-

"Trump Put" vs. Iran Scepticism: Markets are buoyed by a 15-point US peace plan, though Iran’s rejection and continued clashes keep volatility high.

-

Arm’s Historic Pivot: Arm shares jumped 15% on news it will manufacture its own AGI CPUs, targeting $15B in annual sales with Meta as its first client.

-

Supply Chain Risks: Despite tech gains, Nvidia faces risks as Middle East tensions threaten helium supplies, a gas essential for semiconductor production.

-

"Trump Put" vs. Iran Scepticism: Markets are buoyed by a 15-point US peace plan, though Iran’s rejection and continued clashes keep volatility high.

-

Arm’s Historic Pivot: Arm shares jumped 15% on news it will manufacture its own AGI CPUs, targeting $15B in annual sales with Meta as its first client.

-

Supply Chain Risks: Despite tech gains, Nvidia faces risks as Middle East tensions threaten helium supplies, a gas essential for semiconductor production.

US index futures posted modest gains ahead of the Wall Street opening bell, with indices eventually opening slightly higher, buoyed by hopes of a diplomatic breakthrough in the Middle East. Although Iran has officially rejected the proposed ceasefire, markets appear to be placing their faith in Donald Trump’s effective "message management." However, the true standout of the American morning is the technology sector—specifically Arm Holdings, which has announced a revolutionary shift in its business model.

Between Diplomacy and Escalation

The early afternoon across global markets has been defined by high volatility, triggered by conflicting signals from the Middle East. Following yesterday’s mixed session, the situation in Asia showed significant improvement; the Nikkei 225 surged nearly 3%, the Shanghai Composite rose by 1.3%, and South Korea’s KOSPI climbed 1.6%. In Europe, indices are performing slightly better, with most gains hovering around 1.5%, leaving the majority of benchmarks within striking distance of historical highs.

In the US, S&P 500 (US500) and Nasdaq 100 (US100) futures are both trading approximately 0.15% higher, while the VIX remains at elevated levels. Optimism was largely fueled by a 15-point US peace plan, which includes provisions for sanction relief for Iran in exchange for restoring freedom of navigation in the Strait of Hormuz. Crucially, the plan requires Iran to effectively abandon its nuclear aspirations—a point that was previously partially negotiable, but which Tehran has refused to accept since the outbreak of hostilities. Nevertheless, crude oil prices have retreated by nearly 5% following reports of several vessels successfully transiting the Strait over the past few hours.

Market sentiment was eventually dampened by reports from the Fars news agency, stating that Tehran views the talks as "illogical" and rejects the ceasefire terms. Analysts note the persistence of the so-called "Trump Put"; the market assumes the administration will not allow a permanent collapse, even as facts on the ground point to continued exchanges of fire, with Israel maintaining its strikes on Iran.

Technical Analysis and Fundamentals: S&P 500 faces moderating valuations

The S&P 500 (US500) remains at a critical juncture. The price is holding above key support linked to the 23.6% Fibonacci retracement level near 6,600 points. Currently, the US500 is moving within a descending trend channel; a breakout above the upper boundary could lead to a retest of the 6,800-point zone.

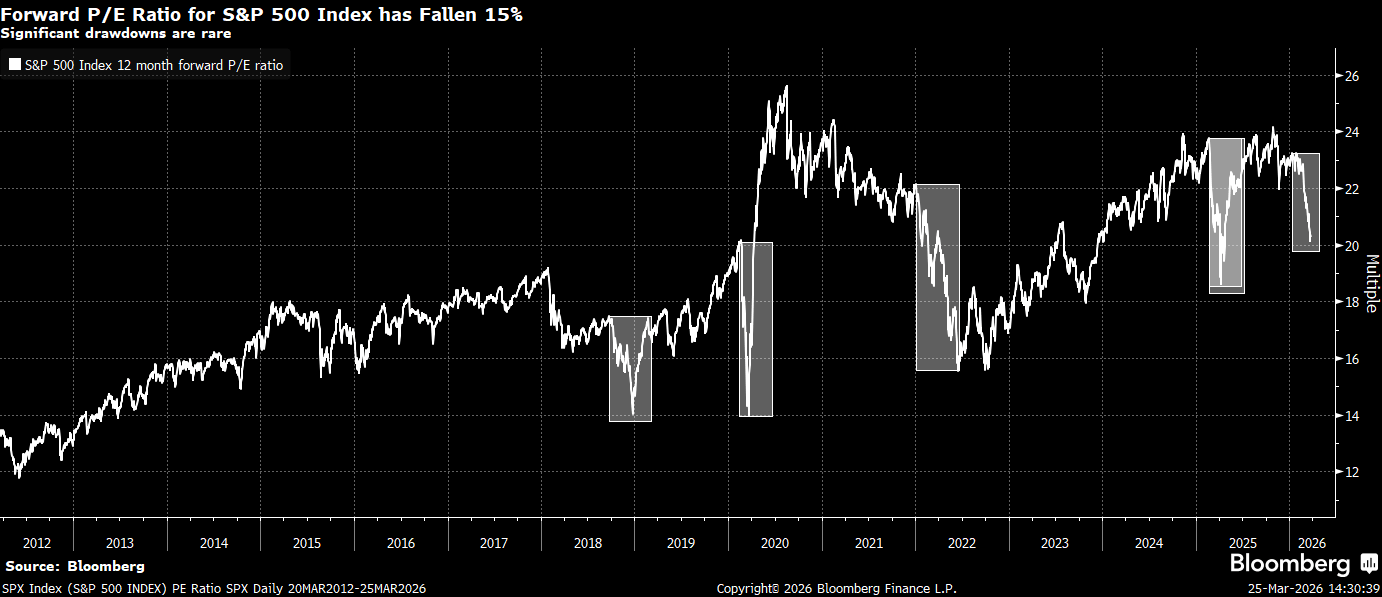

Fundamental valuations also warrant attention. The Forward P/E ratio (price-to-projected earnings) for the S&P 500 is currently oscillating around 21. While this remains above the 10-year average of approximately 18, it is significantly lower than the peaks of 24 seen over the last two years. Although the market is not yet "cheap" (historically the 14-18 range), a definitive resolution to the conflict could provide the necessary tailwinds for S&P 500 equities to gain momentum.

Source: Bloomberg Finance LP

Source: Bloomberg Finance LP

Corporate News: Spotlight on ARM and Chipmakers

The primary mover in today's session is Arm Holdings (ARM), with shares surging over 15%. The company has announced a historic strategic pivot: for the first time, Arm will begin manufacturing and selling its own integrated circuits (the so-called AGI CPUs), moving beyond its traditional model of merely licensing architecture to other manufacturers.

-

Financial Targets: The new business line is expected to generate $15bn in annual revenue within five years. Total company revenue is projected to rise to $25bn over that period, up from approximately $5bn today.

-

Customers: Meta Platforms will be the first major customer for the new 136-core processors, which are to be manufactured by TSMC.

-

Analyst Reaction: Raymond James upgraded ARM to "Outperform" with a $166 price target, describing the move as transformative for the company’s business model.

Within the semiconductor space, attention is also fixed on Nvidia (NVDA) (+2.5%). Despite the gains, supply-side risks loom over the sector. Intensifying conflict in Iran and potential damage to regional gas infrastructure could impact the availability of noble gases such as helium, which is essential for lithography and silicon wafer production. The Middle East, particularly Qatar, is a critical global supplier of helium; reported damage to LNG terminals could lead to long-term increases in chip production costs.

Other Corporate Movers:

-

General Motors (GM): Shares rose just under 2% following an upgrade to "Outperform" by Wolfe Research (PT $96).

-

Tesla (TSLA): Gains 3% amid a general improvement in sentiment toward the broader tech sector.

-

Energy Sector: Fossil fuel companies are retreating alongside WTI crude, which has dipped below $89 per barrel. Exxon Mobil fell 1%, while the natural gas player Cheniere dropped 2.5%.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Texas Instruments earnings: Growth without cash

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.