Markets and macroeconomics

-

European indices are rising on Tuesday – the German DAX is up by around 1.3%, the French CAC 40 by 0.9%, the FTSE 100 by around 0.7%, and the pan-European Stoxx 600 is up by nearly 0.8–0.9%. The main catalyst for the gains is President Donald Trump’s decision to call off the planned strike on Iran following requests from allies in the Persian Gulf – Saudi Arabia, Qatar and the UAE – who urged that diplomacy be given more time.

-

Trump announced that there is a “very good chance” of a nuclear deal with Iran, which has clearly eased geopolitical tensions in the Middle East. Crude oil fell by around 2%, although Brent remains above $100 a barrel – contracts for July delivery are trading at around $109.8. The dollar has returned to an upward trajectory following Monday’s rebound – the Bloomberg Dollar Spot Index is up 0.3%, and the USDIDX is hovering around 99.13–99.14, reflecting fragile market sentiment.

-

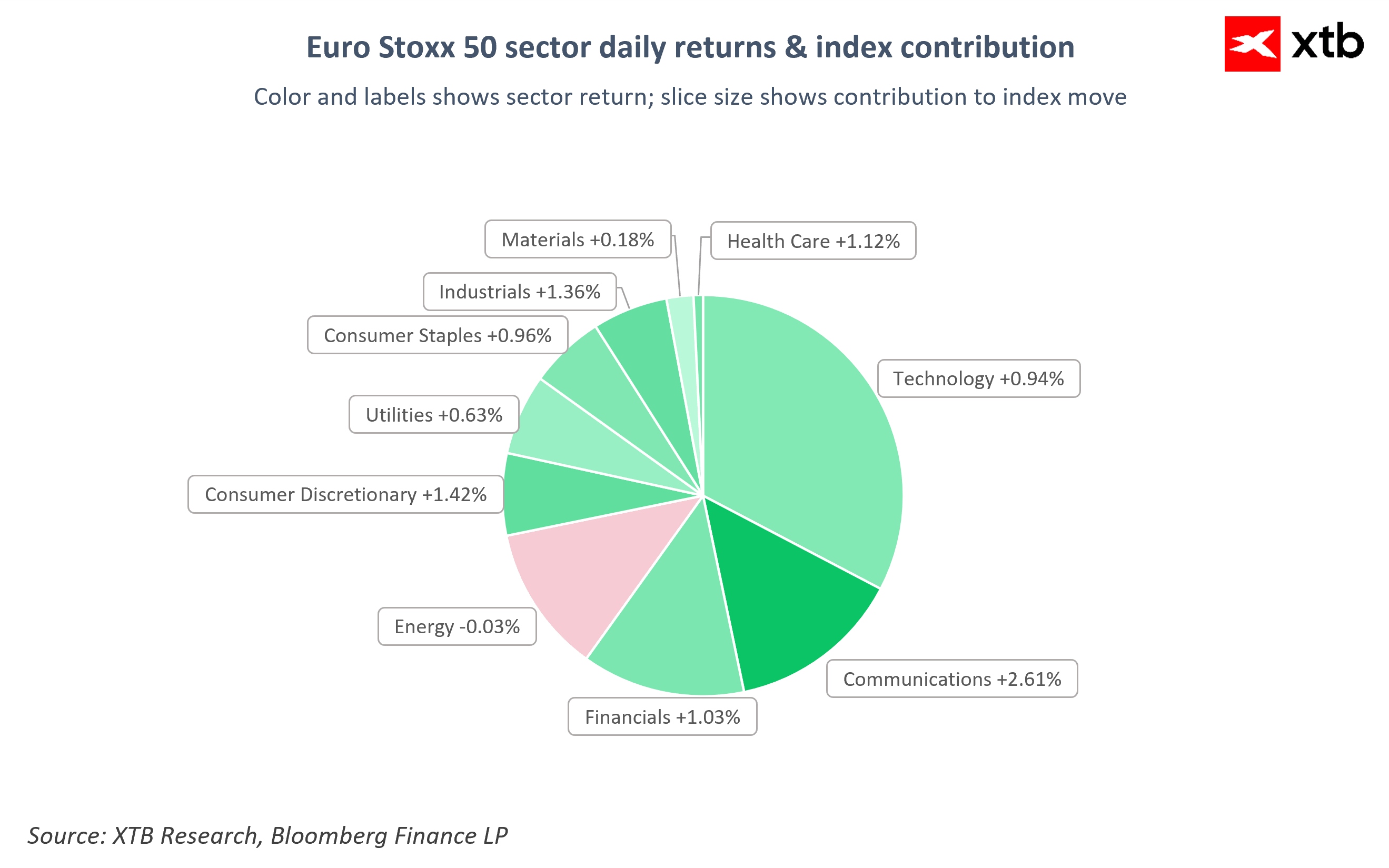

Among the Euro Stoxx 50 sectors, the leaders are: Transport (+2.61%), Consumer Discretionary (+1.42%), Industrials (+1.36%) and Health Care (+1.12%). The Energy sector is the only one in negative territory (-0.03%), dragged down by weakness in TotalEnergies and Eni, whilst Materials are recording only a symbolic rise (+0.18%).

Index and sector chart – What drives the market?

The Communications sector (+2.61%), along with Consumer Discretionary (+1.42%) and Industrials (+1.36%), are driving the gains in the Euro Stoxx 50 today, whilst Energy is the only sector to post a slight loss (-0.03%). Source: XTB

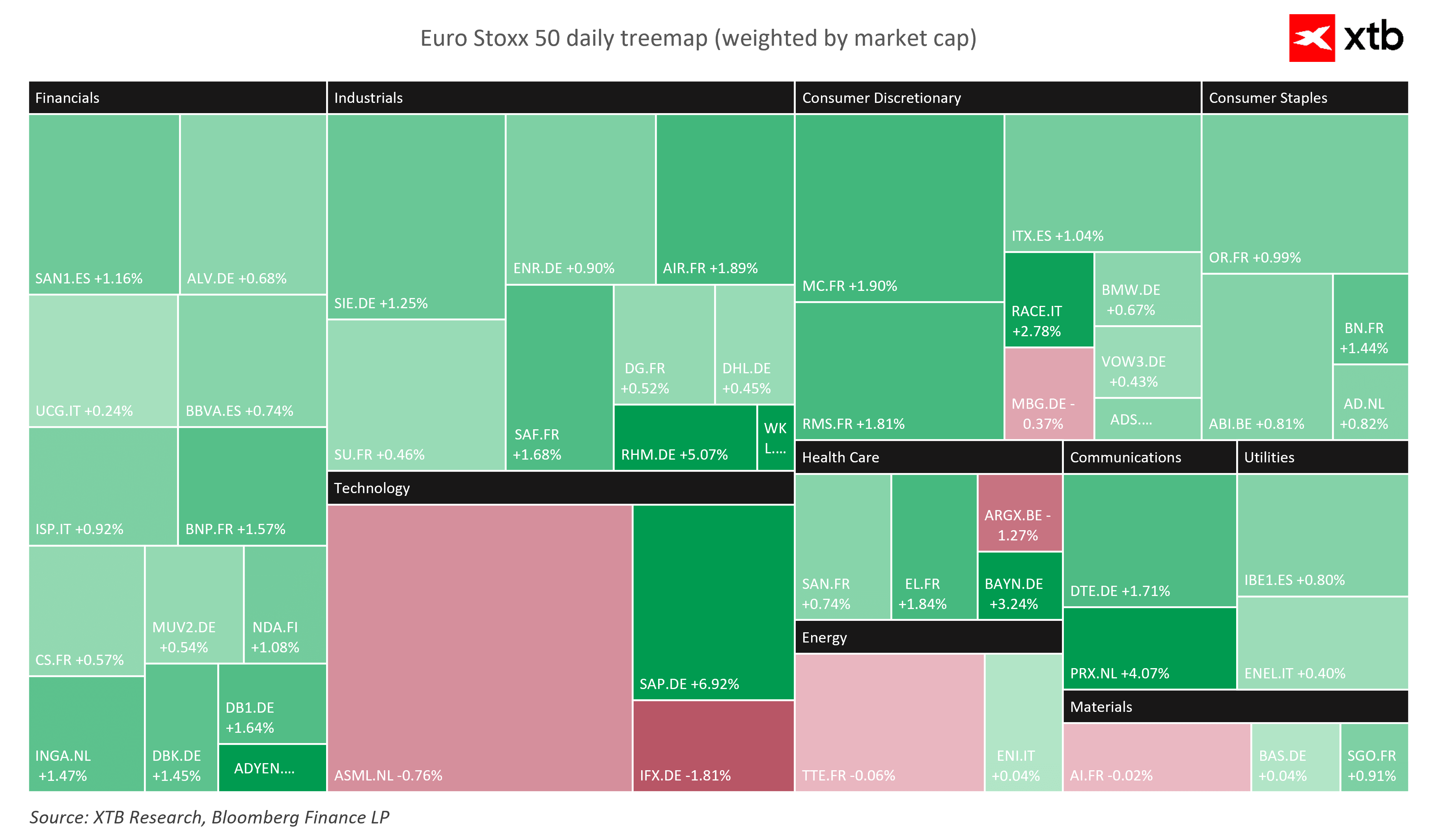

The technology sector (SAP +6.92%, Rheinmetall +5.07%) and consumer and industrial goods are leading the gains on the Euro Stoxx 50, whilst Infineon (-1.81%) and ASML (-0.76%) remain among the few stocks in the red. Source: XTB

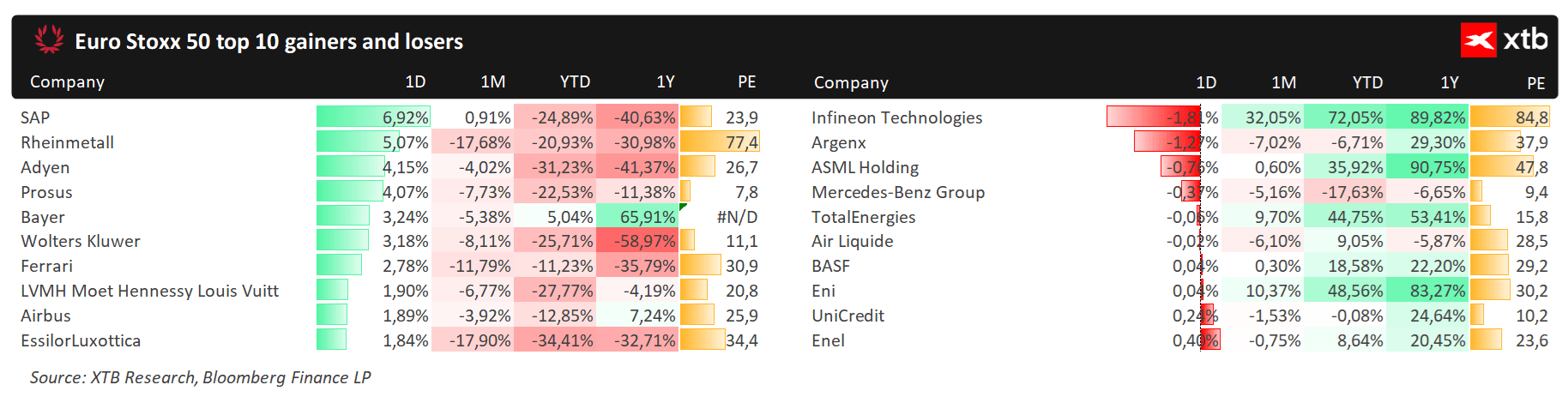

Today’s winners and losers on the European market; companies included in the EuroStoxx 50 and EU50 indices. Source: XTB

Companies

-

SAP is the day’s biggest gainer on the Euro Stoxx 50, jumping by nearly +6.9% – the company is clearly benefiting from the wave of optimism surrounding the technology sector and the return of risk appetite; year-to-date, the company is still down by nearly 25%.

-

Rheinmetall is up by over 5%, and the defence sector (+2.5%) is one of the top performers in Europe – Sweden’s Saab rose by around 4–5% following confirmation that Sweden will purchase naval frigates from France for over $4 billion, with Saab set to develop radar and weapon systems.

-

Evolution Gaming has jumped by over 11% following the announcement of a €2 billion (approx. $2.4 billion) share buyback programme, one of the largest such operations in the company’s history.

-

Vallourec is down nearly 7.8% after ArcelorMittal sold its 10% stake in the French steel tube manufacturer at a discount, generating proceeds of around €667 million.

-

Uniper is up by around 1.9–9.3% following the German government’s announcement of its intention to privatise the energy group – the government holds 99.12% of the company’s shares and plans to sell them or float the company on the stock market, which could be one of the biggest European deals of the year.

-

Infineon Technologies (-1.81%) and ASML (-0.76%) are weighing on the technology sector, even though SAP is rebounding strongly – investors are taking a selective approach to chipmakers amid uncertainty surrounding global trade and Nvidia’s upcoming results.

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season