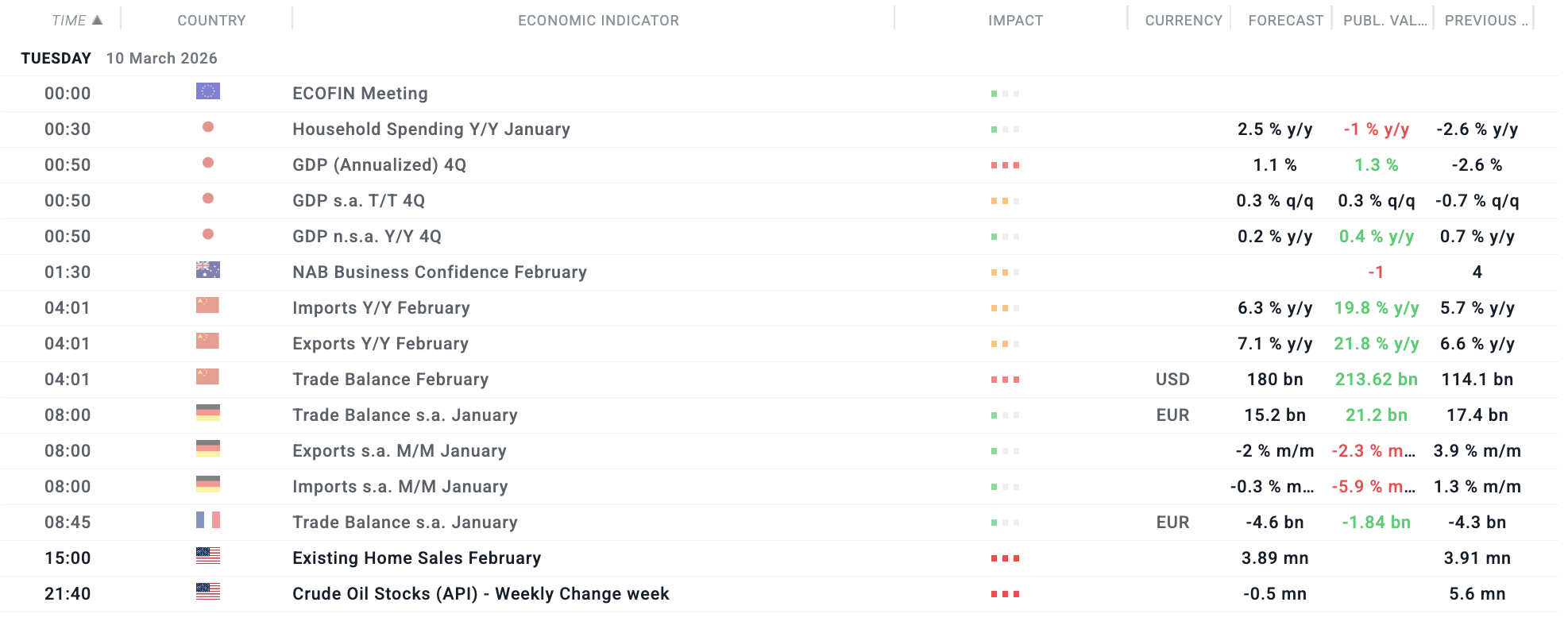

After digesting a heavy batch of data from Asian heavyweights—including Japan's GDP rebound and China’s record trade surplus—alongside fresh Eurozone trade figures, Tuesday’s macro calendar is now virtually empty. This silence is sharpening the market's focus on the fast-moving developments in the Iran war.

We are seeing a temporary breather in the oil market and a bump in risk currencies like the AUD, but the current optimism is fragile. While Donald Trump’s suggestions that the war could be "over soon" provided a welcome boost to sentiment today, words alone may not be enough to sustain a long-term rally if Iran continues its military defiance.

The only significant data point remaining is the crude oil inventory report. Given the recent surge in volatility—with Brent crude currently trading near $89.50 following a sharp plunge from $120—investors are highly sensitized to any data that might impact supply.

All times CET. Filtered by: US, UK, France, Germany, Eurozone, Japan, Australia, New Zealand, China, Canada. Source: xStation5

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains