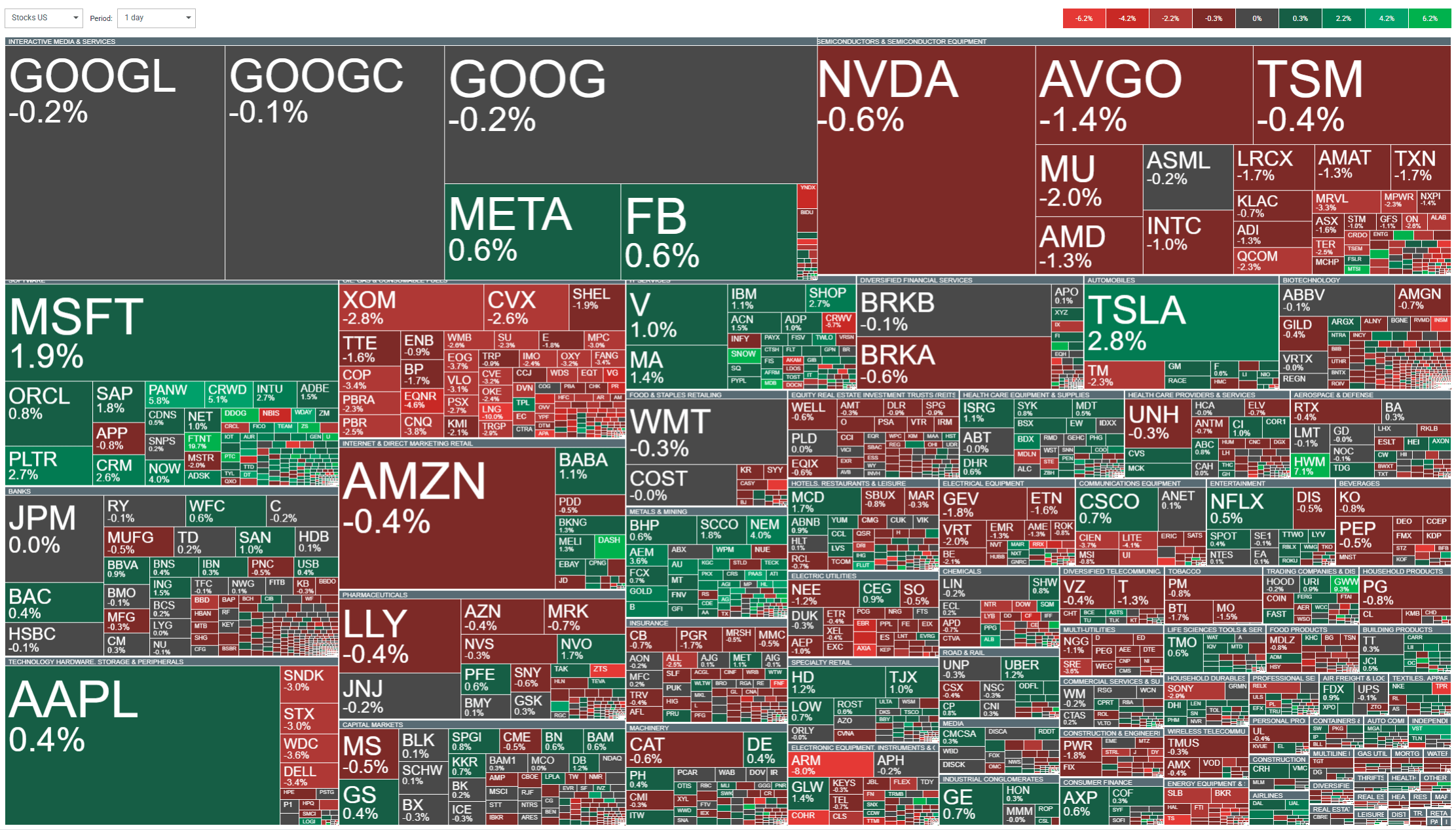

US futures are opening slightly higher — the S&P 500 is up by around 0.2%, the Nasdaq 100 is up 0.1%, and Dow Jones futures are up by around 0.3%, or approximately 133 points. The main driving force is growing optimism surrounding a possible truce between the US and Iran, which is pushing down oil prices and bond yields, and investors are interpreting this as a signal to buy shares.

Since the end of February, when the US–Iran conflict broke out, the markets have been reacting to every new development on the diplomatic front. Yesterday, Axios reported, citing sources close to the White House, that negotiators are close to signing a one-page, 14-point memorandum of understanding that would not only end the war but also create a framework for broader nuclear talks. The Iranian Foreign Ministry confirmed that Tehran is “analysing the proposal” from the US side. However, uncertainty remains high — key issues regarding uranium enrichment and the possible reopening of the Strait of Hormuz remain unresolved. Additionally, a meeting between Trump and Xi Jinping is scheduled for next week (14–15 May), at which tariffs, Taiwan and sanctions on Chinese chips are to be discussed.

Against this backdrop, precious metals are performing best — silver is surging by over 5% and gold is up by around 1%, as the market is betting on an end to the conflict and a resumption of the previous bullish trend. The technology sector, and chips in particular (the SOX index has risen by over 60% this year), remains the leader of the broader market. Energy and consumer companies are performing the worst — WTI crude is down by over 5%, dragging the oil sector down. Restaurant companies (Shake Shack -17%) and household appliance firms (Whirlpool -18%) are also performing poorly.

Source: xStation

Company information:

-

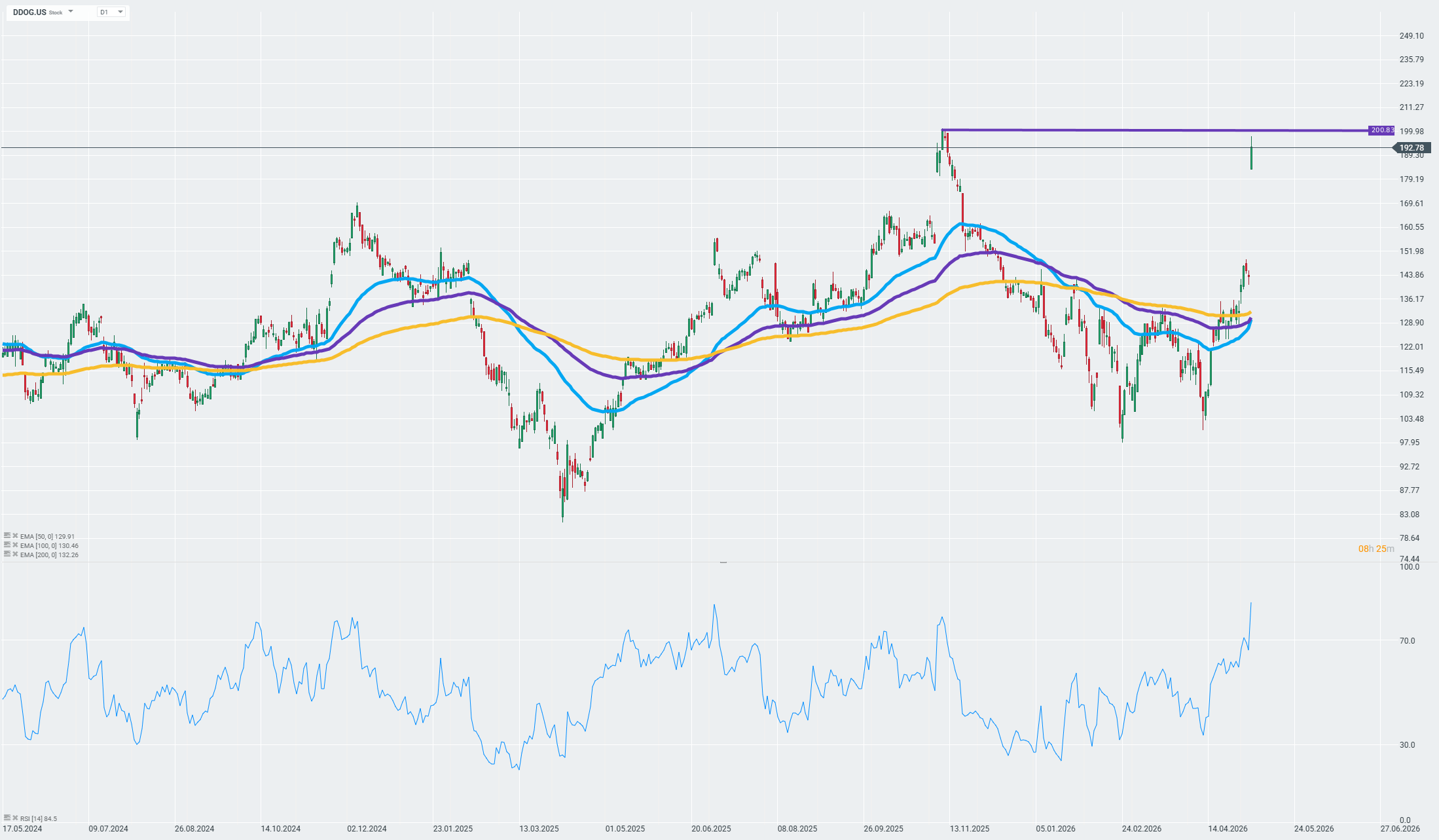

Datadog (DDOG) +22–24% in pre-market trading — The company surprised the market with both its results and its forecasts. Revenue rose by 32% y/y to $1.01 billion, beating the consensus estimate of $958 million — marking the first time the company has exceeded the $1 billion mark in a first quarter. Adjusted EPS came in at $0.60 against an expected $0.52 (+30% y/y), whilst the gross margin remained at 80.0%. The company ended the quarter with approximately 5,000 customers generating over $100,000 in ARR annually (+21% y/y), confirming its consistent expansion into the enterprise segment. Free cash flow reached $289 million with an FCF margin of 29%, whilst cash and cash equivalents on the balance sheet stand at $4.8 billion. An even stronger signal came from the guidance. For Q2, Datadog forecasts revenue of $1.07 billion (+29% y/y) with EPS of $0.57–$0.59, well above the consensus of $995 million and $0.52. For the full year 2026, the company raised its revenue forecast to $4.30 billion (vs. est. $4.10 billion) and EPS to $2.36–$2.44 (vs. est. $2.20). Three additional catalysts contributed to the results: FedRAMP High certification opening up the federal market, a strategic partnership with Sakana AI, and the appointment of Dominic Phillips to the board. CEO Olivier Pomel explicitly stated that AI drives — rather than cannibalises — demand for the Datadog platform, as customers need monitoring and security for their cloud and AI deployments.

Shares are surging at the start of trading and testing levels close to the highest seen since last November. Source: xStation

-

Fortinet (FTNT) +15% — The cybersecurity solutions provider has raised its full-year revenue forecast to $8.8–9.1 billion from the previous $8.4–8.6 billion, beating the consensus on both revenue and profit. The market is interpreting this as confirmation that corporate spending on IT security is resilient to macroeconomic uncertainty.

-

Whirlpool (WHR) -18% — The home appliance manufacturer has drastically cut its full-year forecasts: EPS is expected to be just $3.00–$3.50, down from the previous $6.00, and revenue around $15 billion, down from the previous $15.3–$15.6 billion. In its report, the company explicitly states that “the war in Iran led to a recessionary slump in US demand as consumer confidence plummeted in February and March.”

-

Shake Shack (SHAK) -17% — The burger chain reported an operating loss of $2.6 million in Q1; EPS came in at $0.00 against an expected $0.12, whilst revenue of $366.7 million fell short of the consensus estimate of $372 million.

-

ARM Holdings (ARM) -7.8% — ARM beat consensus estimates for total revenue, EPS and operating margin, but the market focused on the disappointment in the company’s key royalties segment. Total revenue rose by 20% y/y to $1.49 billion (est. $1.47 billion), whilst adjusted EPS came in at $0.60 against an expected $0.58. Licensing and other revenue was strong — a 29% y/y jump to $819 million (est. $775.6 million), signalling a robust pipeline of new chip projects, particularly in AI and data centres. The operating margin was also impressive at 49.1%, with operating income of $731 million (est. $696 million). However, royalties — the company’s most closely watched metric — amounted to just $671 million against a consensus of $693 million (+11% y/y). CEO Rene Haas admitted outright that the smartphone segment showed negative unit growth in the last quarter, and the situation in the mobile end market remains “slightly negative”. The problem is that smartphones and mobile application processors still account for around 46% of royalty revenue. Following the results, Goldman Sachs downgraded its recommendation to Sell, pointing to pressure in the royalty segment, a lack of clear competitive advantage in chip manufacturing, and a high valuation relative to comparable companies. Despite this, most of Wall Street remains bullish — Goldman and AlphaValue are the only banks with a sell recommendation, and ARM shares are still trading 117% higher than at the start of the year.

-

Agilon Health (AGL) +51% — The healthcare provider surprised the market by raising its full-year adjusted EBITDA forecast to a level well above zero, whilst the consensus had expected a loss. Q1 results beat expectations on both revenue and EBITDA, prompting at least two upgrades.

ASML sell-out: Dreams and rumors will not break the monopoly

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐