Economic calendar

- 3 PM GMT, US ISM Services, March: expected at 54.9 vs. 56.1 previously

- Prices Index: expected at 67 vs. 63 previously

- New Orders: expected at 56.8 vs. 58.6 previously

- Employment: expected at 51.0 vs. 51.6 previously

- 6 PM GMT, Donald Trump speech related to the war in Iran

A meaningful increase in the prices sub-index should be expected. The larger the gap between that component and indicators such as new orders or labor market conditions, the more credible the risk of a stagflationary backdrop in the economy becomes. Higher fuel prices mean lower disposable income for millions of households, a dynamic that has historically often coincided with market corrections or bear markets.

Importantly, the prices sub-index does not affect the composite ISM headline directly, which may increase the likelihood of a more pronounced correction in the overall index. At the same time, a sharp downside surprise does not appear particularly likely after stronger-than-expected regional releases from the Dallas Fed, Philly Fed, Empire State, Richmond Fed, and Kansas City Fed, all of which came in above expectations. The prices index could rise to levels not seen since 2022.

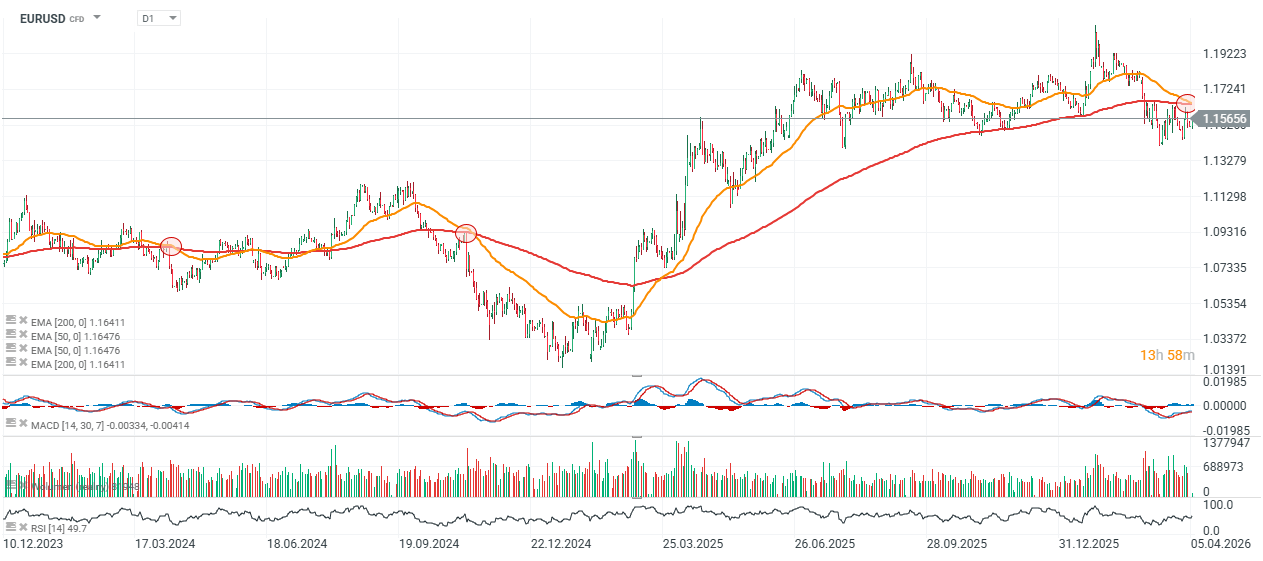

EUR/USD (D1 timeframe)

A strong ISM reading combined with a sharp rise in the prices index could weigh materially on EUR/USD and potentially trigger a bearish impulse in the pair. It is worth stressing that the US economy is significantly more resilient to an energy shock than Europe and is less exposed to fuel supply disruptions. On the other hand, weakness across the main ISM benchmarks, excluding prices, could point to a continuation of consolidation within the 1.15 - 1.16 range.

Source: xStation5

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

Economic Calendar: What Could Move the Market This Week? (03.08.2026)