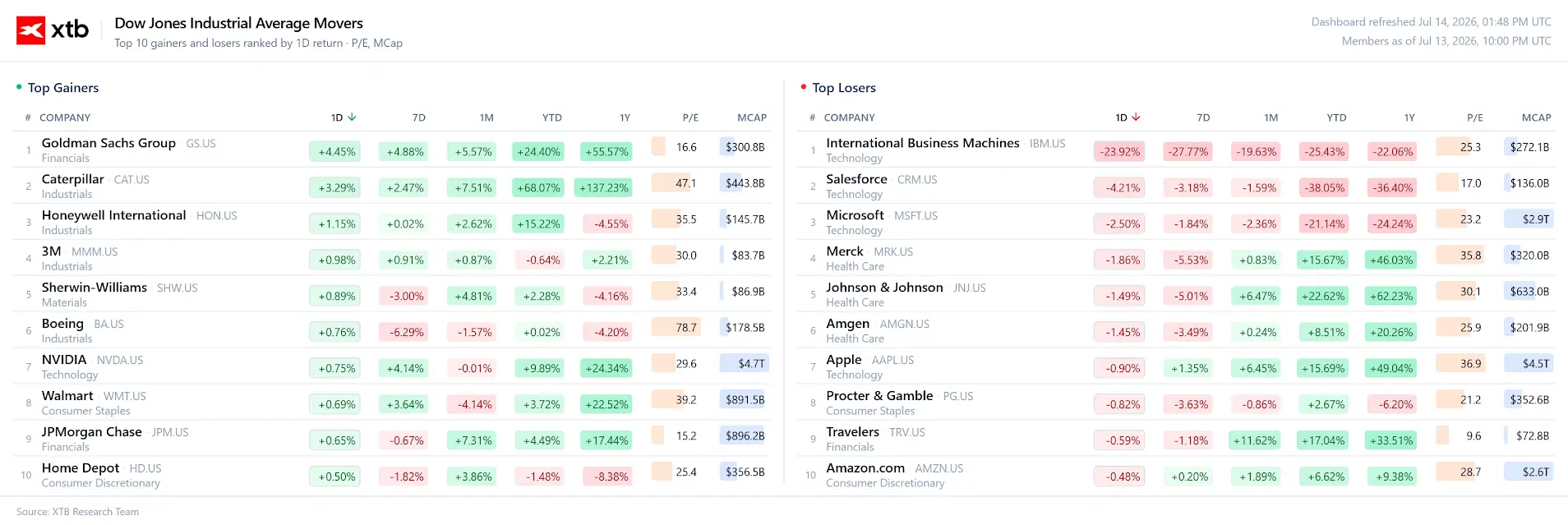

Wall Street's major indices are trading higher after weaker-than-expected U.S. inflation data eased concerns about another near-term Federal Reserve rate hike. The Dow Jones Industrial Average is up 0.2%, supported by strong gains in Goldman Sachs shares but weighed down by a sharp sell-off in IBM. The broader advance remains limited by surging oil prices and heavy losses across software stocks, where IBM has plunged about 25% following a warning of weaker demand for its software and infrastructure businesses, marking its biggest one-day decline since 1987. Investors are now assessing whether softer inflation will be enough to sustain the market rally despite rising geopolitical risks, higher energy prices, and a mixed corporate earnings season.

- June CPI fell 0.4% month-over-month, compared with expectations for a 0.2% decline, while annual inflation slowed to 3.5%, well below the consensus forecast of 3.8%.

- The probability of a July Fed rate hike dropped to 17% from 42% a day earlier, providing a short-term boost to equity sentiment.

- Markets still price in a 63% probability of a September rate hike, suggesting investors are not yet ready to declare an end to the Fed's hawkish stance.

- Treasury yields rebounded from their intraday lows as investor focus shifted from inflation data to rising oil prices and upcoming comments from Fed Chair Kevin Warsh.

- Semiconductor stocks are rebounding strongly, with the VanEck Semiconductor ETF (SMH) up more than 2%, while Applied Materials, Lam Research, Teradyne, and Micron all post solid gains.

- WTI crude has climbed above $80 per barrel and Brent has risen beyond $86, after President Donald Trump announced plans to reinstate a blockade of Iranian shipping through the Strait of Hormuz.

- IBM is down around 24% after warning that second-quarter earnings will miss expectations due to weaker demand across its software and infrastructure businesses.

- The NFIB Small Business Optimism Index rose for a second consecutive month and significantly exceeded forecasts, pointing to improving conditions for the U.S. economy and smaller businesses.

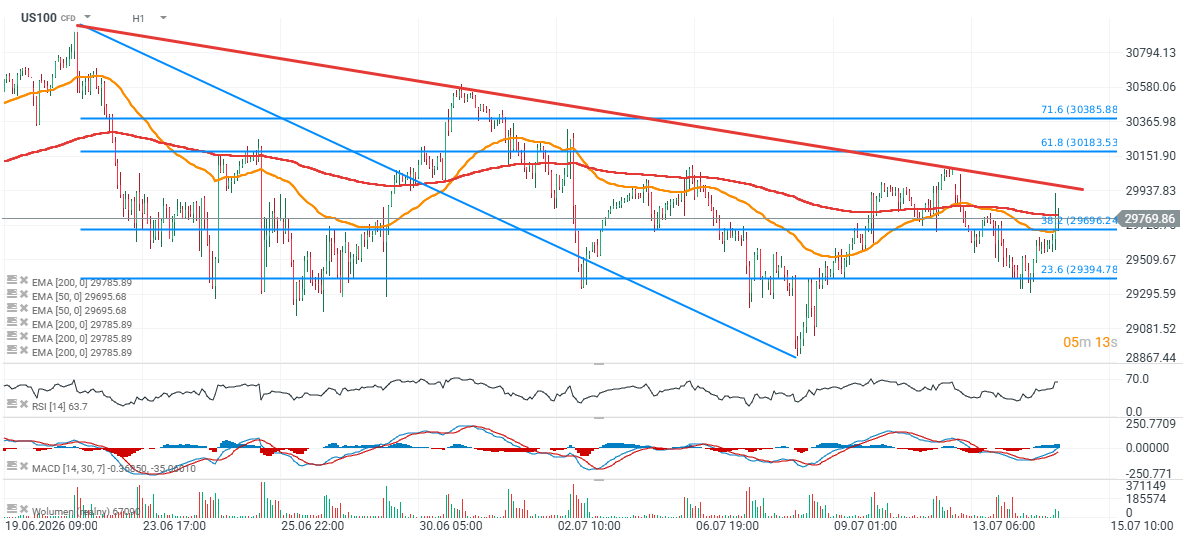

US100 chart (H1 timeframe)

The Nasdaq 100 futures contract is posting modest gains today but has given back most of the rally triggered by the CPI release at 2:30 p.m. The key resistance zone appears to be 29,900-30,000 points, while an important support area is located near 29,400 points, where recent price reactions coincide with the 23.6% Fibonacci retracement of the latest downward impulse.

Source: xStation5

Source: xStation5

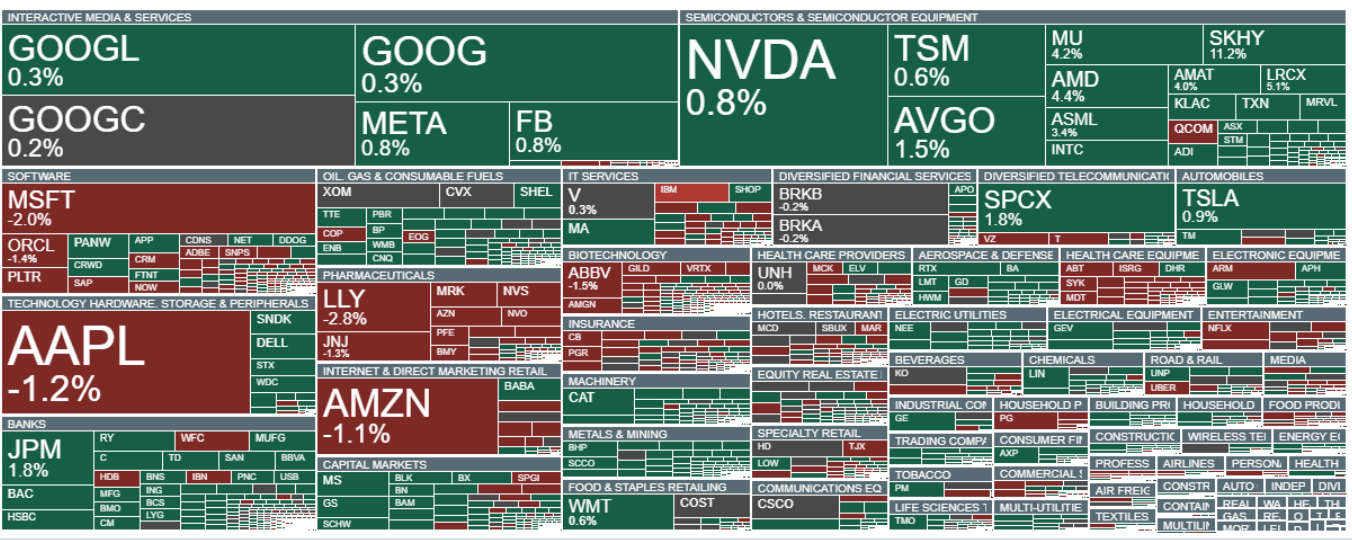

Goldman Sachs, Caterpillar, and Honeywell are among today's strongest performers, while the weakest stocks are concentrated in the software sector, including IBM, Salesforce, Microsoft, and pharmaceutical giant Merck.

Source: XTB Research

IBM (IBM.US)

IBM shares are down nearly 25% after the company released preliminary second-quarter results and lowered its revenue and profitability outlook. If losses hold through the close, it would mark IBM's worst single-day decline since Black Monday on October 19, 1987, when the stock fell 23.7%. It would also represent the largest one-day decline in the company's history based on data going back to 1972. IBM said many enterprise customers are cutting spending on software and IT services while redirecting budgets toward AI infrastructure investments.

JPMorgan Chase (JPM.US)

JPMorgan reported quarterly results that exceeded Wall Street expectations. The bank earned $6.14 per share (excluding one-time items) on $58.02 billion in revenue, compared with analyst estimates of $5.85 EPS and $50.19 billion in revenue. Shares are up nearly 1.5% about 30 minutes after the U.S. market opened.

Goldman Sachs (GS.US)

Goldman Sachs shares are up more than 5% after reporting significantly stronger-than-expected second-quarter results. The bank posted earnings per share of $20.98, well above the $14.48 consensus estimate, while revenue reached $20.34 billion, comfortably beating expectations of $16.13 billion. The results are supporting the broader financial sector and rank among the strongest positive earnings surprises of the current reporting season.

Citigroup (C.US)

Citigroup also delivered better-than-expected quarterly results. The bank reported earnings of $3.15 per share on $24.77 billion in revenue, compared with consensus estimates of $2.74 EPS and $23.74 billion in revenue. Despite the earnings beat, the stock is down about 2%, suggesting profit-taking or elevated investor expectations heading into the release.

Bank of America (BAC.US)

Bank of America also exceeded analyst expectations. The bank reported earnings of $1.21 per share, above the $1.13 consensus estimate, while revenue came in at $31.7 billion, surpassing expectations of $30.72 billion.

Wells Fargo (WFC.US)

Wells Fargo posted stronger-than-expected quarterly results, reporting earnings of $2.00 per share on $22.62 billion in revenue. Analysts had expected $1.72 EPS and $21.84 billion in revenue. Despite the earnings beat, the stock is down around 1%.

Merck (MRK.US)

Merck & Co. remains in focus after BMO Capital raised its price target to $142 from $135 while reiterating its Outperform rating. The upgrade is driven by stronger-than-expected adoption of Keytruda Qlex, the subcutaneous version of the company's blockbuster cancer therapy. BMO expects second-quarter sales of $363 million, compared with the market consensus of $334 million.

According to the brokerage, the key catalyst has been the introduction of a permanent U.S. J-code, which simplifies reimbursement for physicians and should accelerate adoption across the U.S. healthcare system. Although some hospitals have yet to integrate the treatment into their electronic medical record systems, BMO believes U.S. uptake will continue to outpace current market expectations.

Merck also received positive regulatory news. The FDA expanded the indication for its Capvaxive vaccine to include children and adolescents at elevated risk of pneumococcal disease, while the company also improved access to its HIV therapy IDVYNSO through U.S. state assistance programs.

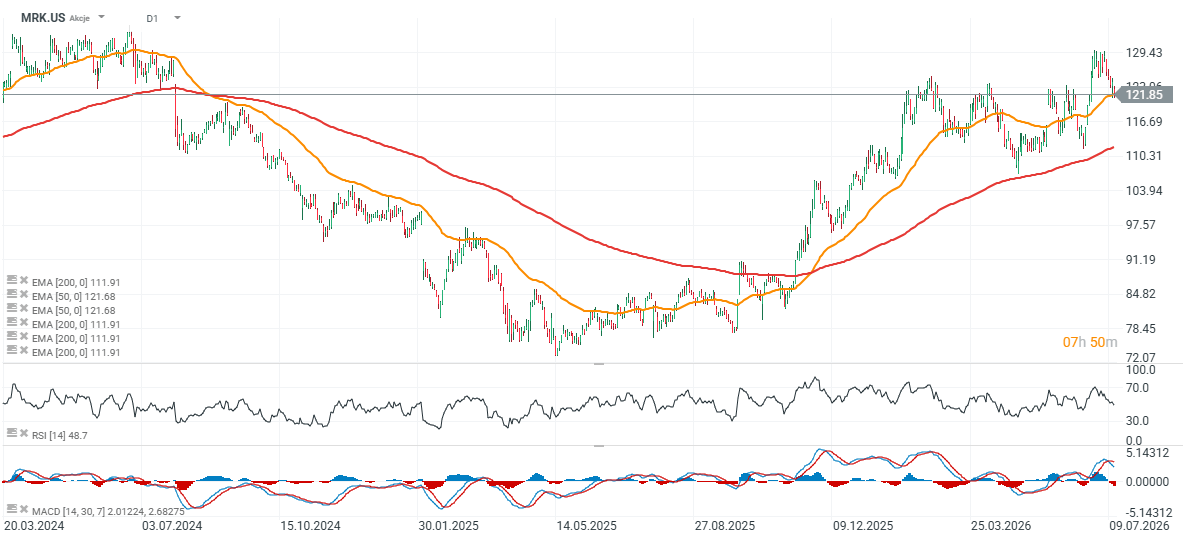

Merck shares (MRK.US)

Merck shares have retreated to their 50-day EMA (orange line) and are currently trading roughly 15% below BMO Capital's $142 price target.

Source: xStation5

Chart of the Day: USDJPY After Japan’s Intervention. The Exchange Rate Falls Below 160, but Pressure on the Yen Remains

Economic Calendar: JOLTS Report and Key U.S. Data Take Center Stage

Morning Wrap: Wall Street Returns to the Offensive as Palantir Fuels AI Optimism

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨