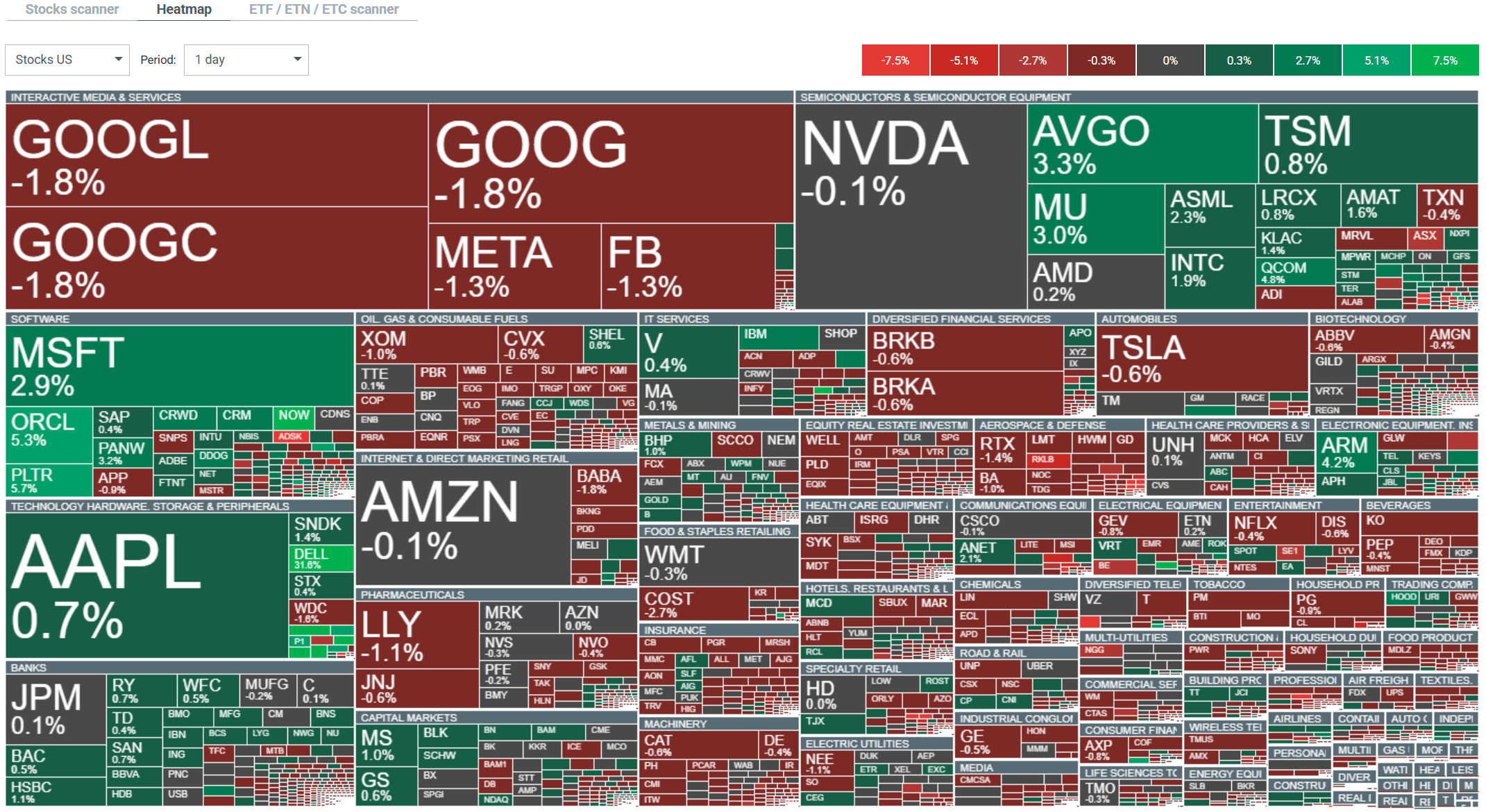

S&P 500 and Nasdaq 100 futures are up 0.1%, while the Dow Jones is gaining 0.2% ahead of the final trading session of May—a month that has proven to be exceptionally strong for the stock markets. The AI narrative remains the main driver: Dell’s after-hours results literally sent the market soaring and pushed the entire computer industry sharply higher.

Dell reported a nearly ninefold year-over-year increase in AI revenue and raised its full-year guidance to $165–169 billion with EPS of $17.90—well above analysts’ expectations of $142.5 billion and $13.09 in EPS. It is Dell’s results that are driving market sentiment today; Dell joins the ranks of “tech dinosaurs” that have found a second life as AI players, much like Intel, Cisco, and Nokia before them. It is worth noting, however, that Goldman Sachs estimates that pension funds are poised to sell $14 billion worth of shares as part of their monthly rebalancing—the 12th-largest estimate of its kind since at least 2000.

On the sector front, technology and computer hardware are clearly winning: Dell +35%, HPE +17%, NetApp +19%, SMCI +10%, HP +7%. Today’s losers include space companies following the Blue Origin rocket explosion on the launch pad (ASTS -15%, Rocket Lab -5.5%), the apparel sector (Gap -15%, American Eagle -11%), and some cybersecurity firms (SentinelOne -16%).

Source: XTB

Company Information

-

Dell (DELL) +35% – An absolute earnings sensation: the company raised its full-year revenue guidance to $165–169 billion (compared to the consensus estimate of $142.5 billion), and revenue from AI servers surged nearly 9x year-over-year. Analysts are calling it a "breakout quarter" and comparing Dell to Intel or Cisco—veteran players who are once again becoming key beneficiaries of the AI boom.

-

Gap (GAP) -15% – The apparel giant lowered its full-year sales growth forecast to 1–2% (previously 2–3%), and Q1 revenue came in at $3.50 billion versus the expected $3.52 billion. The main issue is the struggling Old Navy brand, which weighed on the entire report.

-

SentinelOne (S) -16–20% – The cybersecurity company severely disappointed with its Q2 revenue forecast (USD 289–291 million versus the expected USD 292 million) and announced an 8% reduction in full-time headcount – the market reacted with a sharp sell-off.

-

AST SpaceMobile (ASTS) -11–15% – Shares of the space company, a partner of Blue Origin, plummeted after the New Glenn rocket exploded on the launch pad during a ground test on Thursday evening in Florida. EchoStar (-4.5%) and Rocket Lab (-5.5%) also fell in the wake of ASTS.

-

NetApp (NTAP) +15–19% and Okta (OKTA) +7–8% – Both companies surprised the market with better-than-expected results: NetApp posted solid growth in the storage segment and raised its full-year guidance, while Okta—a leader in identity management—raised its full-year revenue guidance and beat consensus on every line item.

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off

Daily Summary: Equities rally on not-so-hawkish Fed and AI trade revival, Yen dominates FX, oil retreats (30.07.2026)

Unexpected FX intervention? USDJPY plummets more than 2%! 🇯🇵