- The end of today's session brought a lot of turmoil to the markets after reports of possible changes to Japan's yield control program.

- In the wake of these announcements, the USDJPY pair fell sharply below the psychological barrier of 140.00. Moreover, the announcement almost significantly negated the day's rallies on US Wall Street.

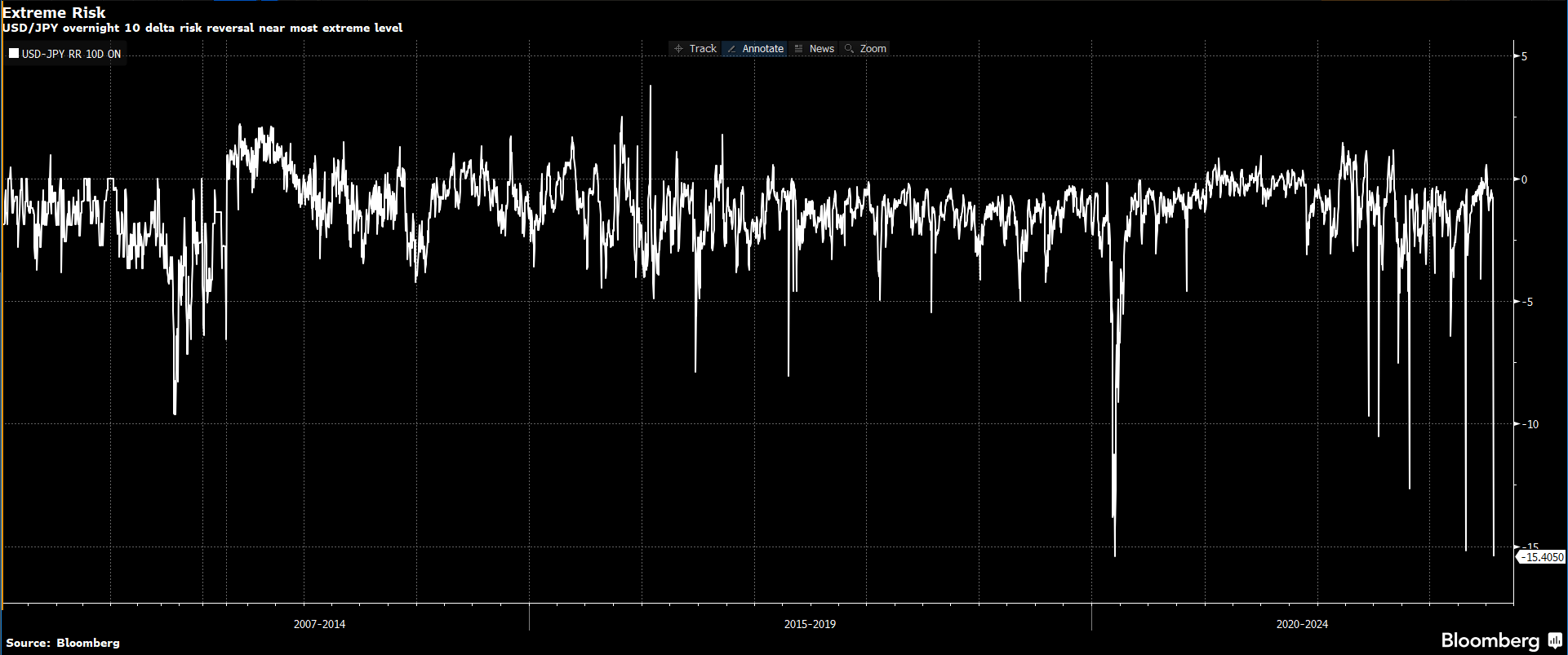

- Quite a lot of confusion is also observed in the options market, where positioning to hedge against a sharp decline in the USDJPY pair reached almost the highest values in 15 years.

- Tomorrow's BoJ meeting is expected to discuss programmatically allowing yields to rise above the 0.50% limit by a certain degree.

- At the moment, the best performing currency in the FX market is the Japanese yen, and the worst performing is the British pound.

- Indexes in Europe were euphoric today, with the DAX up 1.7% with the CAC40 rallying more than 2%.

- After the session, luxury goods giant Kering delivered a weaker-than-forecast Q2 report. After yesterday's surprise results from LVMH, investors are beginning to see opportunities for longer-term weakness in the fashion industry

- The ECB raised rates by 25 bps to 3,75% as expected, but during the press conference, President Christine Lagarde, despite her hawkish narrative, did not rule out a pause in the cycle and indicated that the bank would respond to data. This supported market sentiments and EURUSD weakened;

- The money market now assumes (after Lagarde's initial comments) that the ECB will raise rates by 25 bps at its September meeting with a probability of just under 40%.

- The strength of the US dollar resulting from Lagarde's dovish comments and strong macro data lifted gold prices below the psychological barrier of $1,950

- The macro data package from the US turned out to be much better than expected, which ultimately supported sentiment on the indices. S&P500 gains 0.2% at 0.8% - some of the gains were erased by reports from the Bank of Japan

- U.S. unemployment claims indicated 221,000 with 235,000 forecast and 228,000 previously. Continuing claims unexpectedly fell from 1.75 million to 1.69 million

- Durable Goods Orders surprised sharply upward, rising 4.7% m/m with an expected increase of 0.6% and 1.8% previously. Orders excluding transportation equipment also beat expectations by 0.5% m/m

- Annualized GDP reading indicated 2.4% vs. 1.7% forecast and 2% previously with core PCE inflation 0.2% lower than forecast - reading indicated 3.8% vs. 4.9% k/k previously

- US natural gas inventories data came in above expectations. Current: +16 bcf. Expected change: +14 bcf. Previous: +41 bcf

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

Who Will Surprise With Earnings Next Week? (07.08.2026)

The dollar sinks after labor market data💲📉