The European markets have been quite volatile, with an early panic driven by weak results from Dutch chipmaker ASML, followed by a steady recovery. Most of the major indices are currently trading in the green (DAX: +0.37%, FTSE 100: +0.28%, FTSE MIB: +0.24%, IBX35: +0.58%, SMI: +0.4%), with the exception of French CAC40, trading flat after the proposition of 2026 budget featuring austerity measures.

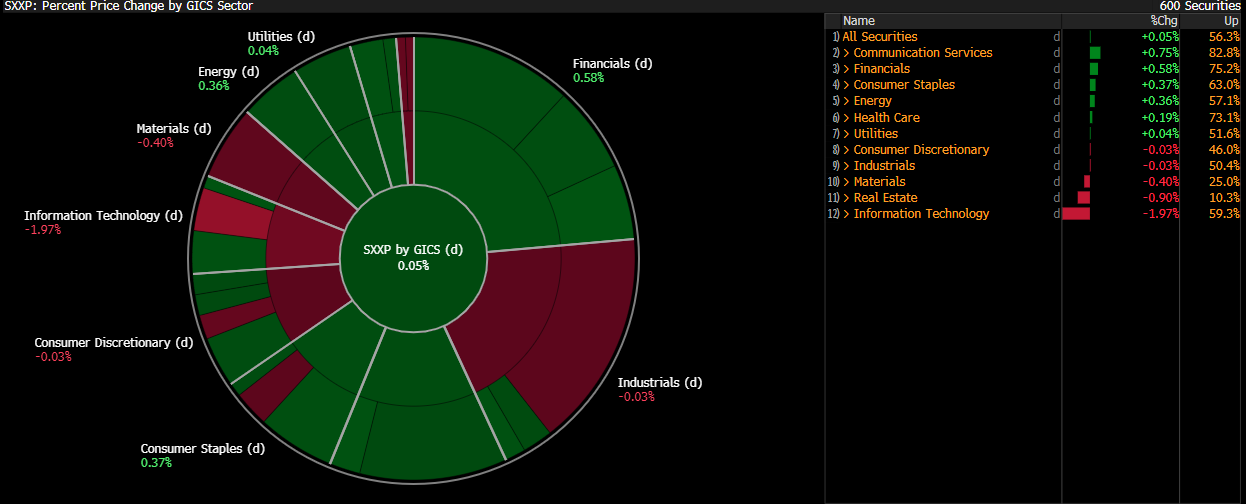

The telecoms and financial institutions are the best performers during today’s session, counterbalancing the overall weakness of tech stocks (with the major exception of German giant SAP, currently up 1.1%). Healthcare and energy extend gains.

Regarding political news we have new advances in German fiscal expansion. Germany has agreed with the European Commission on a multi-year fiscal plan allowing increased investment through 2029 while committing to tighter spending afterward. Using flexibility in the EU’s revised fiscal rules, Germany will boost spending on infrastructure, security, and defense in the short term, then slow expenditure growth. The plan balances investment, structural reforms, and fiscal consolidation, aiming for sustainable public finances and economic growth, with Cabinet approval expected soon.

Volatility in Euro Stoxx 600 sectors. Source: Bloomberg Finance LP

Today’s performance of DAX-listed companies. Source: xStation5

DE40 (H4)

DAX futures have fully recovered their early losses and are currently trading 0.45% above yesterday’s close. Buyers stepped in just below the 100-period exponential moving average (EMA100, dark purple) after the price reached the 78.6% Fibonacci retracement level. The contract is now approaching a key resistance near the 30-period EMA (EMA30, light purple). A break above the recently tested 24,330–24,380 range could spark a rally toward record highs. Otherwise, we may see the price consolidate within the current range defined by these EMAs.

Source: xStation5

Company news:

-

ASML shares fell over 8.2%, heading for their steepest drop since April, despite second-quarter results beating expectations. The sell-off was triggered by management’s caution that 2026 growth is no longer assured due to macro uncertainty, especially U.S. tariffs impacting customer sentiment. CEO Christophe Fouquet noted that while AI-related demand remains strong, the company “cannot confirm” 2026 growth. This shift contrasts with April’s more optimistic tone and overshadowed solid 2025 forecasts, shaking investor confidence despite healthy current bookings and margin performance.

-

Bakkafrost shares plunged up to 15%, the most since mid-2023, after flagging a major 2Q earnings miss. Preliminary operational EBIT came in at DKK65m, far below the DKK251m consensus. DNB Carnegie warns of “material EPS cuts” for 2025 and shaken confidence for 2026–27. One-offs linked to disease-related mortality in Scottish operations contributed, though even without them, results missed estimates by nearly 40%. Full earnings are due August 26.

-

Fuchs shares slumped 13.25%, the steepest drop since 2011, after 2Q EBIT missed estimates and the company cut its full-year outlook. It now sees 2025 revenue at €3.53bn and EBIT at €434m—both below consensus. Weaker industrial production, US-driven tariff concerns, and geopolitical tensions hurt demand. Analysts expect further self-help measures. Despite the disappointment, Jefferies remains positive long-term, citing FUCHS100 strategy and low capex needs. Interim results are due later this month.

-

Renault plunged up to 18% after cutting its 2025 margin and cash flow outlook and naming CFO Duncan Minto interim CEO following Luca de Meo’s exit. Weaker demand, rising Chinese competition, and stalled EV progress cloud the turnaround, unsettling investors and dragging down auto peers.

-

Sanofi received FDA fast track designation for SAR446597, a one-time gene therapy targeting geographic atrophy, an advanced form of dry age-related macular degeneration that can cause permanent vision loss. Shares are up 0.8%

-

Stellantis plans to halt investment in hydrogen joint venture Symbio by 2026, per Michelin and Forvia. The move threatens Symbio’s future, as Stellantis makes up ~80% of its business. Hydrogen costs, infrastructure gaps, and EV momentum likely influenced the decision. Michelin called the move “sudden” and warned of major operational and workforce risks. The stock is down 3.2%

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!