Today, markets will primarily react to geopolitical developments: the start of the U.S. blockade of Iranian ports at 2:00 p.m. GMT could keep volatility high and support oil prices, while any news of de-escalation or a maritime incident will immediately shift market sentiment. In Europe, the market open remains under pressure from risk factors, so investors will be focusing mainly on stock indices, the dollar, and energy commodities, as these will best indicate whether fears of further escalation are growing.

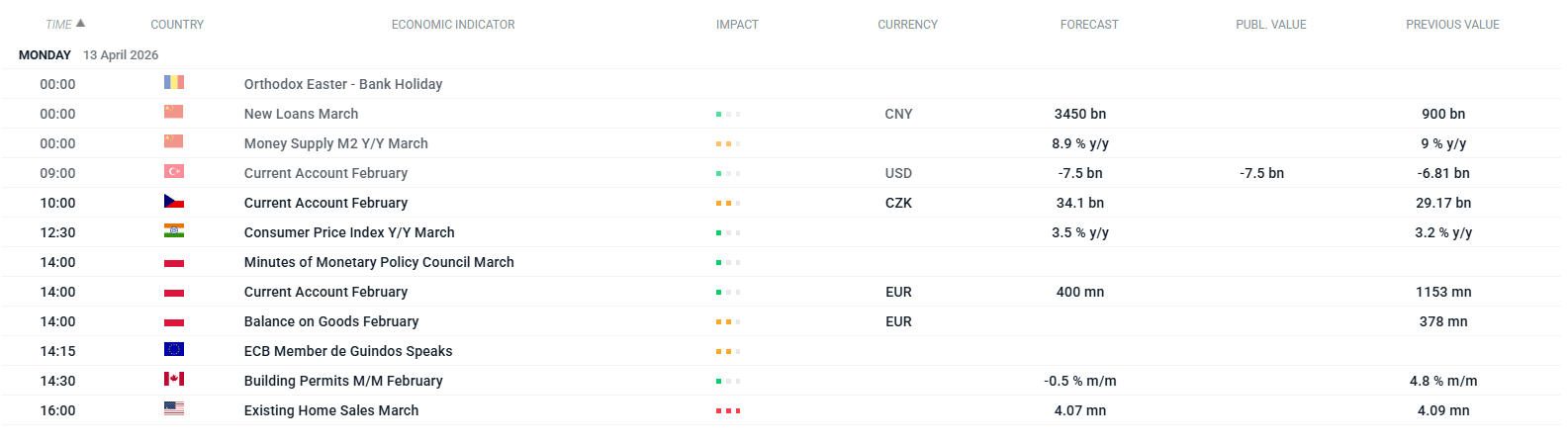

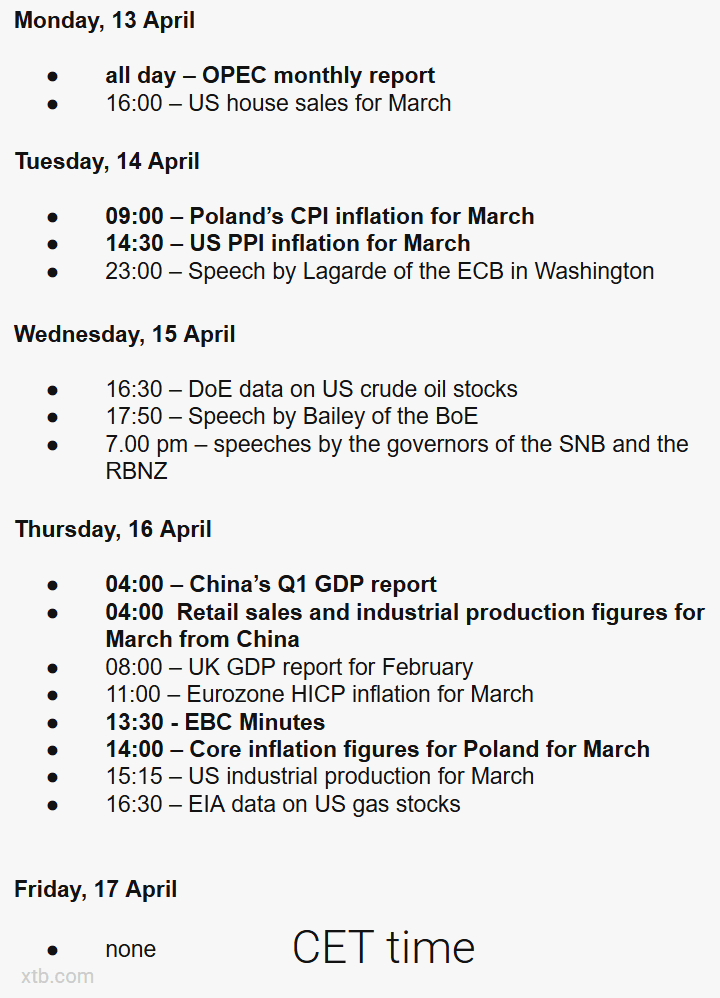

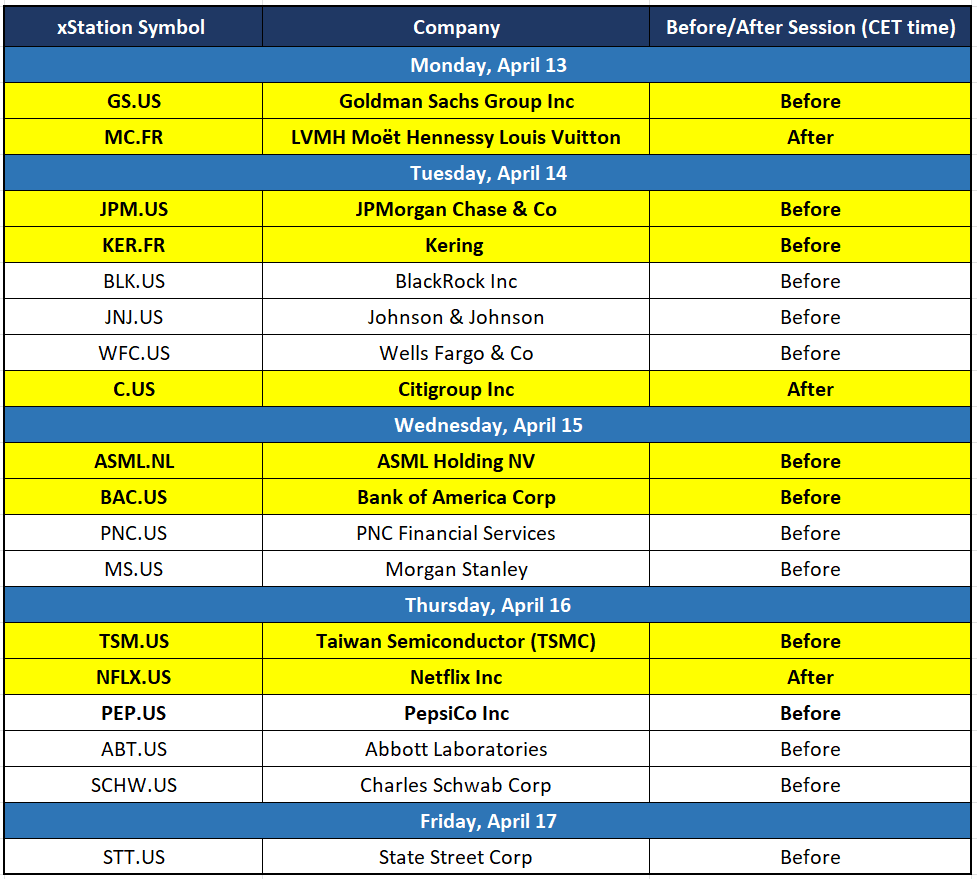

Over the course of the week, three things will be key: developments regarding Iran, the start of the Q1 earnings season, and macroeconomic data from the U.S. and Europe, which could either confirm or undermine the impact of higher oil prices on inflation. The list of upcoming releases includes Poland’s CPI, the US PPI, home sales data, the ECB Minutes, eurozone HICP inflation, and readings from China, so the market will be navigating geopolitics, inflation, and growth prospects all at once. Particular attention will be focused on banks, LVMH, ASML, TSMC, and Netflix, as their results will provide the first indication of how companies are faring at the start of the earnings season.

Today's calendar. Source: XTB

Weekly calendar. Source: XTB

Corporate calendar. Source: XTB

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!