- The first reports from Beijing are focusing on issues relating to Taiwan.

- European markets are in the green, Korean KOSPI is also continuing to rise.

- The dollar remains strong, with limited volatility in the currency market.

- Political problems in Brazil are dragging down the real and the Ibovespa.

- US inflation data has come in higher than expected, but the markets remain calm.

- The first reports from Beijing are focusing on issues relating to Taiwan.

- European markets are in the green, Korean KOSPI is also continuing to rise.

- The dollar remains strong, with limited volatility in the currency market.

- Political problems in Brazil are dragging down the real and the Ibovespa.

- US inflation data has come in higher than expected, but the markets remain calm.

The first few hours of talks between Donald Trump and Xi Jinping are rather uneventful. The market remains optimistic, awaiting headlines that might shed light on the future of Sino-American relations. For now, attention is focused on Taiwan. The Chinese leader has warned that if talks on this issue are "mishandled," relations with the United States could deteriorate significantly. Supporting Taiwan's independence is considered a red line for Xi.

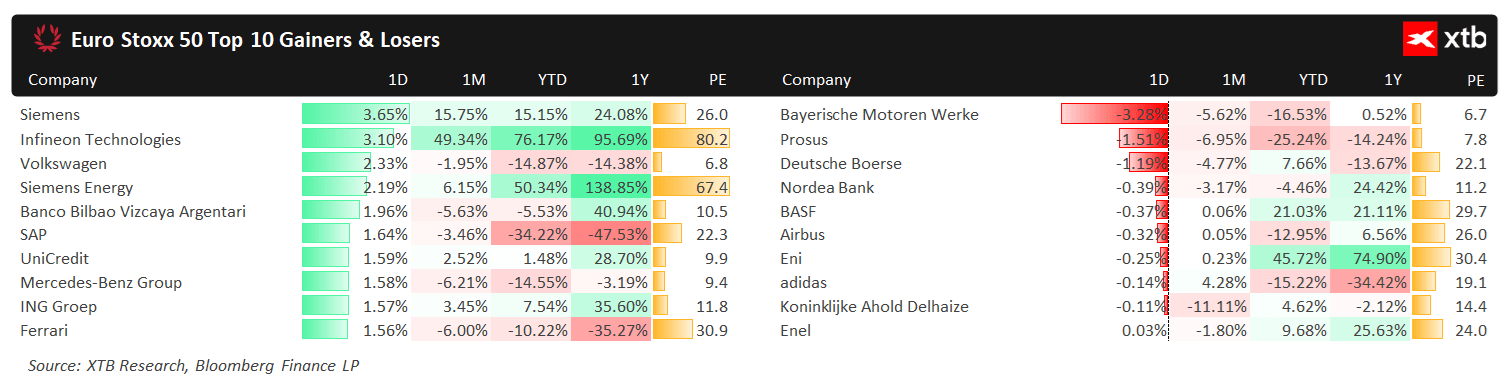

Key European stock indices are posting significant gains. The German DAX leads the pack (1.2%), supported by the resurgent Siemens (3.2%). The industrial giant continued its growth despite slightly weaker-than-expected results for the last quarter, reaching over 15% month-on-month.

Chart 1: Winners and losers in the Euro Stoxx 50 (14/05/2026)

Source: XTB Research, 14/05/2026

Source: XTB Research, 14/05/2026

Movements on Asian markets are less clear. The Shanghai Stock Exchange (-1.5%) and the Japanese NIKKEI 225 (-1%) are both down. Meanwhile, the Korean KOSPI (1.8%) continues to strengthen – the index has already gained nearly 90% since the beginning of the year. The tech giant, Samsung, continues to perform well (4.2%, 95% YTD), with LG near the top of the local dashboard for the day (8.3%).

Volatility in the currency market remains significantly limited. Higher-than-expected inflation data supports the dollar, pushing the EUR/USD pair down to 1.17. Sentiment, however, remains moderately positive, currencies most burdened by the prospect of a prolonged energy crisis – the South African rand, the Thai baht, and the South Korean won – also seeing gains.

At the bottom of the global dashboard, we find the Brazilian real, which is suffering from reports linking Flavio Bolsonaro – son of Jair Bolsonaro, the country's former president – to the scandal surrounding Banco Master SA. The news weakens Flavio's position for the presidency in the October elections, in which he will face the incumbent left-wing leader, Lula – a move not viewed favorably by the markets. The Brazilian stock market is also seeing significant declines. The Ibovespa has weakened by over 10% over the past month.

Macroeconomic data

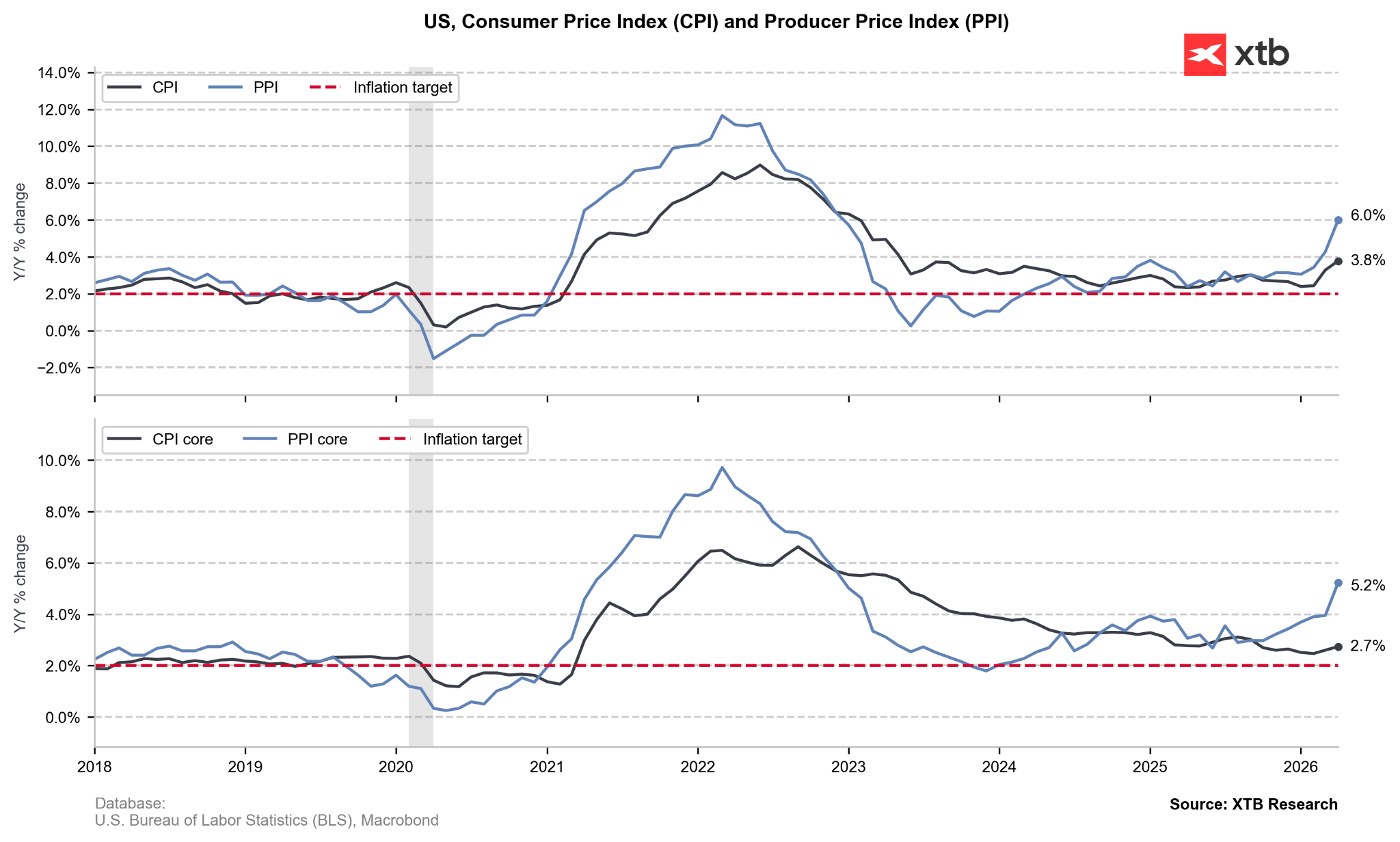

Yesterday, attention once again focused on US inflation data – this time, however, on producer inflation. All of the measures – headline, core, and the so-called "super-core" (which also excludes trade-related services) – not only rose but also performed significantly above expectations. The increase in core price pressures, which could spill over into producer inflation in the coming months, is particularly concerning.

Chart 2: US CPI and PPI inflation (2018 - 2026)

Source: XTB Research, 14/05/2026

Source: XTB Research, 14/05/2026

- PPI inflation [YoY]: 6.0% (vs. 4.8% consensus)

- PPI inflation [MoM]: 1.4% (vs. 0.5%)

- Core PPI inflation* [YoY]: 5.2% (vs. 4.3%)

- Core PPI inflation* [MoM]: 1.0% (vs. 0.3%)

- Super-Core PPI inflation** [YoY]: 5.2% (vs. 4.3%)

- Super-Core PPI inflation** [MoM]: 1.0% (vs. 0.3%)

*Excludes food and energy.

** Excludes food, energy and trade-related services.

The market's reaction was surprisingly muted. While we did note an increase in the implied probability of a US interest rate hike before the end of the year, not only was this move very modest, but it also partially reversed this morning. Markets assign a roughly 35% chance of this happening. The rise in US Treasury yields proved equally unsustainable, with 10-year bonds returning to around 4.46%.

Data on GDP growth of Poland, one of Europe’s leaders in this regard, has also been released. On a quarterly basis, the figures were the worst since Q3 2024 (0.5% QoQ), which may be partially due to poor weather conditions in the first months of the year. It's difficult to directly attribute the slowdown to the disruptions in the energy sector – this should be more noticeable in Q2. The outlook for the Polish economy in 2026 remains good, however. Despite modest downward forecast revisions, the consensus still assumes annual growth of 3.5%.

---

Michał Jóźwiak, Financial Markets Analyst at XTB

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

BREAKING: BoE Keeps Rates Unchanged

🛢️Further escalation and tense situation do not drive oil further

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound