📈 Markets & Companies

-

Futures on European indices are recovering from early trading losses, following the report sparking optimisms around a potential second round of US-Iran talks in Pakistan.

-

This development has led to Brent crude's first price drop in five sessions, falling below $105 a barrel as traders monitor energy supply risks in the Strait of Hormuz.

-

The broad EU50 adds 0,75%, semiconductor-heavy NED25 leads gains (+1,4%), German DAX futures (DE40) are up 0,5%, while France’s CAC 40 is slightly behind (FRA40: +0,15%), evening out yesterday’s outperformance.

-

Kemira: Shares fell as much as 9.8% after 1Q results missed expectations. Revenue dropped 4.4% to €677.3 million. CEO Antti Salminen cited geopolitical tensions and the war in Iran as factors impacting demand. The company is implementing price increases to combat rising costs and return profitability to its target range.

-

Spie: The company reported 1Q revenue of €2.45 billion, a 1.5% year-over-year increase. Performance in France and Germany exceeded consensus estimates. Spie maintains its 2026 forecast for strong organic growth and Ebita margin expansion. The proposed dividend payout ratio remains approximately 40% of adjusted net income. The French company is a top 3 gainer in the Stoxx 600 index today (+7,9%).

-

Eni: Eni boosted its share buyback target by 90% to €2.8 billion following increased cash-flow expectations. Annual operating cash-flow guidance rose to €13.8 billion as the Iran war pushed Brent crude above $100. Despite missing 1Q adjusted net income estimates, the company raised its full-year gas and LNG earnings forecast. Stock trades flat.

-

SAP: Shares surged 6% after 1Q cloud revenue of €5.96 billion beat analyst estimates. The company maintained its annual cloud revenue forecast. CEO Christian Klein is shifting the business model toward AI-consumption pricing. Analysts noted the results help ease concerns regarding AI disruption and Middle East conflict impacts.

-

The Dollar Index reversed gains from yesterday’s spike of safe haven demand (USDIDX: -0.2%), with kiwi dollar (NZDUSD: +0.35%) and euro (EURUSD: +0.25%) leading the rebound against the greenback amid improved risk sentiment.

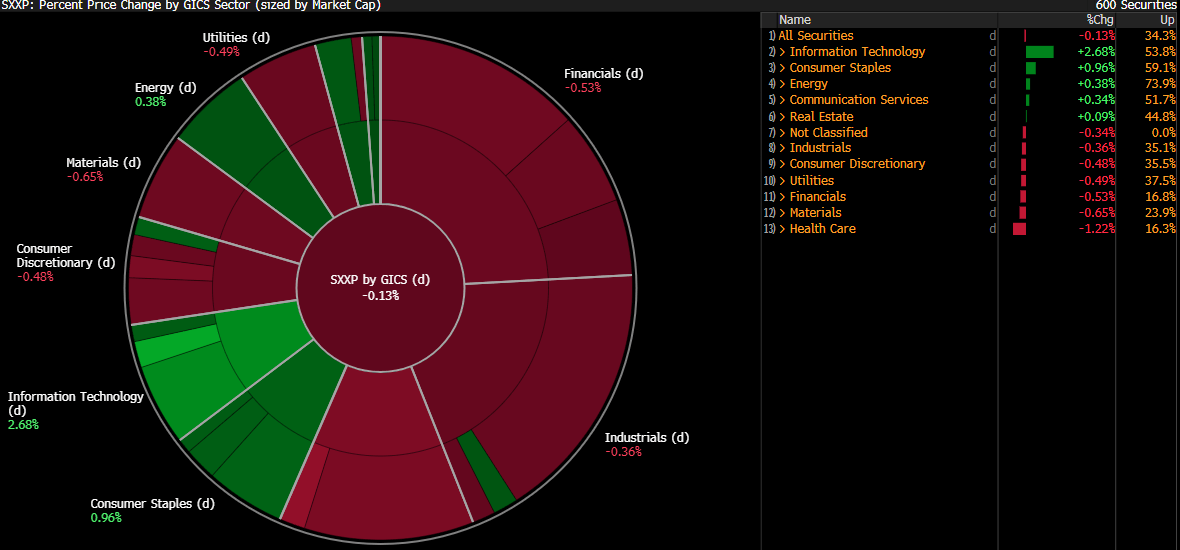

Performance of Stoxx 600 sectors today. Source: Bloomberg Finance LP

🌍 Economics & Politics

-

Optimism is rising as the U.S. and Iran move toward a second round of talks following a period of deadlock, with Iran's foreign minister expected in Islamabad on Friday to potentially ease tensions from the ongoing war.

-

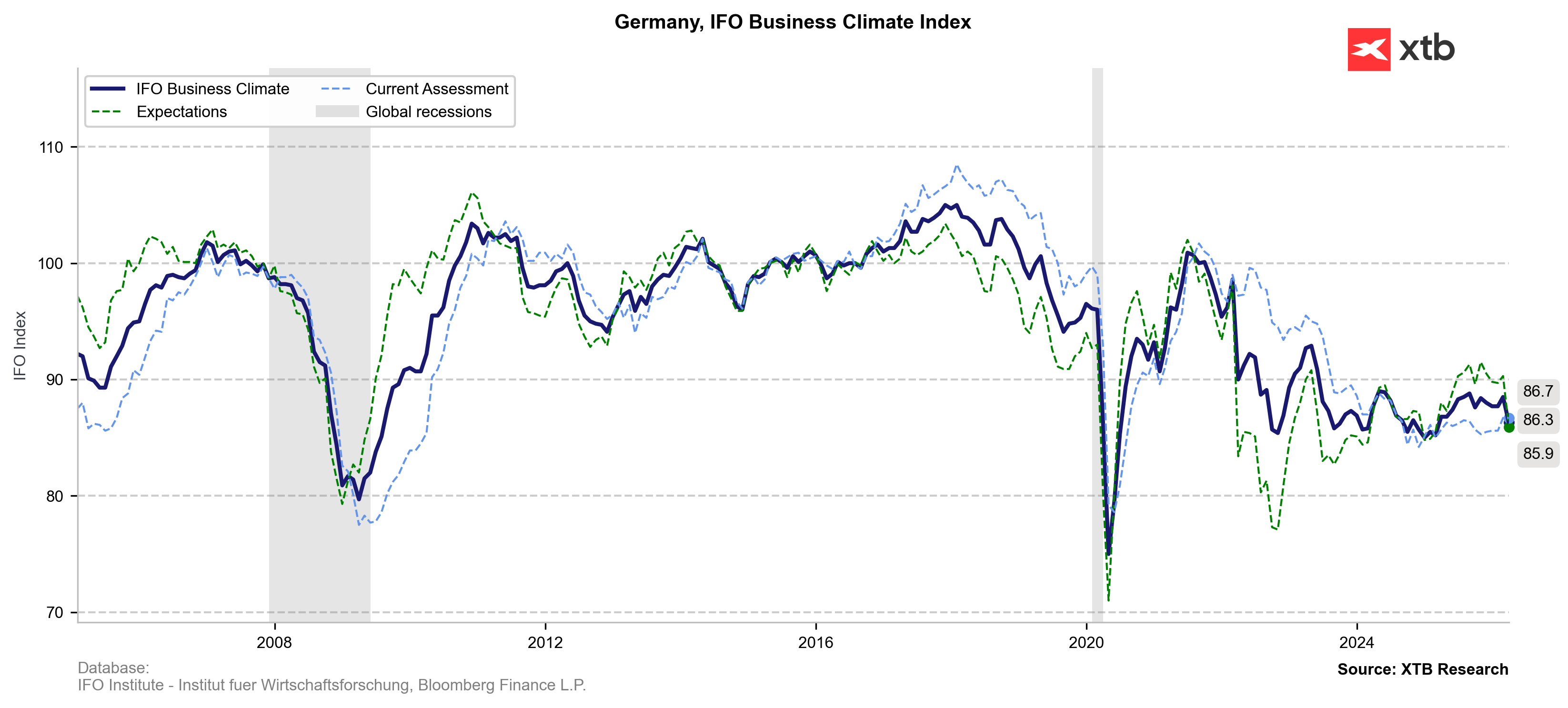

The German Ifo business climate index dropped to 84.4 in April from 86.3 in March, missing consensus estimates and reaching its lowest level since May 2020. Sentiment worsened across all major sectors—particularly in services, trade, and construction—as the expectations index fell to 83.3, reflecting increased pessimism regarding the near-term outlook. This decline, driven by the energy shock from the war in Iran, signals a heightened risk of economic contraction for Germany in the second quarter of 2026.

-

Top US General Caine stated that the US will continue to conduct interdictions in the Pacific and Indian oceans against Iranian vessels, admitting that Iran attacked five merchant vessels.

-

US Secretary of War Pete Hegseth said that Iran has “a chance to make a good deal”, although the naval blockade of Iran will remain in place as long as needed. Additionally, Hegseth accused Europe and Asia of free-riding on US protection, pressuring regions to play their part in the conflict, as “Europe needs the Strait of Hormuz more than us [the US]”.

-

ECB official Peter Kazimir suggested a slight interest-rate hike may be needed as the Iran war drives energy prices higher. With inflation expected to reach 3% , Kazimir noted discussions have shifted from potential cuts to possible increases ahead of the April 30 meeting.

Source: XTB Research

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains