- European indices closed a moderately positive session; the DAX and the UK’s FTSE edged slightly higher, while France’s CAC 40 gained 0.7%. In the United States, Nvidia’s record quarterly earnings report was not enough to fuel broader market optimism; the tech-heavy Nasdaq 100 is down 1.4%, while the S&P 500 is retreating 0.7%. The US dollar is strengthening following solid labor market data, with EUR/USD losing more than 0.3%.

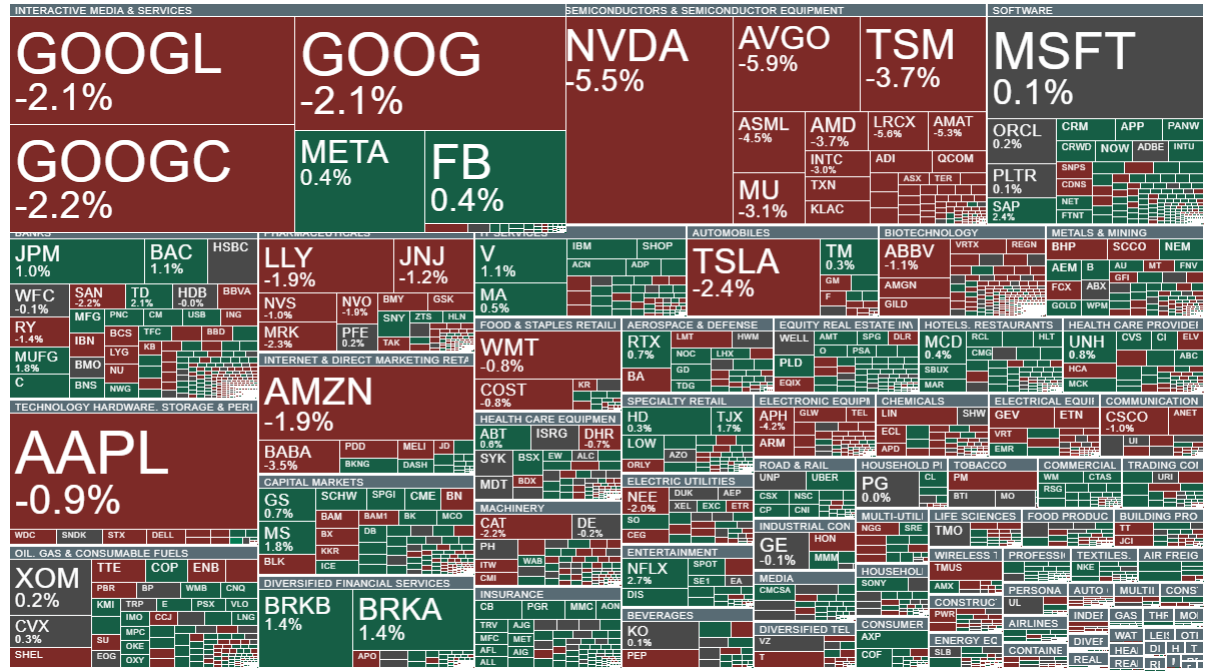

- In the semiconductor sector, we are seeing broad-based declines; Nvidia shares are down more than 5.5%, while Broadcom is losing nearly 6%. Big Tech stocks are also trading lower, with the exception of Meta Platforms. In the software and IT services space, initial gains have been pared back. Shares of aerospace and defense company Heico are falling more than 10%, as investors reacted to rising debt levels and weaker profitability in the Electronic Technologies Group segment - despite 14% year-over-year revenue growth and an earnings-per-share beat.

- Seasonally adjusted initial jobless claims totaled 212,000 in the week ending February 21. This marks an increase of 4,000 from the upwardly revised previous reading, but remains below the Dow Jones consensus estimate of 215,000. The four-week moving average rose by just 750 to 220,250. Continuing claims (reported with a one-week lag) declined by 31,000 to 1.833 million. The data suggest a likely extended pause in the Fed’s policy easing cycle.

- Oil futures are rising amid uncertainty over the outcome of US-Iran negotiations. Iranian state media reported that authorities will not agree to the removal of enriched uranium from Iranian territory, while the United States continues to press “maximalist” demands on Tehran, calling for the suspension of operations in key sites such as Natanz and Isfahan. Earlier, Oman described the talks as constructive, although negotiations are set to resume.

- According to the EIA, US natural gas inventories fell by 52 billion cubic feet, compared with a 50 bcf decline previously and a 144 bcf drop in the prior reading. US Henry Hub natural gas (NATGAS) futures are down nearly 2.4%.

- Semafor, citing sources familiar with the matter, reported that Stripe is not currently considering a takeover bid for PayPal (PYPL.US). The news triggered a sharp sell-off in the payments giant’s shares, which had recently used speculation about a potential acquisition as a “springboard” for a rebound following heavy losses - fueling investor hopes of a buyout at a potentially significant premium to the current market valuation.

- Bitcoin is down nearly 2% to around $67,000, Ethereum is falling 2.5%, and Ripple is retreating by almost 5%. Strategy shares are edging slightly higher, holding near $130 per share. Meanwhile, shares of Circle Internet Group, associated with the USDC stablecoin, are extending yesterday’s gains and moving above $86, posting an increase of nearly 3.5% despite weaker broader market sentiment.

-

(Summary in progress)

Source: xStation5

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR