Today's release of the FOMC minutes from the US central bank's May 1 meeting has a chance to raise volatility on the dollar and equity markets - provided it contains comments that provide more clarity or to some extent surprise previous market expectations. Since the beginning of May, however, we have learned a lot of macro readings, indicating a gradual cooling of the US economy so the 'hawkish' tone of the minutes could (theoretically) be considered 'outdated (although the components of the latest US CPI were not dovish at all), and the dovish tone could increase pressure on the dollar and yields.

- If the record suggests a more dovish stance, theoretically the dollar could weaken, Wall Street could gain and expectations for policy easing could rise because a slew of data from the US, since the beginning of the month, has pointed to a slowdown and a weaker consumer, and the latest CPI came in marginally lower, after a series of several higher-than-forecast readings in a row.

- On the other hand, the evidently hawkish message, surprisingly at odds in some ways with Powell's own posturing, may suggest that the Fed is seriously considering no rate cuts this year, and that elevated services inflation and the soon-to-be fading 'disinflationary' base effect from 'rents' may determine a 'higher for longer' policy. However, the FOMC minutes do not seem to shed more light on whether the Fed, on the wave of higher inflation data, will realistically consider raising rates in the months ahead. After all, Powell in May chose not to communicate such a scenario to the markets. What's more, recent weak data has definitely reduced the chances of such a scenario.

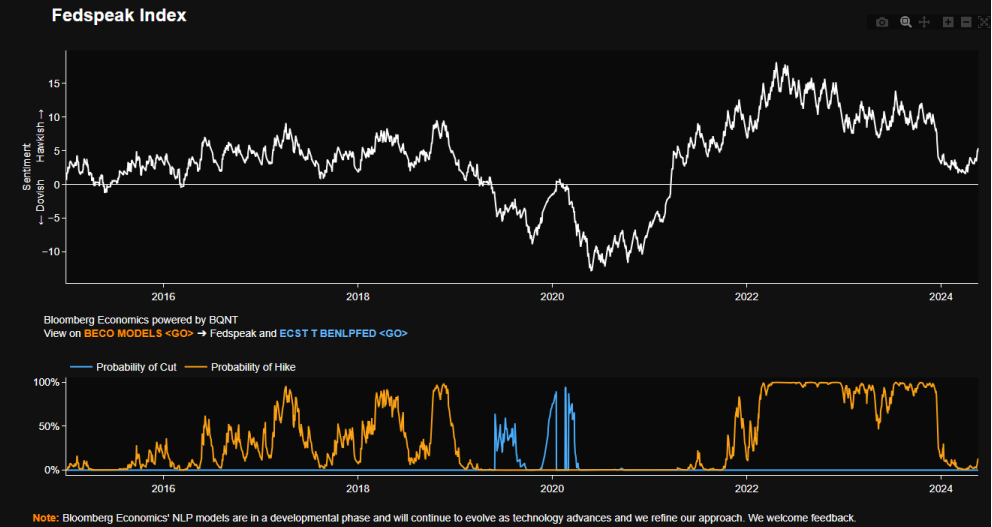

An index tracking the tone of Fed members' statements recently rose signaling a 'small' hawkish turn, on a wave of consistently higher inflation readings and persistent data from services, from which it is difficult to 'root out' price pressures, with a strong labor market and higher wages. Inflation in services rose 4.9% in April, up from 4.8% in March. On the other hand, it seems clear that these readings were required to communicate a change of attitude at the Fed. The question - will this change prove to be permanent? Source: Bloomberg Finance LP

Costs of hawkish policy rising?

Behind the prevailing optimism around a 'soft landing' is the prevailing belief that improving supply-side factors are lowering inflation, without much cost to the labor market. Announced earlier, the tapering of quantitative tightening (QT) in June is likely to be viewed as a way to ease ongoing balance sheet reduction, rather than stopping it or reducing the scale. Nevertheless, Powell's May speech was perceived as dovish; it saw yields on two-year US treasuries fall 8 basis points. Powell's baseline stance in May, however, has not changed; it is still to maintain restrictive policy at the Fed for as long as necessary. It does not seem that recently released macro data can 'stir' this belief 'in favor' of the dollar. It seems that the chances of a recent reduction have indeed increased (and of a rate hike - dismissed) but not without 'costs' in the form of a cooling economy and a more cautious consumer (strong performance of Walmart discounters, weakness at Target).

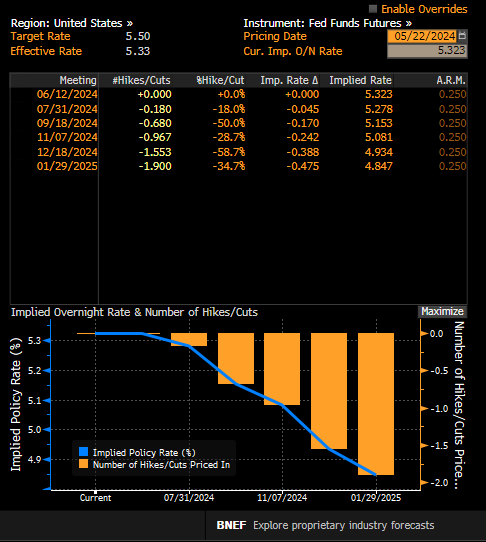

Wall Street expects the Fed's downward pressure on rates to increase, with US rates near 5% by early 2025. Without significant inflammatory factors in the economy such as an oil supply shock or a stronger economic slowdown and systemic shocks, the current consensus assuming very cautious policy easing in the US seems largely justified. Source: Bloomberg Finance LP

What to expect?

- In almost every summary of forecasts issued over the past five years or more, the median Fed participant has maintained an estimated long-term US GDP growth rate of 1.8%. There may be some upward or downward revisions here in the minutes

- Data from Fed members' speeches suggest that there is an ongoing discussion at the Federal Reserve about the size of the neutral interest rate (10 mentions among 50 Fed members' speeches since May 1), which may have risen since the pandemic.

- Currently, SOFR futures imply a long-term nominal interest rate of 3.5%-3.6%, which corresponds to a neutral rate around 1.5%-1.6% versus 0.5%, in 2019, before the pandemic.

- Almost certainly, only a small group of Fed members see a slowdown in the labor market as likely, while Bloomberg Intelligence expects the disinflationary trend to continue according to most Fed members throughout 2024. There are also likely to be references to the beneficial effect of higher immigration on inflation and economic growth.

- Jerome Powell may turn out to be more dovish compared to other FOMC members, believing that favorable supply-side factors will lower inflation without compounding the negative effects on the economy. On the other hand, recent data suggesting a weaker U.S. economy may cause Wall Street to start considering a 'potential mistake' in Powell's stance, and look closely at what the other Fed members are saying.

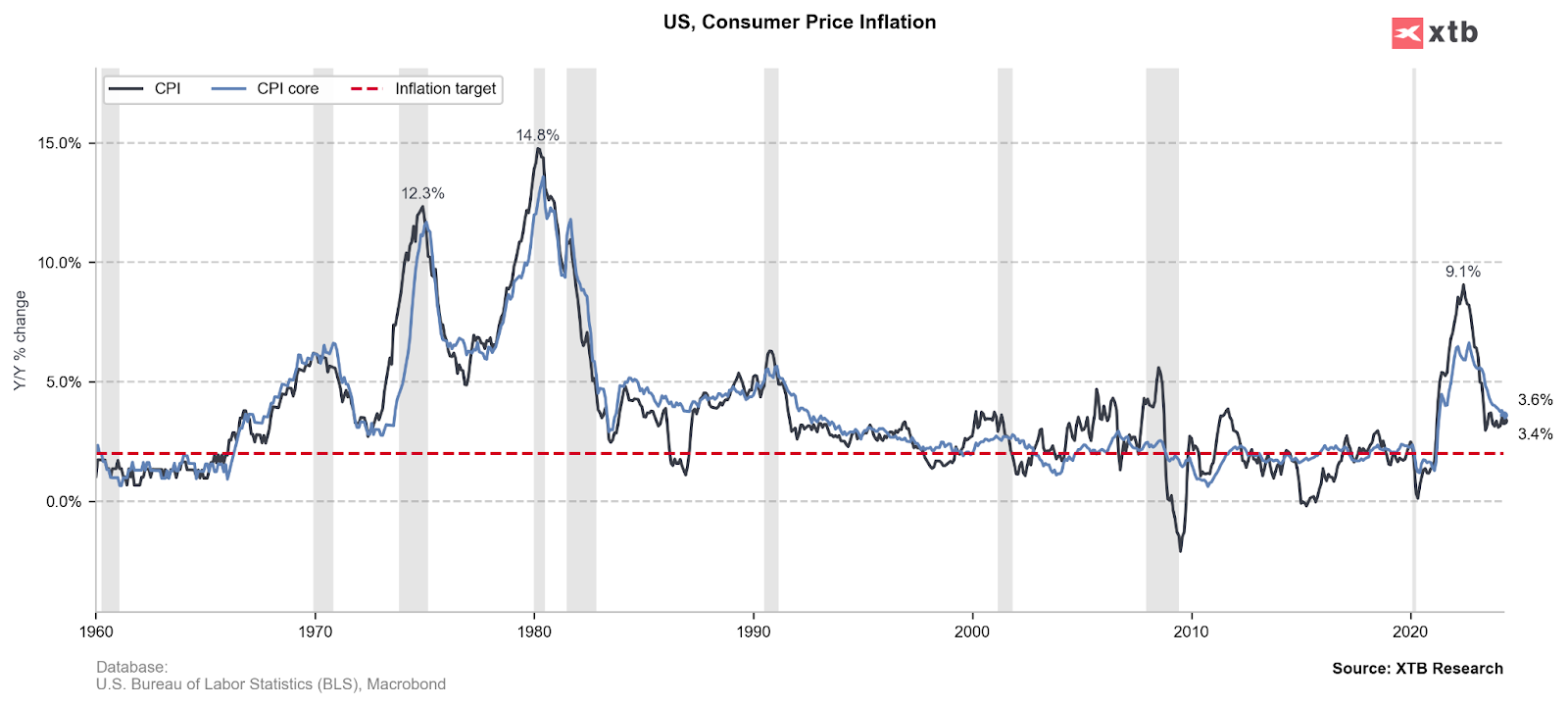

The latest CPI readings came out nominally quite positive, but soon rental prices will stop adding to the downward momentum of the CPI, and inflation in services came in at 4.9% vs. 4.8% previously, giving the Federal Reserve a case for maintaining restrictive policy. Source: XTB Research

Summary

The FOMC minutes should show a consensus at the Fed that interest rates are restrictive - though not necessarily whether they are restrictive enough. However, recent macro readings from the world's largest economy may suggest that the biggest 'hawks' at the Fed may have changed or are considering a change of heart relative to May 1, and in June they will not be convinced that a rate hike would really be adequate. Most important for the markets, Jerome Powell may turn out to be one of the biggest optimists at the Fed, regarding the impact of favorable supply-side factors lowering inflation, without affecting the labor market. However, if the trend of recent weak readings from the US continues, the market may begin to price in a possible 'Powell mistake.

EURUSD (D1 interval)

Recent data from the United States has been noticeably weaker, but the situation in Europe looks no better. With a likely ECB pivot in June confirmed by Christine Lagarde's comments today, pressure on the EURUSD could return as long as the US central bank maintains a hawkish stance - and recent weaker data readings suggesting more cautious consumers and the gradual impact of high rates on the US economy do not prove to be the 'new normal'.

Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡