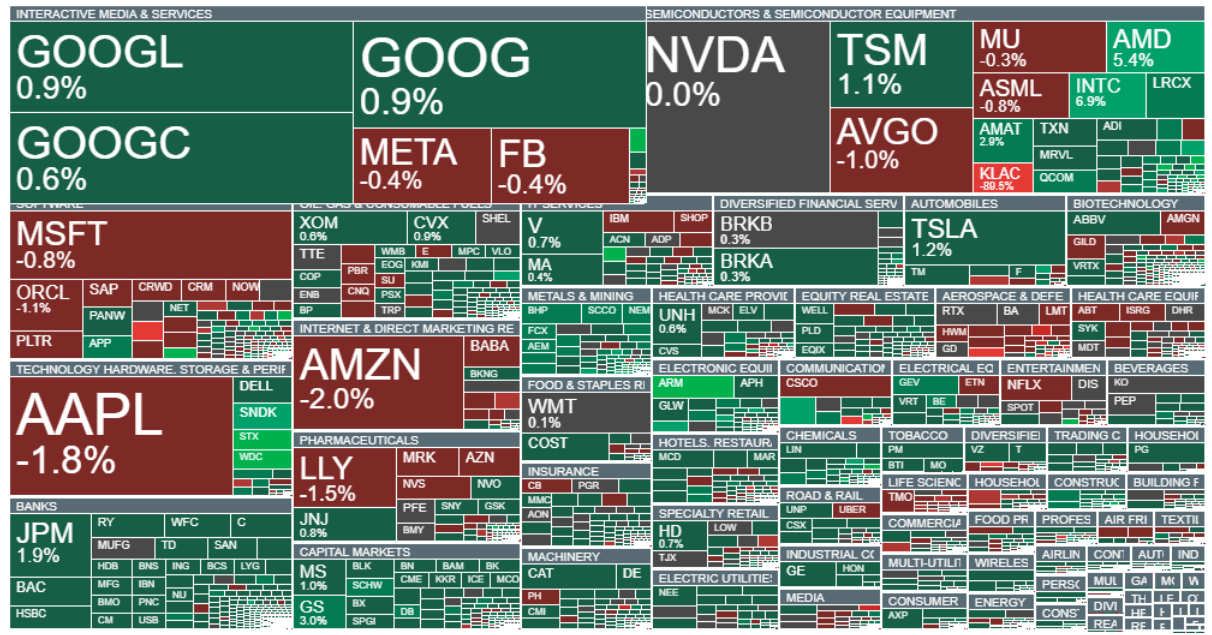

- Stock indices are advancing on the final trading session of the week, supported by falling oil prices, gains in semiconductor stocks, a successful SpaceX market debut (the company is up more than 28% since its listing), and encouraging U.S. macroeconomic data. The latest figures showed stronger-than-expected consumer sentiment and a surprising decline in inflation expectations. The Dow Jones Industrial Average is up nearly 0.7% today, while the Nasdaq 100 is gaining 0.2%, with semiconductor stocks among the best performers.

- European markets also traded firmly in positive territory. The Euro Stoxx 50 rose more than 2.1%, while Germany’s DAX gained 1.7%. Shares of French luxury goods companies such as Hermès and Kering, as well as some of Europe’s largest banks, advanced after the latest inflation reading pointed to higher price growth. Meanwhile, in the United States, shares of Intel, AMD, SanDisk, and Arm are posting strong gains, underscoring the continued dominance of the AI infrastructure theme.

- The preliminary University of Michigan Consumer Sentiment Index came in at 48.9 points, beating expectations of 46.0 and improving from the previous reading of 44.8. Consumer sentiment increased by roughly 4 index points this month, representing a 9% rise. The improvement was partly driven by lower gasoline prices at the beginning of the month. The gains in sentiment were broad-based, spanning different age groups, education levels, and political affiliations. Lower-income consumers recorded particularly strong improvements, as fuel costs account for a larger share of their household budgets.

- Assessments of personal finances, financial expectations, and business conditions all improved during the month. Despite the rebound, sentiment remains weak, standing 13% below January 2026 levels and 19% lower than a year ago. Consumers continue to focus on everyday living costs and remain concerned about inflationary pressures. One-year inflation expectations declined from 4.8% in May to 4.6%, although they remain elevated. Long-term inflation expectations fell from 3.9% to 3.4%, but still remain above the 2.8%–3.2% range observed throughout 2024.

- Oil is trading near USD 87 per barrel and, after a sharp sell-off, has approached its 200-day moving average on the daily chart, highlighting a key technical level. The decline accelerated following reports that Donald Trump had called off a planned strike on Iran and news that negotiations over a potential agreement with Iran had entered their final stages, a development that was tentatively confirmed by Iranian officials. However, the situation remains highly fluid.

- Precious metals are rebounding, with gold rising 0.5% to USD 4,230 and silver gaining more than 1%. Bitcoin is trading around USD 63,500 after giving back part of its earlier gains. In the commodities space, cocoa stands out with gains of more than 2%, while U.S. Henry Hub natural gas (NATGAS) futures are up nearly 1%.

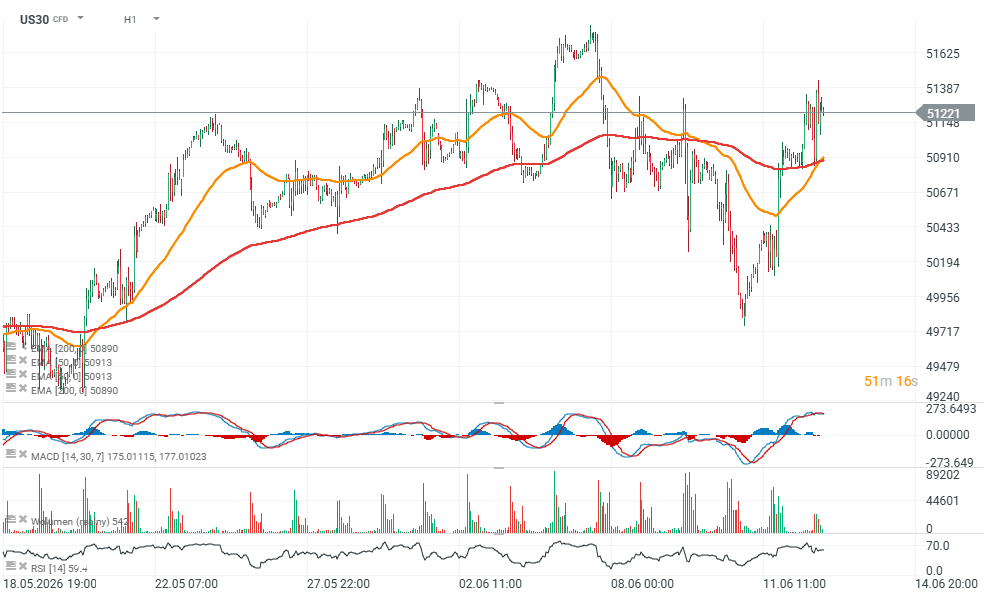

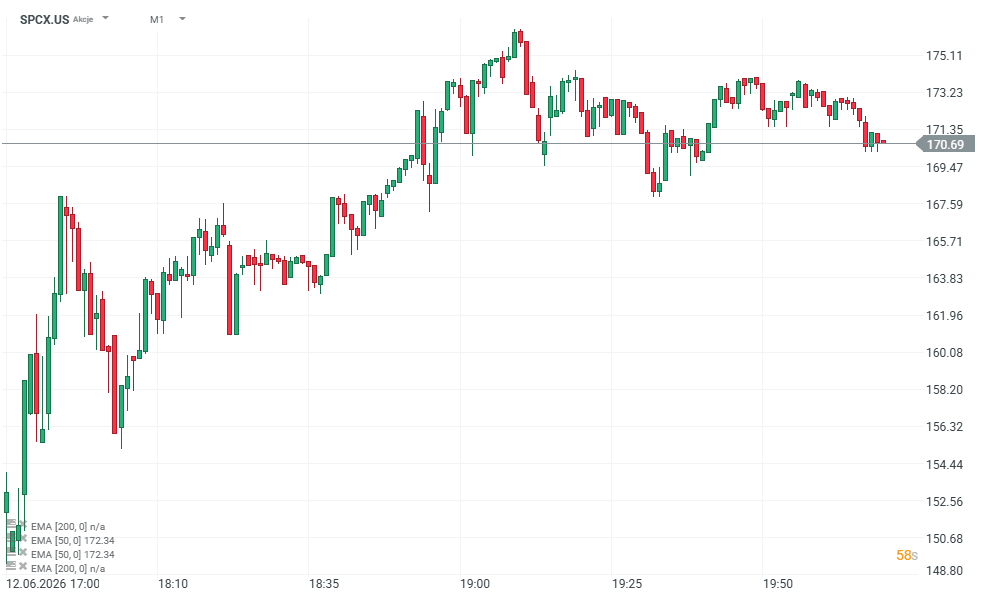

US30, SPCX.US (interval H1, M1)

Source: xStation5

Source: xStation5

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

🔼 DE40 gains amid SAP earnings

Economic Calendar: Industry’s condition in the shadow of oil prices