European equities opened Wednesday's session without a clear direction after the STOXX Europe 600 closed at a fresh all-time high in the previous session. Investors remain cautious ahead of two major macro events: the release of the Eurozone's preliminary June inflation data and speeches from the world's leading central bankers at the ECB Forum on Central Banking in Sintra, Portugal.

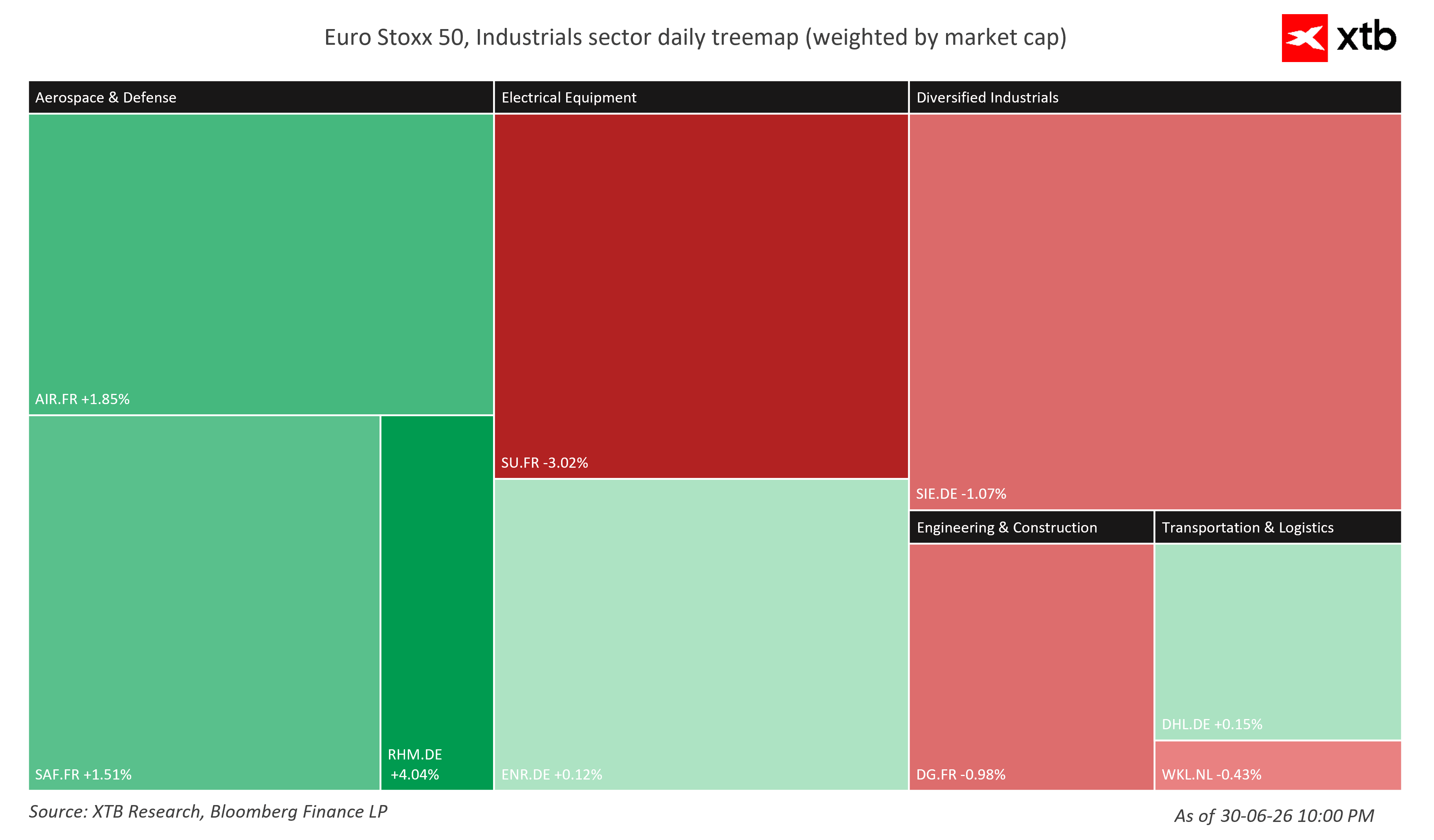

Defense stocks are among today's strongest performers. Shares of Rheinmetall are up around 4%, with RENK Group and Hensoldt also advancing sharply. The rally extends beyond Germany, lifting several French, British, and Norwegian defense companies as well. Meanwhile, crude oil is trading near multi-month lows at around $72 per barrel, providing additional support for global risk assets by easing inflation concerns.

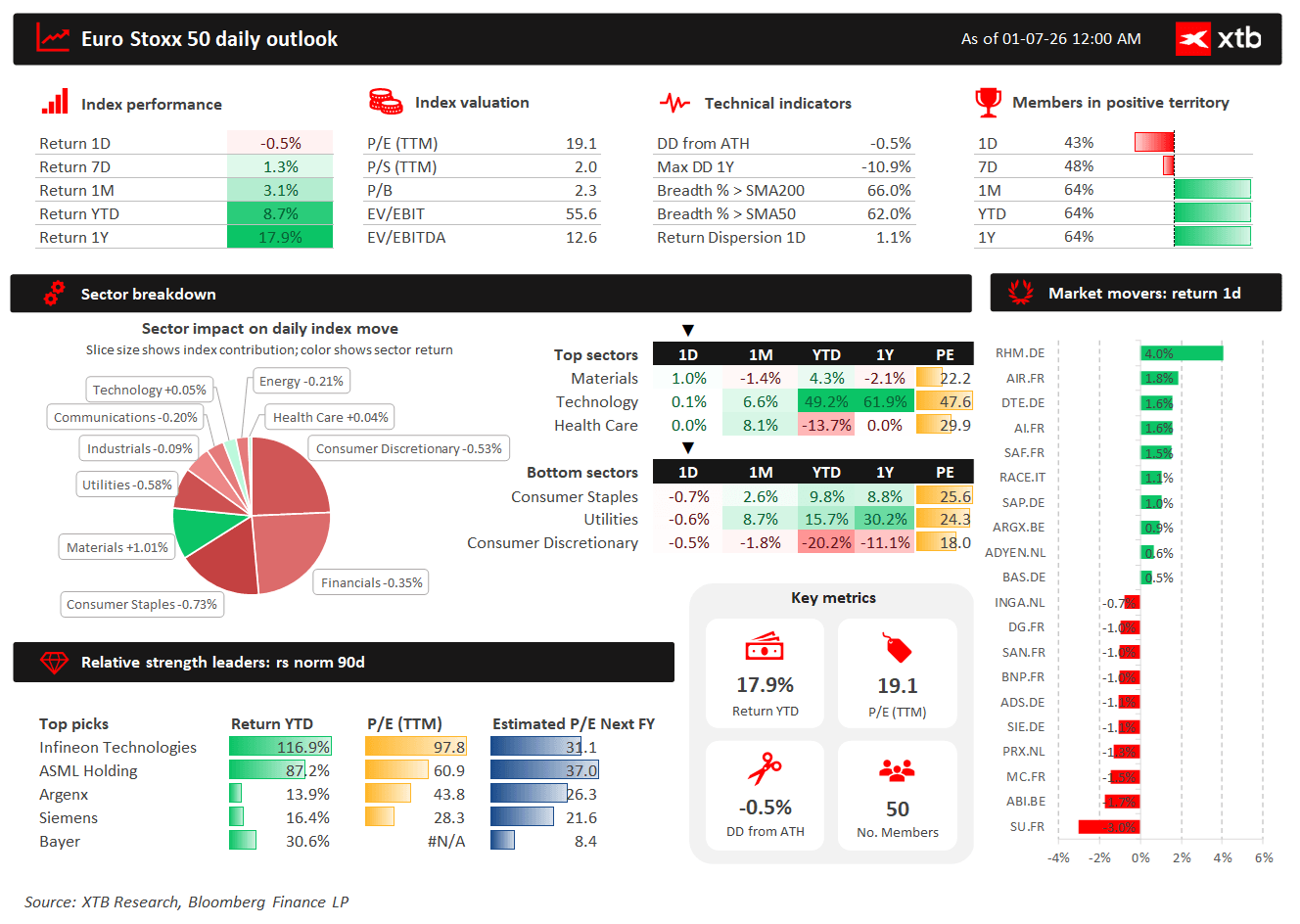

Key market moves

- Euro Stoxx 50: -0.5%

- STOXX Europe 600: -0.3%

- DAX: +0.2%

- CAC 40: -0.3%

- FTSE 100: -0.2%

- IBEX 35: -0.3%

- FTSE MIB: -0.3%

Today's price action lacks a clear trend. After a strong rally over recent weeks, investors appear to be taking profits while waiting for fresh macroeconomic catalysts that could determine the next move in European equities.

Source: XTB Research

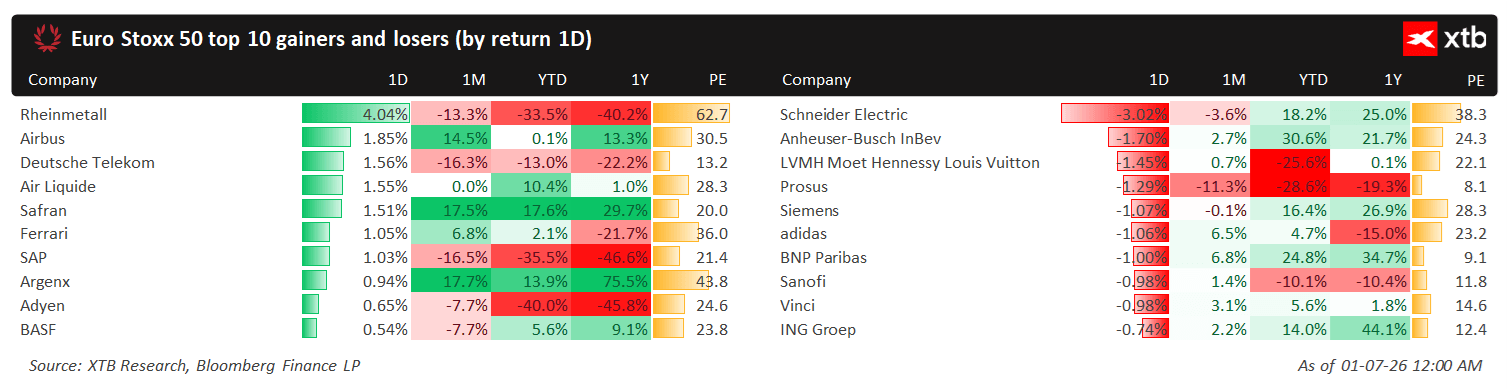

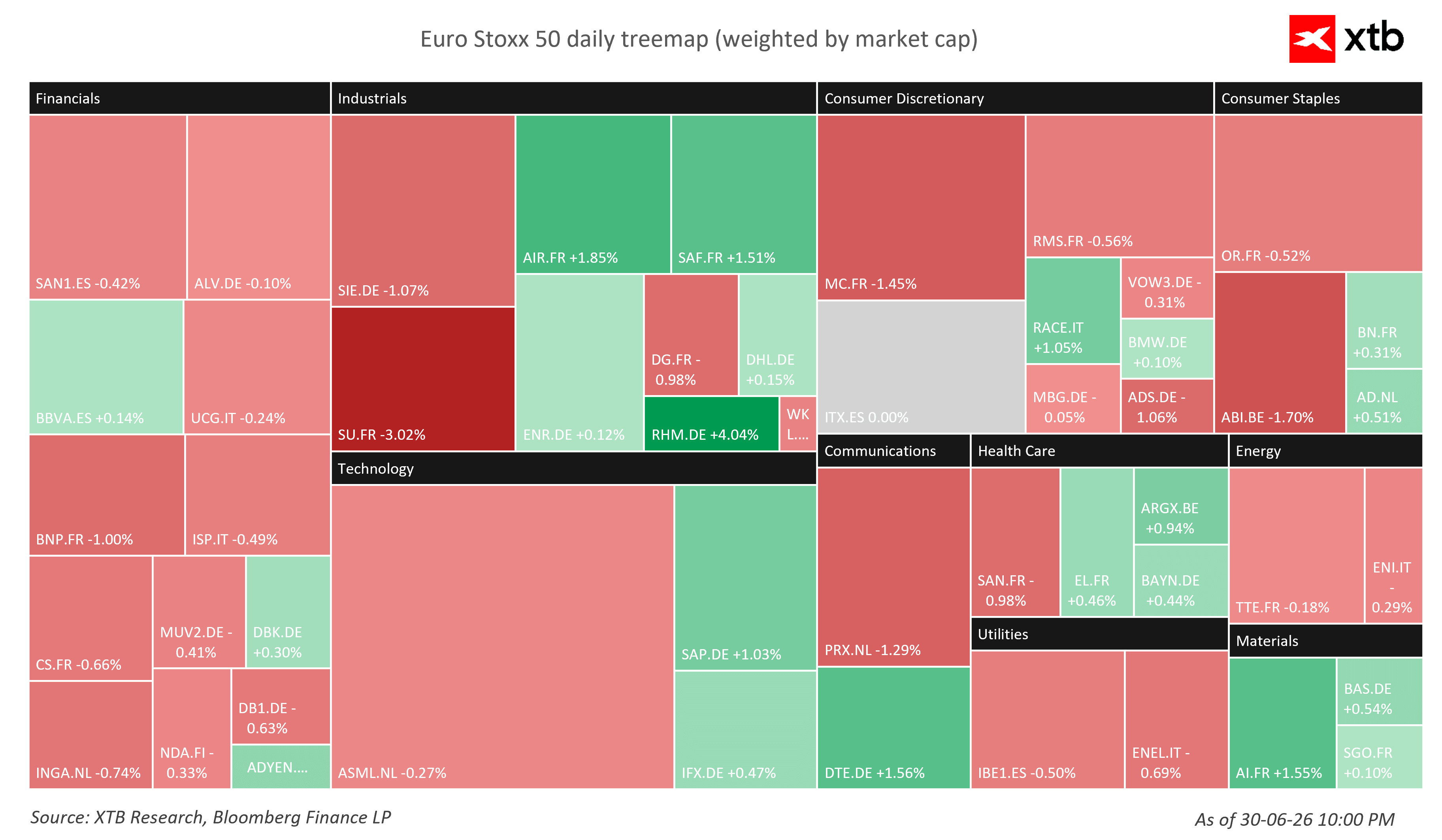

Defense stocks outperform while luxury goods lag

Today's strongest performers within the STOXX Europe 600 include Rheinmetall, Airbus, and Deutsche Telekom, reflecting continued investor interest in defense and selected defensive sectors.

On the downside, Schneider Electric, Anheuser-Busch InBev, and LVMH are among the session's weakest performers, highlighting continued sector rotation across European equities.

Source: XTB Research

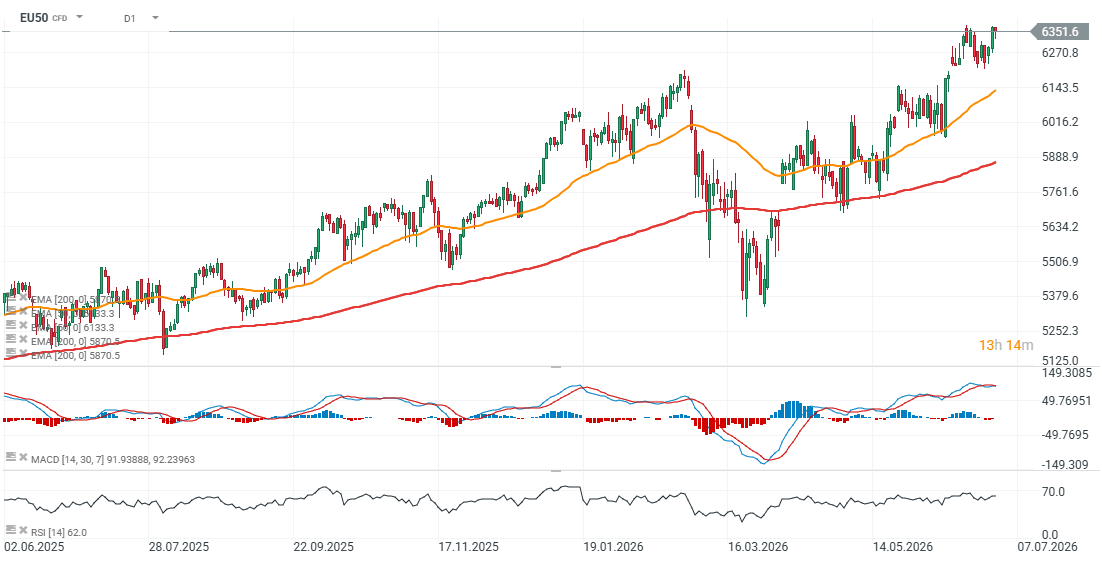

DE40 and EU50 technical outlook

Since June 2025, the Euro Stoxx 50 futures contract has experienced four meaningful pullbacks, recovering each decline relatively quickly. The long-term uptrend remains intact, with the 200-day exponential moving average (EMA200) currently located near 5,900 points. A move back to this level would imply roughly an 8% correction from current prices.

The index is once again testing the record-high area around 6,350 points. A decisive breakout above this resistance could open the door to another leg higher and fresh all-time highs.

Source: xStation 5

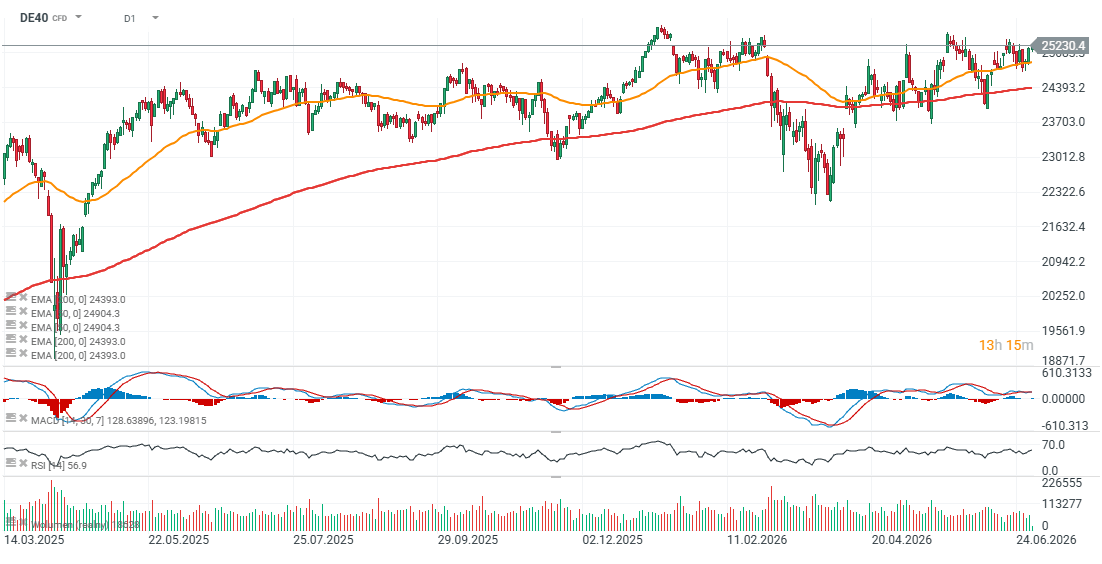

The German DAX futures contract is trading higher today, although the structure of the rally has flattened over recent months. Since spring, the index has fallen below its EMA200 on five separate occasions before successfully recovering each time.

From a technical perspective, maintaining support above the 50-day exponential moving average (EMA50) near 24,400 points remains the key condition for preserving the current bullish trend.

Source: xStation 5

Sector rotation across the Euro Stoxx 50

Recent market action continues to highlight active rotation between sectors and individual stocks within the Euro Stoxx 50. Investors are selectively shifting capital toward industries expected to benefit from higher government spending, resilient earnings, and improving macroeconomic conditions, while taking profits in sectors that have significantly outperformed over the past year.

Source: XTB Research

Source: XTB Research

PMI data point to improving manufacturing, but the recovery remains uneven

Wednesday's manufacturing PMI releases suggest that Europe's industrial sector continues to stabilize after a prolonged slowdown, although the recovery remains far from uniform.

Spain disappointed, with its Manufacturing PMI falling to 49.7, below both expectations and the key 50-point expansion threshold. Switzerland also missed forecasts, although its reading of 54.3 continues to signal solid manufacturing growth.

France delivered a positive surprise, with Manufacturing PMI rising to 51.2, while Germany's final reading came in at 50.3, remaining marginally in expansion territory. The Eurozone Manufacturing PMI was confirmed at 51.4, slightly above market expectations.

Overall, the data indicate that European manufacturing is gradually improving, but momentum remains fragile. While stabilization should support cyclical companies, the pace of recovery is still insufficient to suggest a strong acceleration in corporate earnings.

Inflation is today's key macro catalyst

The main event of the day will be the release of the Eurozone's preliminary CPI inflation report for June.

Economists expect headline inflation to slow from 3.2% to 3.0% year-over-year.

A softer reading would reinforce expectations that inflationary pressures are gradually easing after this year's energy shock, potentially giving the European Central Bank more flexibility to ease monetary policy later this year.

Conversely, a stronger-than-expected inflation print could push government bond yields higher and reduce expectations for future ECB rate cuts, weighing on equity valuations.

Sintra forum could set the tone for global markets

The second major catalyst will be the annual ECB Forum on Central Banking in Sintra.

Investors will closely monitor comments from:

- Kevin Warsh, Chair of the Federal Reserve

- Christine Lagarde, President of the European Central Bank

- Andrew Bailey, Governor of the Bank of England

- Tiff Macklem, Governor of the Bank of Canada

The spotlight is firmly on Kevin Warsh, who is making his first major international appearance since becoming Fed Chair. Although many initially expected him to pursue a more dovish policy stance, his recent comments have been noticeably more hawkish, emphasizing the risk that structural inflation may remain persistent.

Any indication that major central banks intend to keep monetary policy restrictive for longer could influence both bond yields and equity markets worldwide.

Geopolitical risks remain in focus

Although crude oil prices have largely erased the gains triggered by the recent Middle East conflict and shipping through the Strait of Hormuz has largely normalized, geopolitical risks remain on investors' radar.

Reports suggested that U.S. President Donald Trump recently considered renewed military action against Iran before ultimately deciding to continue diplomatic efforts. Upcoming talks between U.S. and Iranian officials in Doha mean geopolitical uncertainty remains elevated.

For Europe, this is particularly important. The eurozone economy is considerably more sensitive to higher energy prices than the U.S. economy, meaning another spike in oil prices could quickly feed into inflation expectations and complicate the ECB's policy outlook.

What investors are watching

Following a series of record highs, European equities have entered a wait-and-see phase.

If today's inflation report comes in below expectations and central bankers strike a balanced tone, European stocks could extend their recent rally.

However, a hotter-than-expected inflation reading or more hawkish messaging from Sintra could encourage investors to lock in profits after the strong gains recorded in recent weeks.

For now, markets remain relatively calm, but the combination of key inflation data, central bank communication, and geopolitical developments could significantly increase volatility later in the session.

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

Berkshire earnings: What do the reports say about the market’s direction?

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Intel Needs $15 Billion. Is It a Financial Problem or the Price of an Ambitious Expansion?