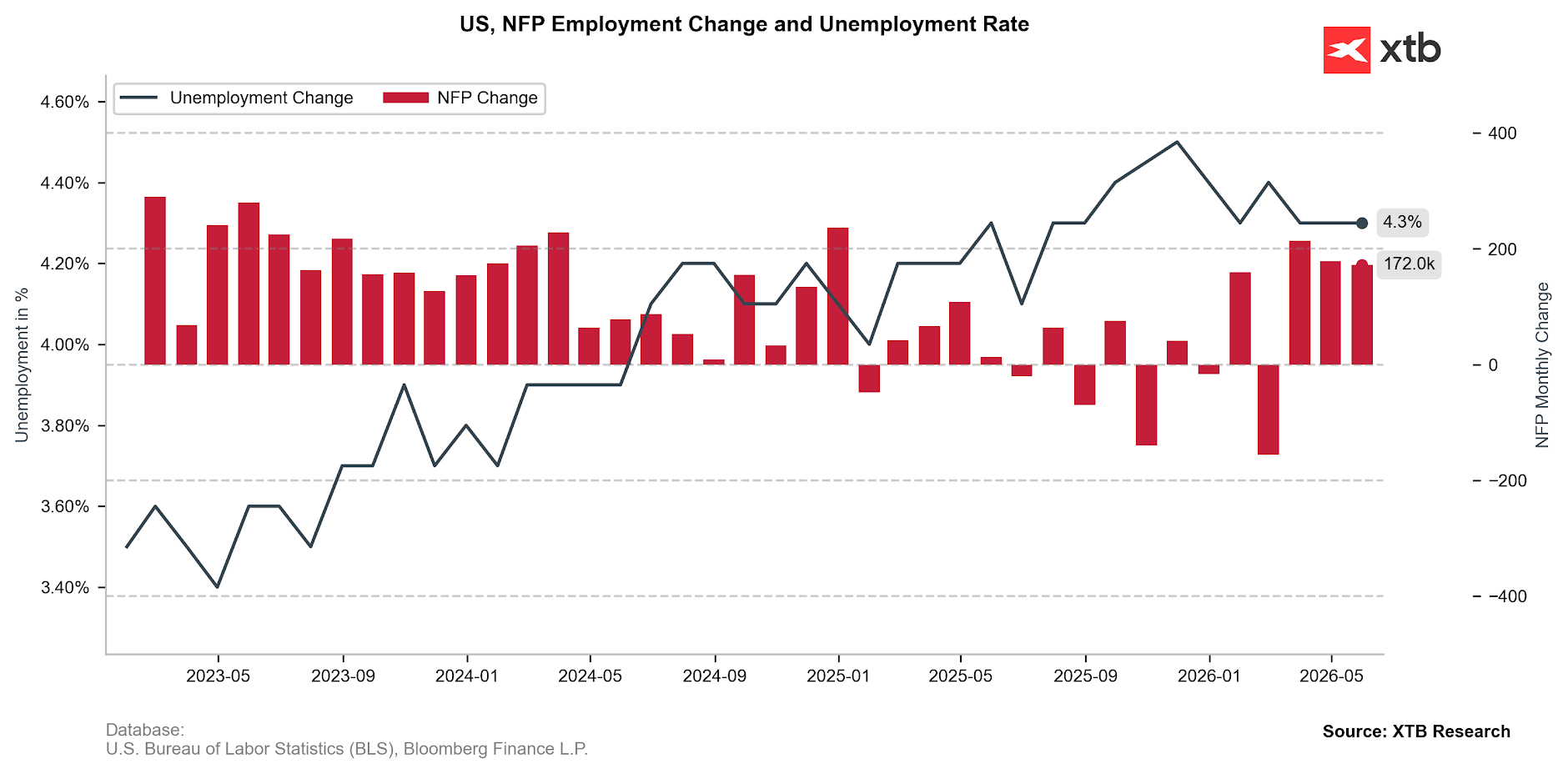

Friday's NFP report did not disappoint. The data exceeded even the most optimistic forecasts, signaling that the situation in the US labor market is indeed stabilizing. This plays into the hands of the already strong hawkish wing within the FOMC. Markets are now fully pricing in a US interest rate hike before the end of the year. This repricing was the main driver behind the dollar's strengthening over the past week.

Little has been resolved regarding the situation in the Middle East. Markets continue to react strongly to media headlines, but they lack a clear direction. For the record: over the weekend, we witnessed mutual attacks between Israel and Iran, while today President Trump announced a temporary ceasefire between the parties, which slightly improved market sentiment.

Any news from Tehran could still leave a significant mark on exchange rates. President Trump would likely want to announce an agreement between the parties as soon as possible, especially since the World Cup – co-hosted by the US and watched by billions of viewers worldwide – kicks off on Thursday. However, there are few indications that a memorandum can be signed in the coming days.

On Thursday, attention will shift not only to the Estadio Azteca in Mexico City, but also towards Frankfurt am Main, where President Lagarde will take the podium following the ECB's interest rate decision. Everything indicates that the Governing Council will deliver a rate hike, which is fully priced in by the markets. Attention will focus on whether Lagarde’s rhetoric leans more towards growth data signaling stagnation or concerns regarding inflation.

Wednesday’s release of US inflation data could prove equally important. The core reading, being less volatile, will be of particular interest, as it should help determine the pass-through level of higher energy commodity prices onto other sectors of the economy.

US Dollar (USD)

Recent incoming data suggests that Kevin Warsh's first meeting as FOMC Chairman (June 17) will not be among the easiest. It is currently hard to believe that he will be able to maintain his conviction regarding the necessity of monetary easing. It is even harder to believe that he will convince other policymakers.

The number of job openings in the US labor market rose by 172k. This result is not only better than the consensus (86k) but significantly exceeds even the most optimistic forecasts (125k). The report fits perfectly into the broader picture painted by recent labor market releases. Weekly unemployment claims remained near multi-year lows, while ADP and JOLTS data surprised to the upside – the latter particularly strongly, though it should be noted that they are significantly lagged compared to the rest.

Figure 1: Non-farm payrolls (NFP) change and the unemployment rate in the US (2023 - 2026)

Source: XTB Research, 08.06.2026

Source: XTB Research, 08.06.2026

It is also consistent with the narrative from the latest FOMC minutes – Fed analysts showed that after a period of cooling, labor market conditions have "stabilized." Even then, for some policymakers, this served as an argument that the economy is not on the brink of a sudden slowdown and does not need the support of cheaper money.

Euro (EUR)

Before attention shifts across the ocean, however, the ECB meeting awaits us. A lack of an interest rate hike could cause a minor earthquake for the markets, as it is currently fully priced in. The Governing Council should not surprise, shifting the focus to the press conference. President Lagarde has not accustomed us to overly exciting speeches, keeping forward guidance – i.e., hints regarding future moves – to a minimum.

Most likely, this time will be no different. However, if the rhetoric emphasizes the weakness of the European economy to a greater extent, and inflation concerns to a lesser extent, the decline of the EURUSD pair could continue. Some light on the sentiment within the Council may also be shed by later reports from the already infamous "sources close to the ECB."

G10 Currencies

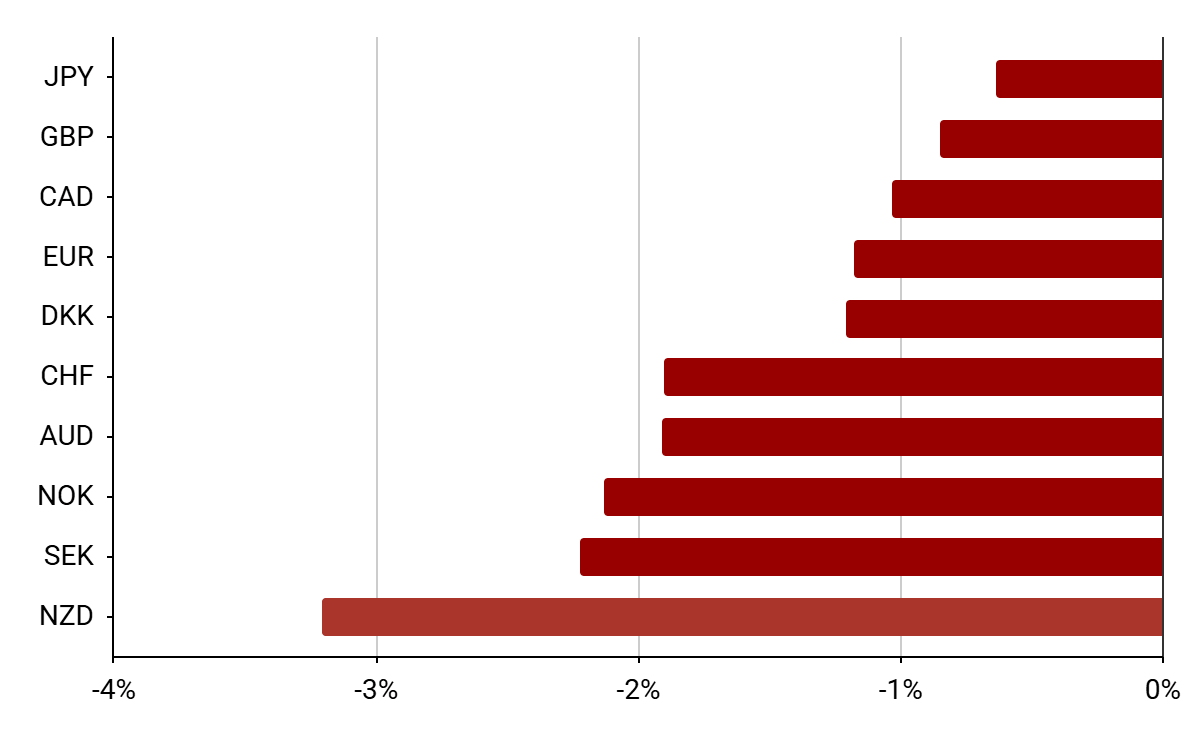

Figure 2: G10 currency performance [vs. USD] (29.05 - 05.06)

Source: Bloomberg, 08.06.2026

Source: Bloomberg, 08.06.2026

All other G10 currencies weakened against the dollar last week. A relatively small move was observed on the USD/JPY pair, but it was enough to push it above the 160 level, considered by many as a psychological barrier of sorts. This increases the likelihood of another Bank of Japan intervention, although, as recent weeks have taught us, there is little indication that it could provide the yen with any lasting relief. Such relief can likely only be brought by a stronger pivot in monetary policy.

At the other end of the spectrum, we find the New Zealand dollar, which has given back virtually all the gains made after the last RBNZ meeting. It continues to be weighed down by high geopolitical uncertainty, which also pressures other high-beta currencies – the Swedish krona and the Norwegian krone.

Aside from Thursday's ECB meeting, we will closely watch Wednesday's inflation data from China and Norway, the BoC decision (also Wednesday), as well as the week-ending GDP and industrial production readings from the UK.

EM Currencies

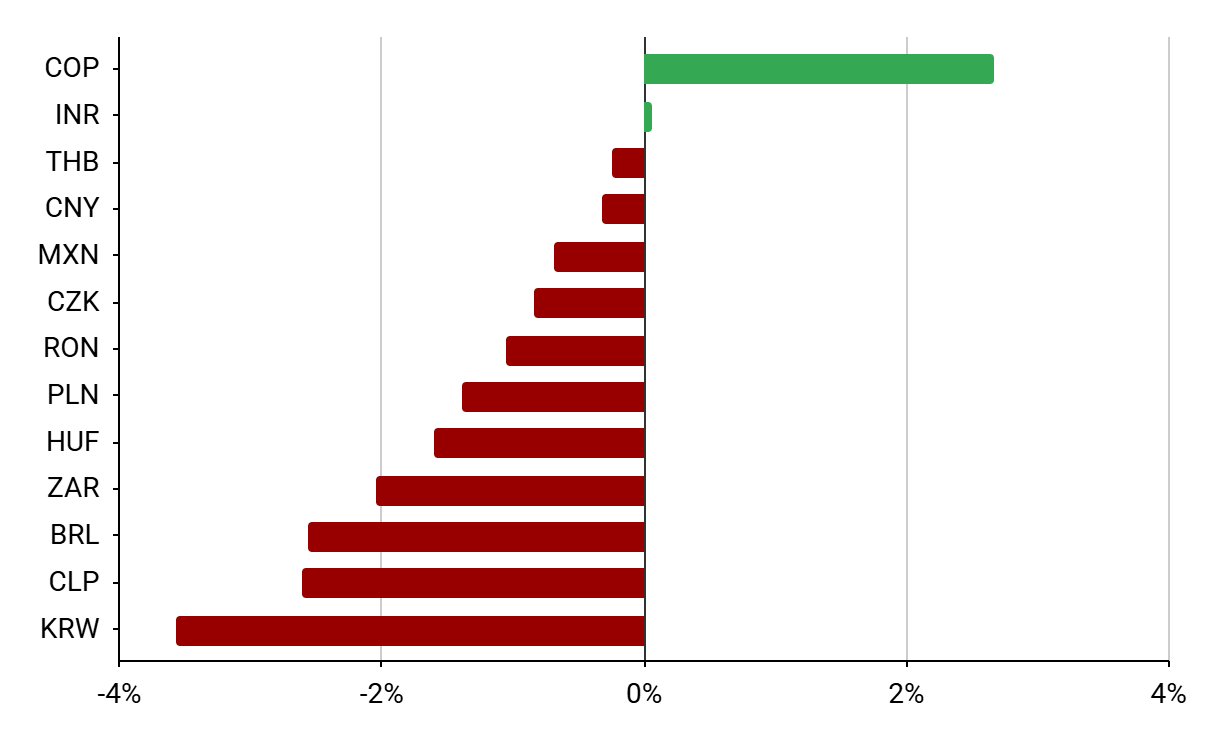

Figure 3: Selected EM currency performance [vs. USD] (29.05 - 05.06)

Source: Bloomberg, 08.06.2026

Source: Bloomberg, 08.06.2026

The Colombian peso finishes the week at the top. As we wrote last week, markets reacted extremely positively to the surprisingly strong performance of the right-wing Abelardo de la Espriella in the first round of the presidential election. He is seen by investors as the undisputed favorite to win the second round scheduled for June 21.

On the other side, unsurprisingly, were the currencies of the countries most exposed to a prolonged closure of the Strait of Hormuz – the Brazilian real, the South African rand, and the Hungarian forint. Due to the drop in copper prices, the Chilean peso also underperformed.

The biggest loser turned out to be the South Korean won, which suffers not only from deteriorating investor sentiment due to the lack of significant progress in negotiations between Iran and the US, but also from profit-taking on Korean equities by foreign investors. Both the scale of the KOSPI's rise in 2026, which exceeds 70% even when accounting for today's more than 8% sell-off, and the recent emergence of leveraged single-stock contracts (Samsung and SK Hynix, which account for 50% of the index), expose the Korean stock market to significant volatility. This may therefore also accompany the won.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

⬆️Oil back above $88

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse