Market Sentiment and Macroeconomic Overview

Sentiment across US markets remains highly optimistic at Friday’s opening bell, with equities on track to register their longest streak of weekly gains since 2023. The buoyant mood is underpinned by an overall injection of liquidity and robust macroeconomic indicators. Investor risk appetite has been further whetted by the VIX volatility index sliding to its lowest level since early February , notwithstanding a brief technical uptick in early morning futures trading. Notably, there is considerable optimism heading into the weekend regarding geopolitical developments in the Middle East, as both sides report progress in diplomatic talks, driving a further retracement in crude oil prices.

Market momentum is also being fueled by an aggressive wave of corporate share buybacks and cash takeovers. According to data from EPFR, the aggregate value of these corporate equity purchases has already surpassed $1tn for 2026. Defying broader global trends, the S&P PMI data released on Thursday underscores the resilience of the US economy, particularly within the manufacturing sector. It is increasingly evident that artificial intelligence capital expenditure is beginning to manifest in tangible macroeconomic data.

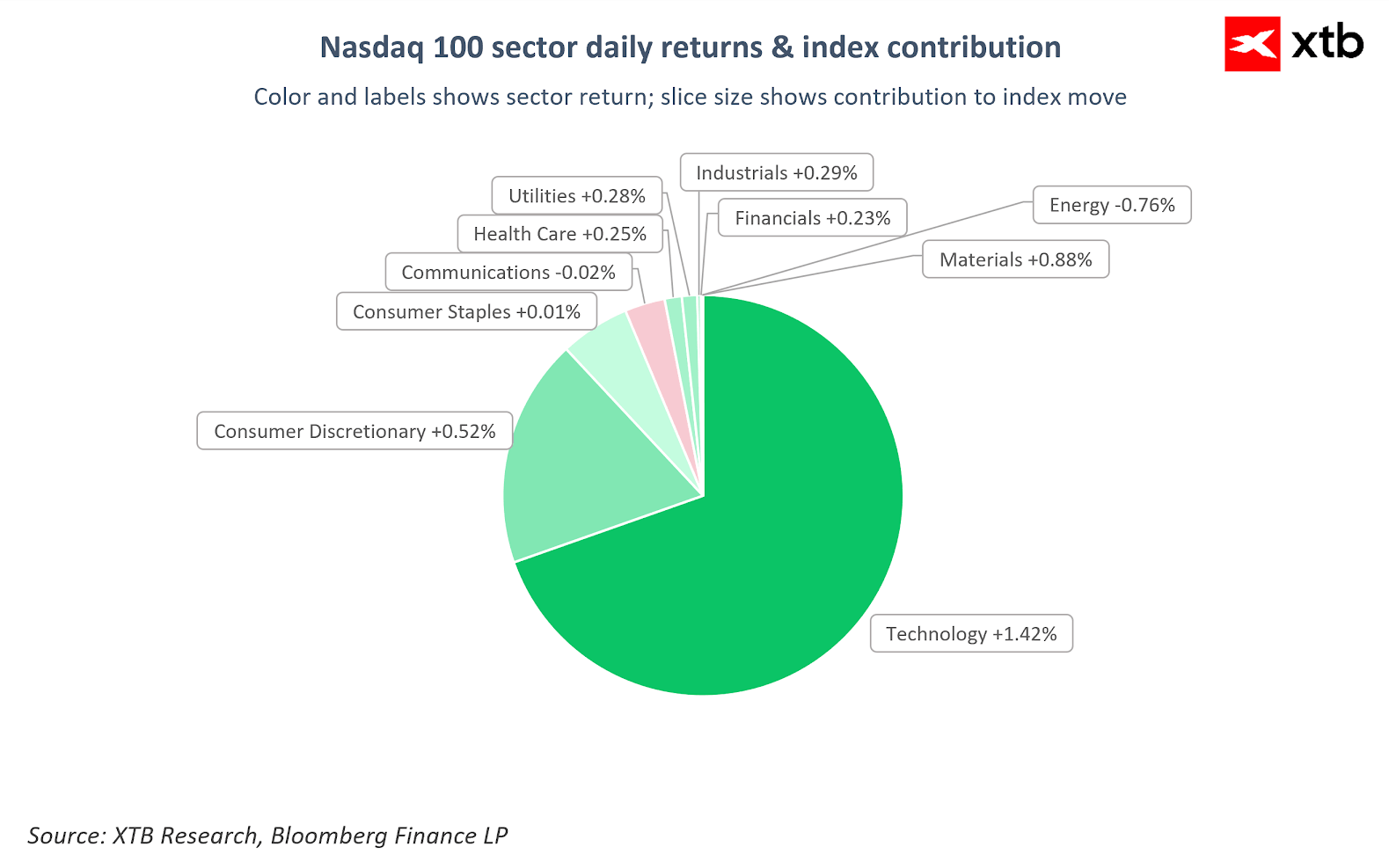

Unsurprisingly, given such a heavy concentration of technology heavyweights, the core sector of the Nasdaq 100 is leading the charge today. Source: Bloomberg Finance LP

Unsurprisingly, given such a heavy concentration of technology heavyweights, the core sector of the Nasdaq 100 is leading the charge today. Source: Bloomberg Finance LP

Nasdaq 100 (US100) Analysis

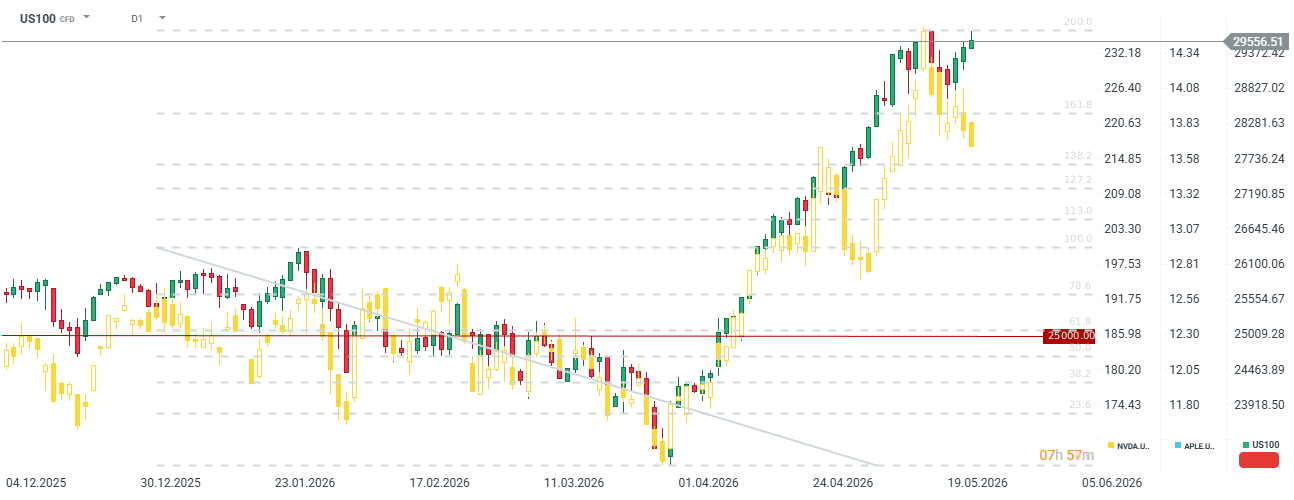

The S&P 500 (US500) and Nasdaq 100 (US100) gained approximately 0.5% at the opening of the cash session before slightly moderating their advances to the 0.3% to 0.4% range, leaving both indices just fractions of a percent below their all-time highs. As a reminder, US markets will be closed on Monday in observance of the Memorial Day holiday, with futures trading operating on an abbreviated schedule until 19:00 CET.

The Nasdaq 100 has pushed higher despite a pullback in Nvidia shares; while the chipmaker delivered stellar financial results, the announcement appears to have triggered a bout of profit-taking among investors. Conversely, mega-caps such as Apple and AMD are trading near peak levels, while peers like Microsoft and Meta Platforms remain well below their historical records, suggesting further headroom for the major averages to extend their gains.

Corporate Highlights

- IBM (+2.2%) and GlobalFoundries (+7.8%) advanced following news that the US government has awarded $2bn to develop quantum wafer facilities.

- Workday (WDAY) rose 6.8%—having surged up to 12% in pre-market trading —after its first-quarter financial results beat Wall Street expectations.

- Zoom Communications (ZM) climbed 11% on the back of better-than-expected earnings and an upgraded full-year outlook. The stock was further supported by KeyBanc upgrading its rating to Sector Weight.

- Take-Two Interactive (TTWO) slid 4.4%, reversing a pre-market gain of up to 5% , despite delivering solid quarterly figures and formally confirming a November 19 release date for Grand Theft Auto VI.

- IMAX Corp. (IMAX) surged nearly 17% following media reports that the large-screen cinema operator is exploring a potential sale and has approached various entertainment companies.

- Alcoa Corp. (AA) jumped 7% after UBS upgraded the aluminum producer to a Buy rating, citing a favorable outlook for aluminum prices driven by the ongoing war.

- Peloton (PTON) rallied 11% and Universal Technical Institute (UTI) gained 8% following the announcement that both stocks will be added to the S&P SmallCap 600 Index.

- US-listed Chinese stocks declined, with Alibaba (BABA) down 1.1% and Trip.com (TCOM) down 2.2%, weighed down by concerns over plans by China's securities regulator to penalize cross-border brokerages.

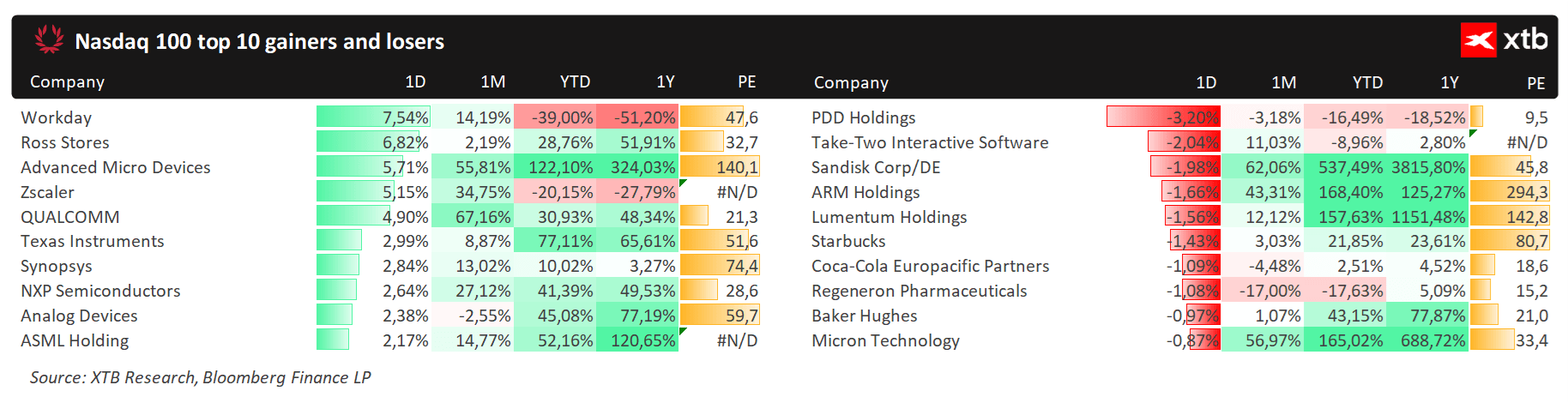

Nasdaq 100 leaders and laggards. Source: Bloomberg Finance LP

Nasdaq 100 leaders and laggards. Source: Bloomberg Finance LP

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Worse than the Dot-com bubble: IBM stock crash