Diplomatic communications, media reports, and independent analyses indicate that an escalation of the conflict between the United States and Iran is highly likely.

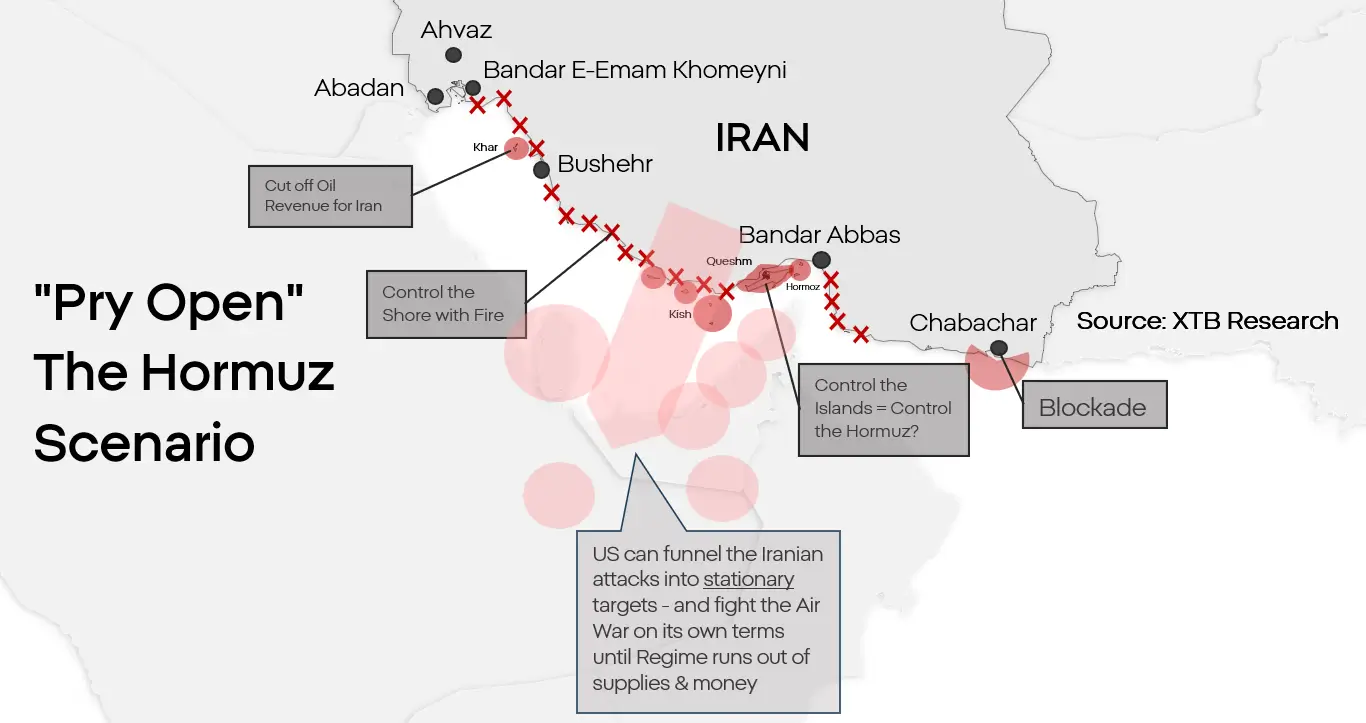

Iran’s geography is one of its greatest, if not its greatest, strengths. But it also creates a number of vulnerabilities. The vulnerability with the largest implications for the conflict, and the one that offers the United States the best gain-to-risk ratio, is Kharg Island.

This island, located about 30 kilometers off Iran’s coast, is its Achilles’ heel. Iran’s coastline is sparsely populated and poorly organized, but this is not a matter of choice, it is a matter of constraints. Iran’s coastal waters are too shallow for the mega tankers that form the backbone of the global economy to dock in Iranian ports.

Under these conditions, Iran is forced to transport its oil to a port on an island where tankers can pick it up. The island is small, only 8 square kilometers, about 2.5 times the size of Central Park in New York City. Despite its size, it handles 90% of Iran’s oil exports.

Realistically, if the United States wanted to make Iran’s leadership understand how unfavorable their military position is, it could seize the island. Even if U.S. losses are possible, it is not possible for Iran to repel a determined U.S. amphibious landing.

This matters because oil exports are one of the last lifelines of the Iranian economy. While a wartime economy can function much longer than most suspect, it is important to remember:

- Iran is a desert; the balance of available food and water has been on the edge of a humanitarian crisis for years and is gradually worsening.

- Iran’s industry is dispersed, inefficient, and neglected; it requires inputs from abroad.

- Iran has been operating under a wartime economic regime not for a year or two, but in practice since the 1970s.

A real threat still hangs over Iran: the loss of water and power infrastructure. Here, too, Iran is powerless against U.S. air power, and the destruction of already strained infrastructure in a desert country of 90 million citizens would have apocalyptic consequences.

After such a move, the United States might no longer have anyone left to negotiate with, but that is a last resort.

Leading indicators

Despite the chaotic nature of decision-making in Washington and Tehran, there are a number of qualitative signals that suggest the likelihood of escalation is increasing.:

- It is worth remembering that the United States has not withdrawn a large portion of its military assets from the Persian Gulf region, despite ceasefire arrangements. There is a significant probability that both sides, at the moment of signing the agreement, were calculating a convenient moment to break it.

- On July 10, Trump officially called the campaign in Iran a war and asked Congress for support. This clearly points to the long-term nature of the conflict.

- U.S. attacks are no longer focused solely on IRGC facilities. There have also been many strikes on Iran’s regular military, the Artesh. This indicates that this is no longer an operation to change the government using Iranians, but a long-term campaign aimed at degrading the Islamic Republic’s ability to project power.

Effects

The math is, at least superficially, simple:

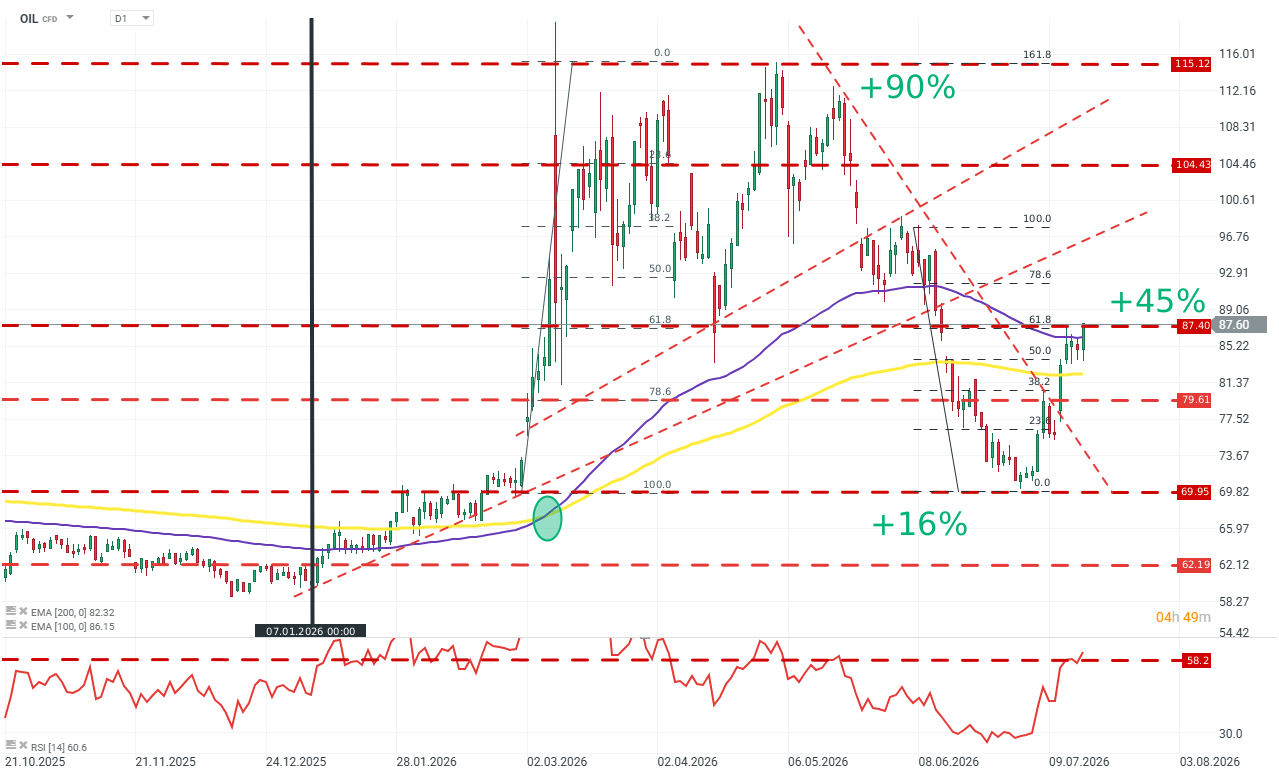

- About 25% of the supply of refined petroleum products came from the Persian Gulf region.

- The Strait of Hormuz, which is currently blocked, handled about 75% of the total volume.

- The blockade is not airtight; depending on circumstances, about 5 to 15% of the pre-war volume gets through the strait.

- This implies a reduction in global oil supply of about 16 to 18%. That would correspond fairly well to the roughly $72 per barrel level from late June and early July, an increase of about 18% compared with around $60 per barrel in December 2025.

The gradual release of reserves by (mainly) the United States and China would be enough to prevent an explosion in inflation, but the problem today is different.

What the global economy lacks most is not crude oil but fuel. There are currently no gasoline and diesel inventories large enough to suppress price increases over the long term in the face of a supply shock, and worse, refining capacity in the United States and Europe is currently too limited. The undeniable proof is the so-called crack spread at the highest level in recorded history.

What does all this mean?

- The price of oil already reflects significant, but not total, escalation.

- Gasoline prices do not reflect the tightness in the refined products market.

- The decline in inflation may prove temporary, and the next wave of increases may be delayed.

Kamil Szczepański

Financial Market Analyst at XTB

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

Morning Wrap: Oil Rises Again (07.08.2026)

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)