- Markets in the APAC region traded in a slightly weaker mood. Chinese indices recorded sizable declines, which negated part of the rebound seen recently. The Hang Seng is currently losing 2.02%. Markets in Korea and Japan are posting slight gains.

- The U.S. Treasury Department expects to take on $760 billion in net market debt in the January-March period, down $55 billion from the October 2023 estimate. The news triggered a drop in US 10-year yields during yesterday's session.

- European futures point to a higher opening in the European cash session.

- Highlights for the day include: regional eurozone inflation data, a GDP report from the eurozone, and JOLTS data. The calendar will be topped off with quarterly reports from UPS, Pfizer, Marathon Petroleum, Microsoft, Alphabet, Starbucks and AMD.

- BBVA's 4Q23 results:

- - Q4 Net interest income: EUR 5.25 billion (est EUR 5.89 billion)

- - Q4 net income: EUR 2.06 billion (est EUR 1.95 billion)

- - FY Net income: EUR 8.02 billion (est EUR 4.9 billion)

- - Bad loan ratio: 3.4% at end-December

- Saudi Arabia orders oil giant Aramco not to increase production capacity.

- ECB representatives, including Lane and Nagel, will speak on Tuesday.

- Wages in China are falling fast. Average wages in Q4 in 38 major cities fell 1.3% y/y.

- Retail sales in Australia in December -2.7% m/m (-0.9% expected).

- Prices in British stores rose this month at the slowest annual pace since May 2022, the British Retail Consortium reported Tuesday. On Thursday, investors will learn the BoE's latest interest rate decision.

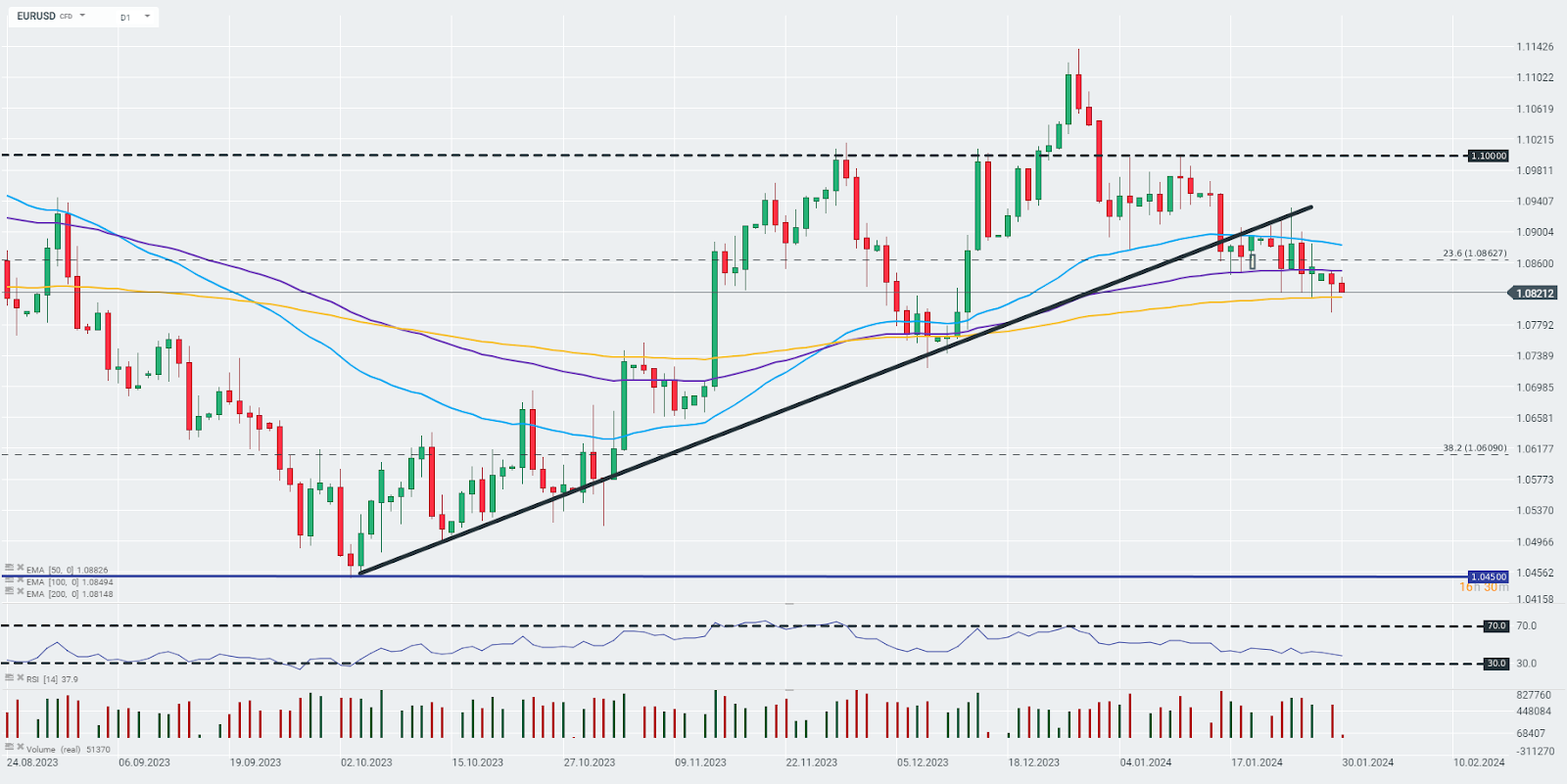

- In the currency market, the New Zealand dollar and the Canadian dollar are currently performing best. The euro and the pound are currently trading under heavy downward pressure. The EURUSD pair is holding slightly above the zone of the 200-day exponential moving average.

- Cryptocurrencies continue to rise, with Bitcoin clearly breaking out above the $43,000 barrier.

The EURUSD pair is trading in the zone of key supports. Source: xStation

NFP much below expectations! 🚨EURUSD spikes 📈

Dollar and Nasdaq facing a key test

Chart of the Day: What will drive the US stock market? (07.08.2026)

Economic Calendar: Will NFP Move the Market? (07.08.2026)