Key US indices remain close to their opening levels today. The S&P 500 is up by 0.1%, while the NASDAQ Composite has gained 0.2%. Oil prices also remain stable – Brent crude is trading slightly below $80, while WTI oscillates around $77. There are no major developments in the currency market either, with the dollar recording modest gains.

President Trump's chaotic statements regarding the agreement with Iran, set to be signed this Friday, have not triggered greater volatility. Attention is fully focused on the fast-approaching Fed meeting. It is not expected to bring a change in interest rates – or at least that is what the markets assume. However, ahead of us is the publication of the new interest rate projections (Dot Plot) and, crucially, the first conference by the new chairman – Kevin Warsh.

- The decision will be published at 7 PM UK time.

- It will be accompanied by the Dot Plot, which is the Committee's interest rate projection.

- We will also receive new forecasts for economic growth and inflation.

- At 7:30 UK time, Kevin Warsh will take the podium.

Monetary Policy

The chairman chosen by Trump will face a difficult task. Many expect him to want to appease the president by adopting a dovish tone. At the same time, his message will be meticulously assessed by analysts worldwide, who will be watching whether the discrepancy between Warsh's communications and the signals coming from the rest of the Committee is significant. If this is the case, the new chairman may lose investor confidence right at the start; thus, it seems unlikely that he would decide on a very sharp shift in rhetoric.

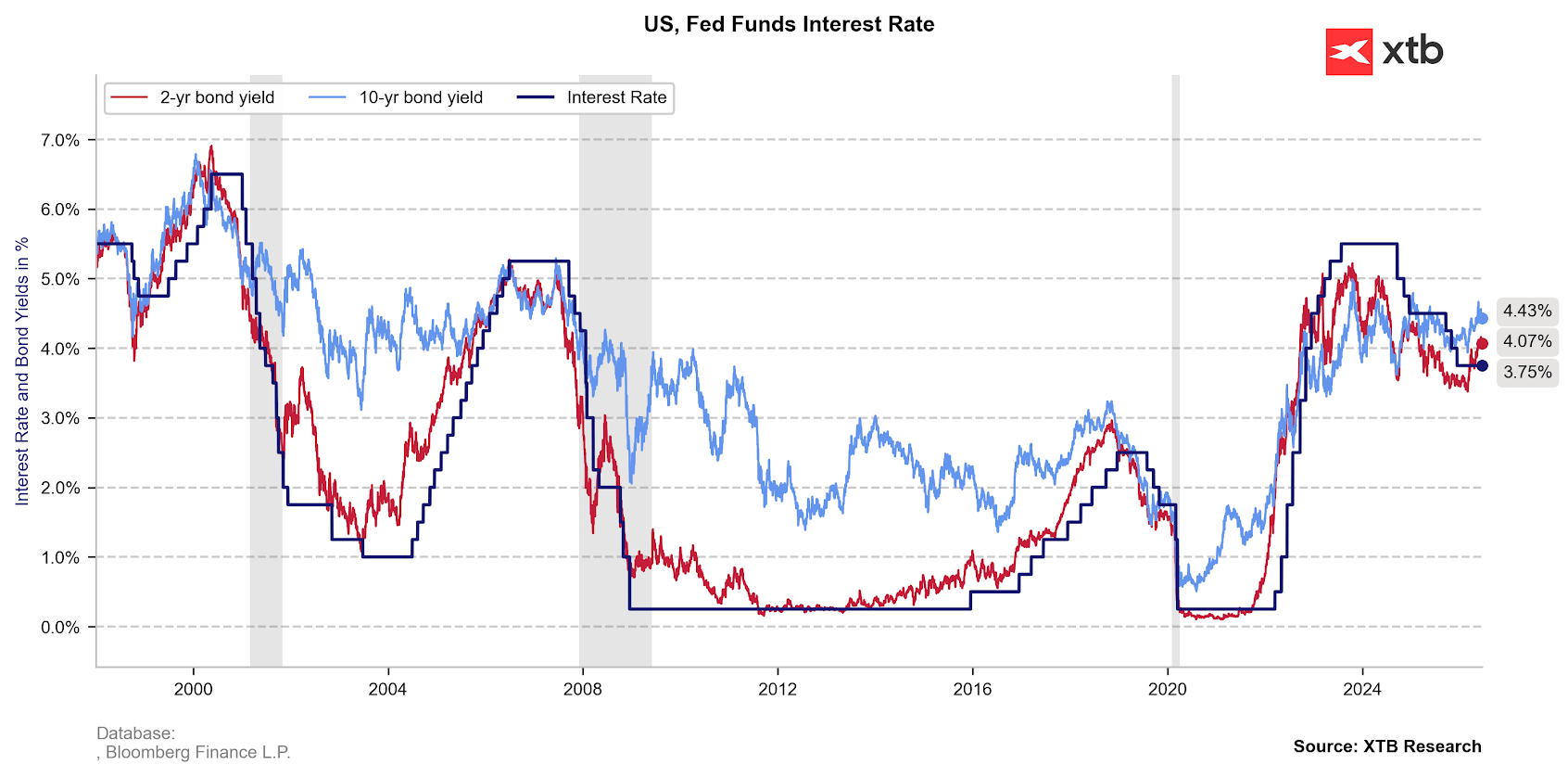

Figure 1: US Interest rates and bond yields (1998 - 2026)

Source: XTB Research, 17.06.2026

Source: XTB Research, 17.06.2026

Current conditions do not seem to allow for this, although the signing of the memorandum between the USA and Iran scheduled for Friday should slightly ease Warsh's task, allowing him to take a more detached approach regarding the recently prioritised inflation risks. What is crucial – his statements will be confronted with the Committee's interest rate projection (Dot Plot).

Geopolitics

As we wrote in today's US Open, President Trump continued his chaotic communication regarding the agreement with Iran today. At the G7 summit in Evian, France, on the one hand, he emphasised that the Strait of Hormuz would be opened within a day or two, while on the other, he noted that the memorandum with Iran does not constitute a final agreement and that if "he doesn't like what he sees, he will attack (Iran) again". However, markets do not currently seem to attach too much weight to his words.

The signing of the document is scheduled for Friday. The actual return of maritime traffic in the Strait will be a significant stimulus for the markets – despite all assurances from the White House, investors remain distrustful regarding the conclusion of the American-Iranian saga.

Commodities

In the absence of major news in the Middle East, the relative stability of key energy commodity prices is not surprising. LNG continued its decline – TTF below 42%, NATGAS around $3.17.

We observe modest increases in crude oil (+0.7-0.9%). In part, this can be attributed to the large drop in its inventories shown by the EIA report (-8.3M compared to the consensus of -3M).

- Such a strong deviation from expectations results primarily from a sharp drop in oil imports and high refinery utilisation – oil throughput increased to 17.2 million barrels per day, and refinery capacity utilisation reached 96.7%.

- You can read more on this topic in Kamil Szczepański's commentary titled "BREAKING: Big drop in oil inventories, Brent back above $80", which is available on the platform.

Modest gains were also observed in gold (+0.6%) and silver (+0.8%), which are benefiting from the decline in Treasury yields in major economies. For this reason, today's FOMC meeting could be a significant test for both precious metals.

Stock Market

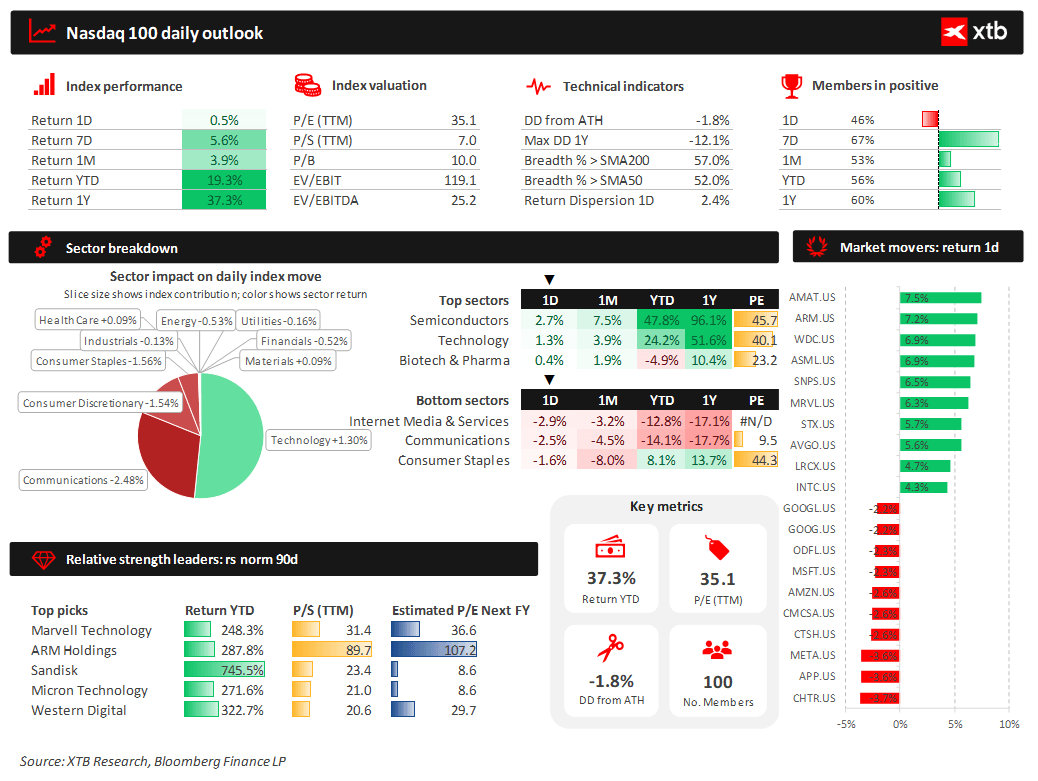

Lack of a clear direction. The semiconductor industry is recovering losses, led by Applied Materials (7.5%). The agreement announced by the company with Essilor Luxottica is intended to bring highly technologically advanced glasses powered by AR and AI systems. The company is also favoured by analysts raising their price targets.

Figure 2: Dashboard for Nasdaq 100 (17.06.2026)

Source: XTB Research, 17.06.2026

Source: XTB Research, 17.06.2026

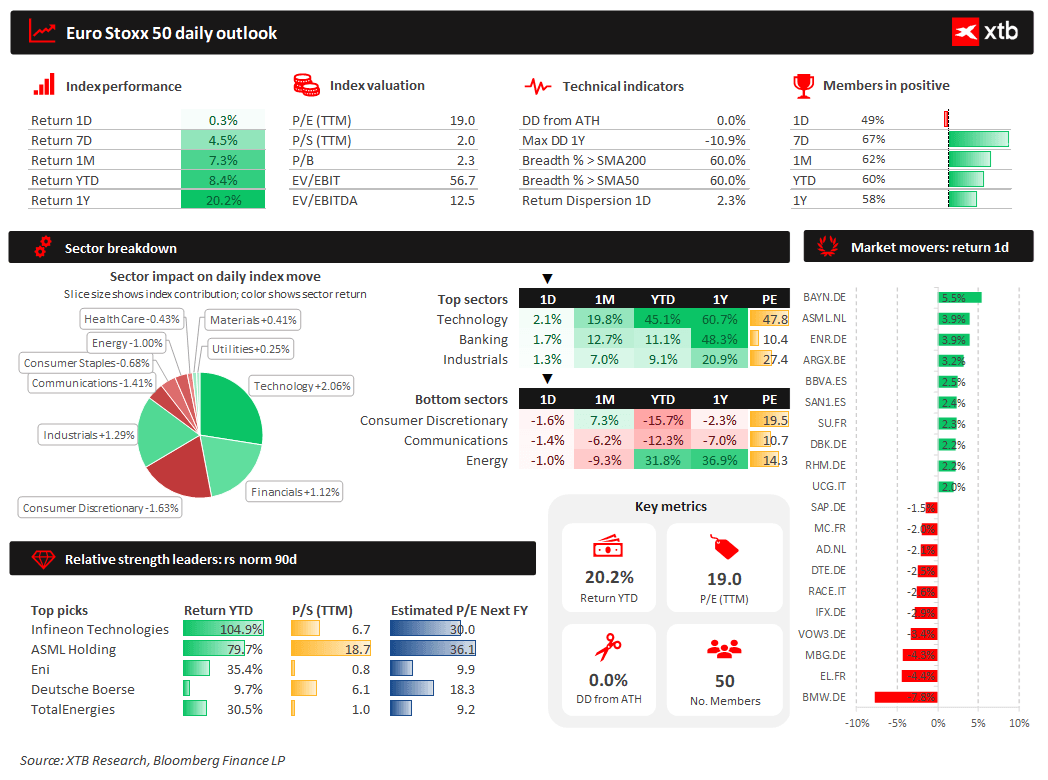

Europe largely closed the day with small gains. The Euro Stoxx 50 index (+0.3%) and the German DAX (+0.1%) strengthened – despite a substantial weakening recorded by BMW shares (-7.8%). The automotive giant came under pressure after lowering its annual profit forecast, exerting pressure on other companies in the sector, such as Volkswagen or Mercedes-Benz.

Figure 3: Dashboard for Euro Stoxx 50 (17.06.2026)

Source: XTB Research, 17.06.2026

Source: XTB Research, 17.06.2026

Macroeconomic Data

American retail sales data surprised to the upside. On an annual basis, we recorded an increase of 6.9%, and 0.9% on a monthly basis. Data from the control group (+0.7% m/m) was also above expectations, confirming that the growth momentum is not just a consequence of higher prices at petrol stations.

The strength of the American consumer is certainly good news for the US economy, although it should be remembered that this occurs largely at the expense of savings. Furthermore, we observe immense stratification in this area. Consumption growth in the lowest-earning third is increasing much more slowly.

—

Michał Jóźwiak, Financial Market Analyst at XTB

France Challenges Palantir, Market Reacts.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices