- European markets traded with mixed sentiment today. The Euro Stoxx 50 posted modest gains, while Banca Monte dei Paschi di Siena stood out in the financial sector, with its shares climbing nearly 10%. Germany’s DAX fell more than 0.5%.

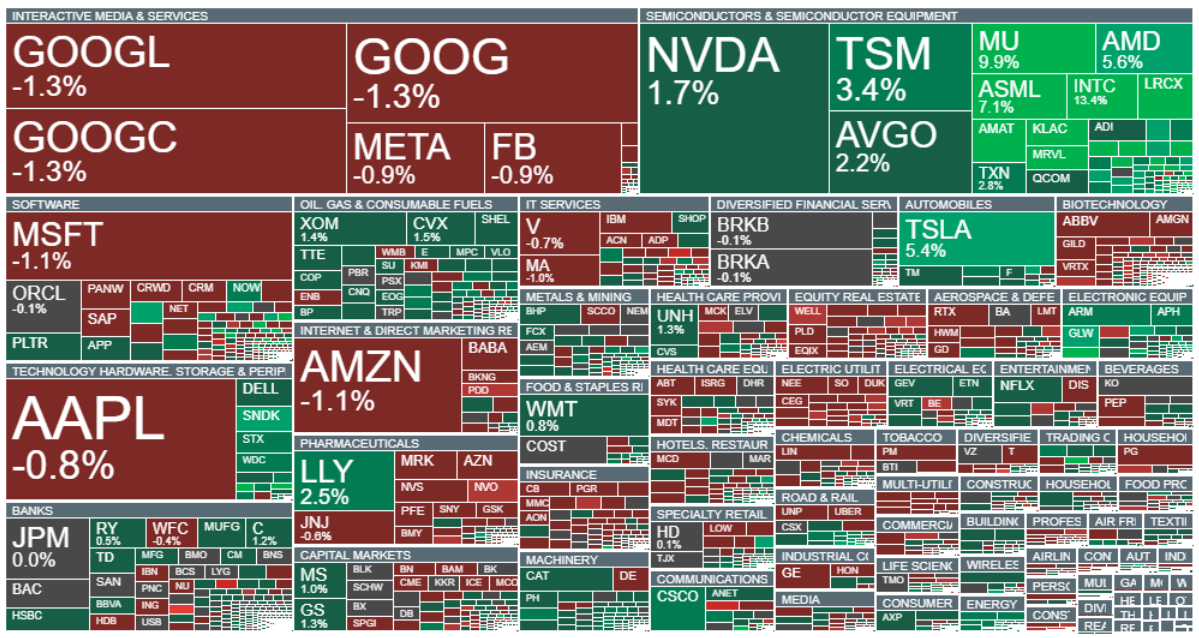

- U.S. equities are moving higher, although it is somewhat concerning that the gains are largely concentrated in the technology names that suffered the steepest declines on Friday, particularly semiconductor and AI-related stocks. Other sectors are lagging behind. The Dow Jones Industrial Average is slightly lower, while the Nasdaq 100 is up around 1.3%. The deteriorating market breadth, where gains are increasingly concentrated in a narrow group of stocks, does not appear healthy for the market over the longer term.

- The decline in oil prices has allowed investors to breathe a sigh of relief despite the ongoing escalation between Israel and Iran. Israeli Prime Minister Benjamin Netanyahu reportedly instructed the country not to respond to Tehran’s latest strikes, while President Trump stated that a deal with Iran is currently being finalized. As a result, oil prices retreated from around $98 per barrel at the open to below $94 per barrel.

- At the same time, forecasts cited by Bloomberg pointing to a significant decline in global inventories suggest the risk of a major supply crisis by October 2026 if no diplomatic solution is reached and unrestricted traffic through the Strait of Hormuz is not restored by then.

-

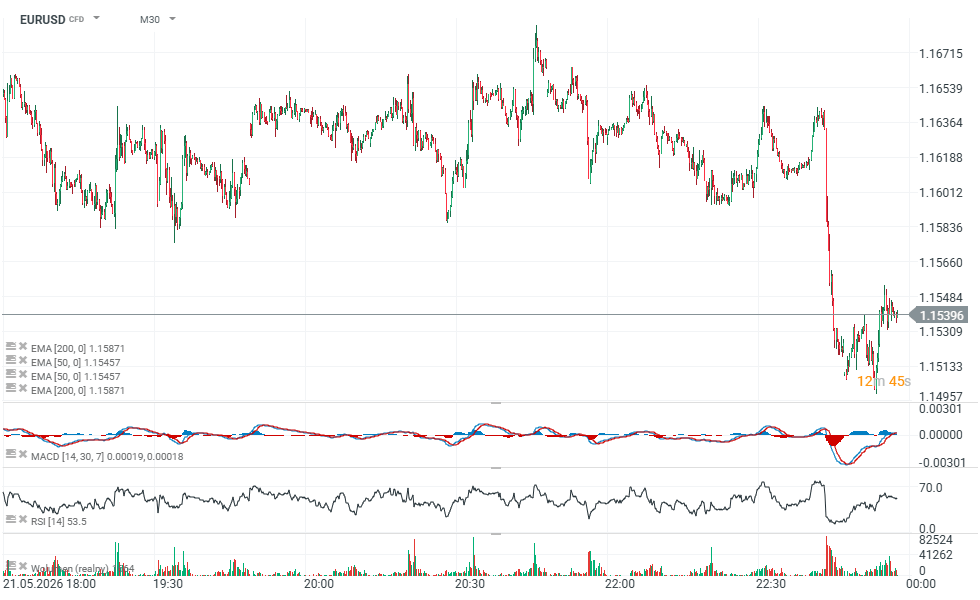

Precious metals are generally underperforming, although gold is attempting to recover part of its losses from the open, trading near $4,320 per ounce. Platinum and palladium are both down around 2%. Bitcoin has regained some ground and is trading close to $63,000, after falling below $60,000 last week. Today's announcement by Strategy regarding another Bitcoin purchase has provided some support for the cryptocurrency. EUR/USD is posting a modest rebound following last week's sharp sell-off, while U.S. Treasury yields are edging slightly higher. - Pentagon plans to designate Alibaba, Baidu and BYD as Chinese military-linked companies, according to a federal register notice. Shares of the Chinese ADR-s are falling after it - Alibaba shares reversed almost all gains it gained since the beginnig of April.

- The upcoming SpaceX IPO on Nasdaq is attracting exceptionally strong investor interest and is reportedly significantly oversubscribed. The company is expected to close its order book after Wednesday's market session and is scheduled to make its Wall Street debut on Friday, June 12.

- Goldman Sachs and JPMorgan are reportedly exploring futures contracts linked to GPU rental prices, according to The Information, highlighting growing institutional interest in AI infrastructure markets. ($GS, $JPM)

-

Semiconductor and memory-chip stocks like Micron and Sandisk are leading today’s U.S. trading session. Meanwhile, declines are concentrated in real estate, biotechnology, defense, and healthcare stocks. Within the healthcare sector, Novo Nordisk is moving lower, while Eli Lilly is posting gains.

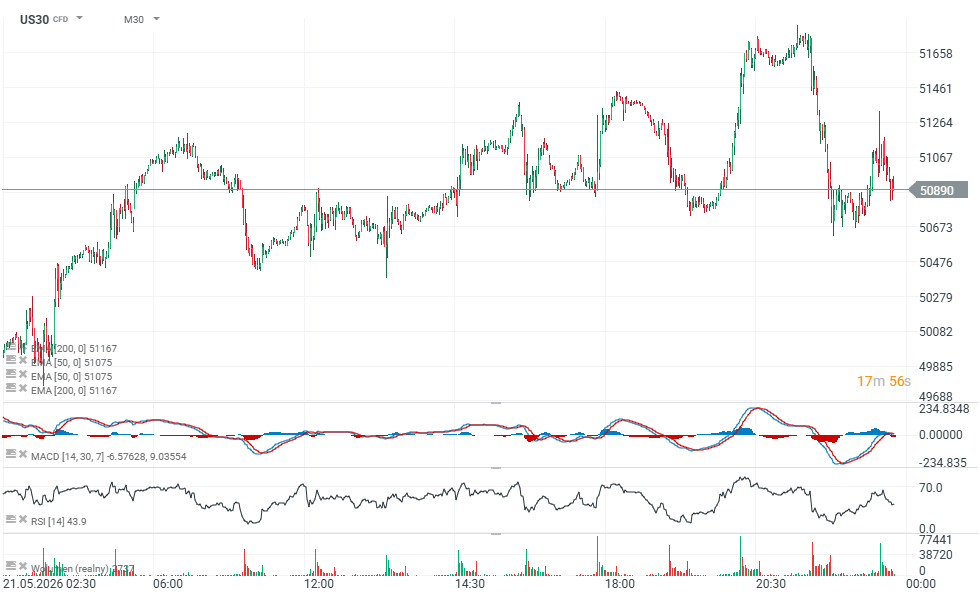

Charts: US30, EURUSD

Source: xStation5

Source: xStation5

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse