- Germany’s DAX fell more than 1% today, the UK’s FTSE dropped over 0.85%, and France’s CAC40 declined 0.65%, following mixed final PMI services readings across European economies. Sentix data pointed to a sharp deterioration in business and investor sentiment in the eurozone, falling to levels not seen since April 2025 (-19.2 vs -8 expected and -3.1 previously).

- U.S. equity indices recovered part of their initial losses, with S&P 500 futures down 0.3% compared to a drop of over 1% shortly after the opening. U.S. durable goods orders fell by 1.4% month-over-month, more than the expected -1.2% decline after 0% previously. However, core orders (excluding transportation) rose by 0.8% versus expectations of 0.5%. One-year inflation expectations according to the NY Fed increased to 3.4% (vs 3.5% forecast and 3% previously), while Fed’s Austan Goolsbee warned of real inflation risks stemming from rising fuel prices, which could weigh on growth and complicate the fight against inflation.

- John Williams of the Fed maintained a relatively calm tone despite higher readings. He emphasized that monetary policy remains appropriate, suggesting no need to react to a single inflation shock. He also indicated that inflation could reach around 2.75% in 2026, with more pronounced pressure in the middle of the year. The current interest rate range stands at 3.5% - 3.75%, and the Fed continues to signal one rate cut this year

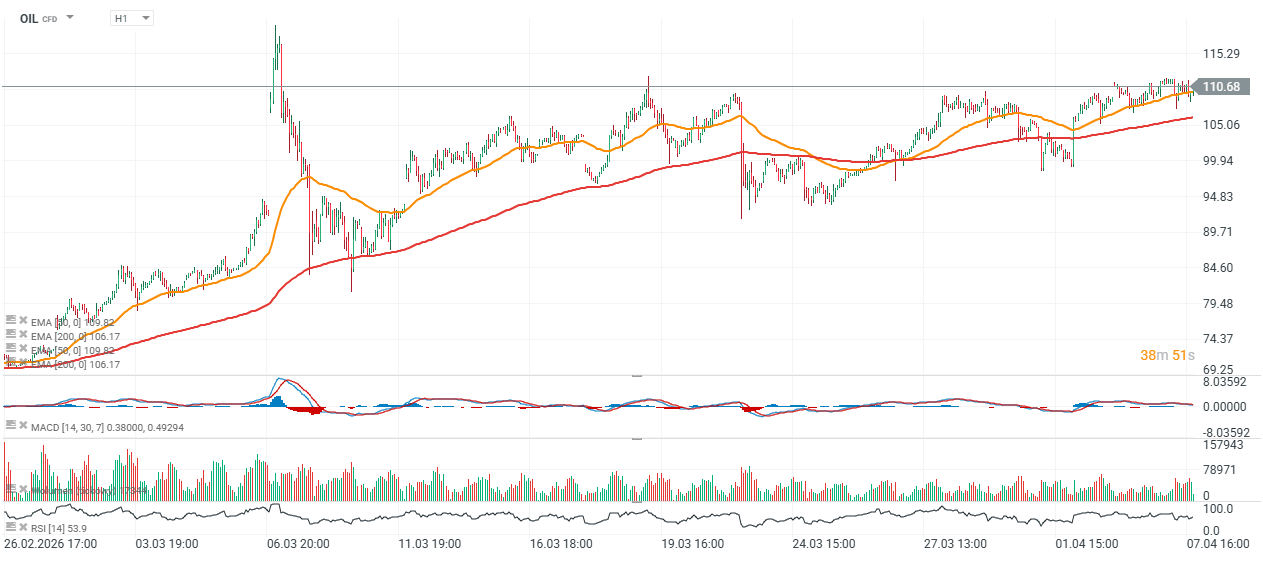

- Trump has threatened massive strikes against Iran but maintains that the situation could still change before a final decision on military action is made. Iran previously announced it had withdrawn from talks with the United States following the president’s threats, and aside from Axios reports, there is no clear confirmation of ongoing negotiations between the sides. Oil remains near $110 per barrel, suggesting that investors do not see a near-term resolution regarding the reopening of the Strait of Hormuz.

- Gold is gaining 0.5%, rising to $4,650 per ounce, while EURUSD jumps 0.3%. Cryptocurrencies are losing momentum. Bitcoin failed to break above $70,000 and has pulled back to around $68,500 today. Meanwhile, cocoa futures on ICE are falling nearly 7%, partly driven by a stronger U.S. dollar.

- Bank of America analysts have added Microsoft shares to their list of top U.S. picks, but the stock is not seeing any significant rebound in response to the news. Sentiment in the technology sector remains weak. Broadcom stands out with strong gains, rising 5% following a chip deal with Google and Anthropic, while UnitedHealth Group is also surging, with the insurance giant up 10% today.

- Oil continues its upward trend, holding around $110 per barrel ahead of a potential U.S. strike on Iran announced by Donald Trump. According to the statement, the attack is expected to begin on Wednesday around 2 a.m. Polish time. Iran has warned of an unprecedented retaliation targeting neighboring countries and relevant infrastructure. Iranian officials claim Tehran has over 45,000 drones and several thousand missiles at its disposal, with stockpiles described as “far from depleted.” Meanwhile, the Pentagon maintains that Iran’s military is weak and incapable of achieving victory.

Source: xStation5

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

Silver breaks above $59 and attracts capital again. Gold remains in the shadow of its younger sibling