Technology company Snap Inc. yesterday issued a troubling statement, part of which was sent to the U.S. Securities and Exchange Commission. The company lowered its quarterly growth forecasts and pointed to the deteriorating macroeconomic environment. Will Snapchat's statement lead to another cascading sell-off and deterioration in sentiment among technology companies similar to what happened previously with Netflix?

-

The 20-25% revenue growth forecast published by Snapchat in April will have to be lowered and revised again;

-

The company announced that it is not meeting its revenue growth targets for the quarter. CEO Evan Spiegel intends to control spending at the company, and will hire only 500 new employees by the end of 2022, a significantly lower figure compared to 2,000 workers hired in 2021. The plan outlined looks similar to those previously published by Meta Platforms and Twitter, which are also cutting costs this year;

"We believe it is likely that revenue and adjusted EBITDA will be below the low end of our guidance for Q2 2022" said CEO Evan Spiegel "The first quarter of 2022 proved more difficult than we expected" and "While our revenue continues to grow year-over-year, it is growing more slowly than we expected at this time" he also noted.

-

According to Spiegel, the company is currently struggling with uncharacteristic problems: rampant inflation and rising interest rates causing clients to cut back on purchases and lower demand for installment products. Also privacy protection introduced among others by Apple on iPhones also affect Snap operations, while the war in Ukraine reduced number of clients;

-

Rising inflation and interest rates coupled with supply chains disruptions have taken their toll on the tech sector as a whole, which recently has scored one of the biggest sell-offs in history;

-

Snapchat was trading at a very high price-to-earnings ratio (PE Ratio 49.4 vs 37.7 for the tech industry) and price-to-book value (PB Ratio 10.6) compared to the sector average. The company is one of the so-called growth companies for which surging revenues were an excuse for very high valuations. In the context of a more complicated macroeconomic situation and changes in monetary policy, growth companies are literally running out of steam. That is why the prospect of limited ability to generate revenues looks particularly alarming. Despite booming revenues, Snapchat is still not a profitable company, and its high premium listing means that the potential for further declines still exists;

-

Snapchat's price to book value ratio (10.6) is still significantly higher compared to other technology companies Meta Platforms (4.67) or Netflix (4.72)

-

The news reported by Snapchat has already spilled over into the market and pushed pressure on other tech stocks. In the pre-market, shares of Meta Platforms, Twitter and Google are falling;

-

If Snapchat launches today’s session near the $15 level, it will mark a near 80% drop from all-time high. This is a massive sell-off which lasted only 7 months. However, the company still has a base of more than 330 million users worldwide who are eager to use its services. Some aggressive long-term investors may look for opportunities in recently losing growth companies like Netflix and Snapchat. At the same time, Spiegel conveyed that: "We remain excited about the long-term growth opportunities for our business (...) Our community continues to grow and we continue to see strong engagement across Snapchat, and we continue to see significant opportunities to grow our average revenue per user over the long term."

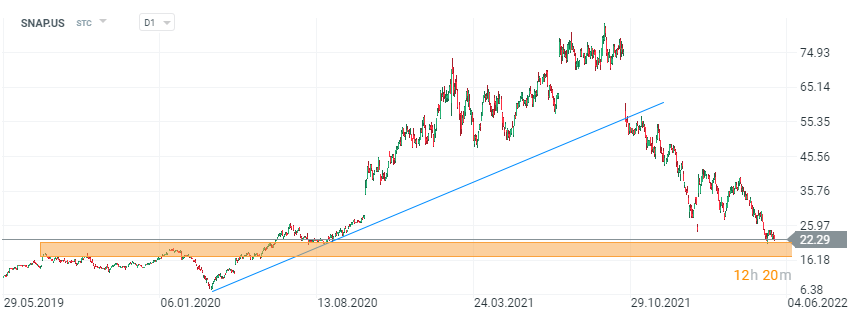

Snap (SNAP.US), D1 interval. Stock has been moving in a very dynamic uptrend since the beginning of the pandemic. Price skyrocketed nearly 1500% from March 2020 lows as people spent more time on the app and stayed home. However, prices plunged in the second part of 2021 after weak quarterly results. Since then, the stock has been moving in a dynamic downtrend. If buyers manage to defend support around $15 then upward correction may be launched towards the $20 area. On the other hand,if current sentiment prevails sell-off may accelerate towards the psychological support at $10. Source: xStation5

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

SoftBank earnings: Intel and AI are not enough?

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure