US equity markets are under clear pressure as the key deadline of Donald Trump’s ultimatum to Iran approaches (2:00 AM CET, April 8), with hopes for a deal fading after Iran announced it had cut off all indirect communication channels with the US in response to Trump’s threats. Escalating geopolitical tensions are weighing on equities while pushing oil prices higher, increasing uncertainty around the future direction of US policy. White House rhetoric is raising the risk of a forceful scenario, although markets still leave room for limited de-escalation.

- Trump has set an 8:00 PM ET deadline for a deal with Iran on reopening the Strait of Hormuz, warning that failure to reach an agreement could result in the destruction of Iran’s infrastructure.

- Recent comments from the US president suggest low odds of a breakthrough, although a narrow window for an alternative outcome remains.

- Media reports indicate that the US has carried out strikes on Iran’s Kharg Island, further intensifying tensions.

- Commodity markets are reacting sharply: WTI is trading above $116 (+3%+), while Brent is firmly above $110, pointing to a rising geopolitical risk premium.

- Analysts note that while a full agreement appears unlikely, a worst-case scenario involving large-scale attacks on civilian infrastructure may still be avoided.

- UBS has cut its S&P 500 year-end 2026 target to 7,500, citing rising uncertainty linked to the conflict and energy prices. The bank recommends a more cautious stance, particularly toward markets sensitive to energy shocks such as Europe and India.

- Macro data disappointed, with durable goods orders falling 1.4% month-over-month, below expectations and adding to negative sentiment.

- At the same time, ADP employment data showed an increase of 27k jobs (vs. 10k previously), suggesting the labor market is not overheating but also not a broad source of weakness—potentially reinforcing inflation risks.

- Despite the broader risk-off environment, select names such as Broadcom continue to outperform, supported by strong exposure to artificial intelligence and new contract wins.

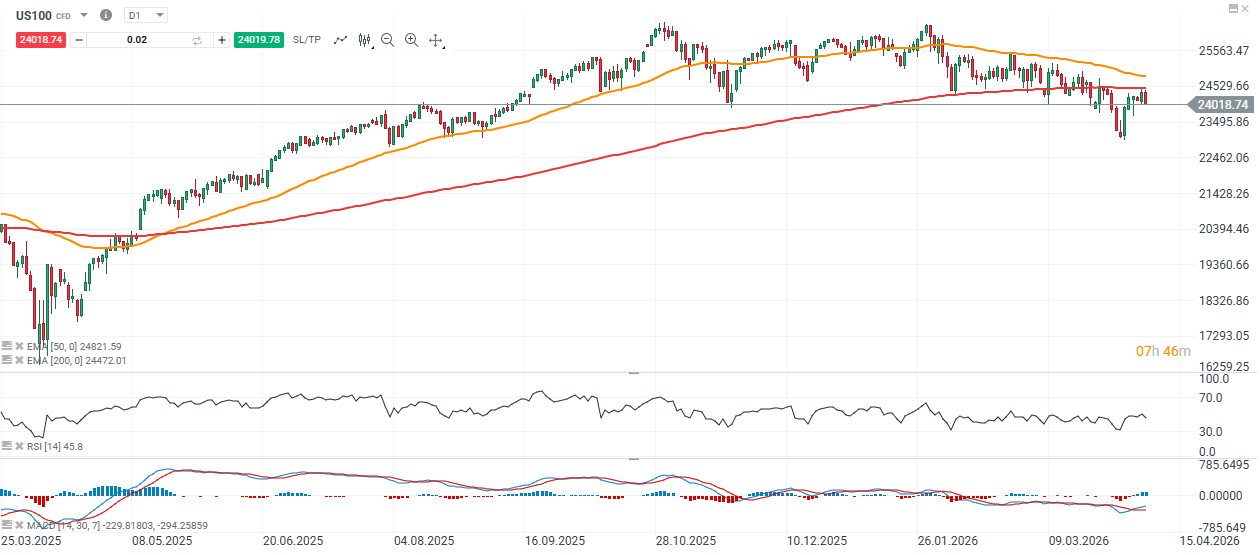

US100 chart (D1 timeframe)

Source: xStation5

Corporate news

- Universal Music Group (UMG) – shares jumped around 10% after Pershing Square proposed a €55.8bn ($64.4bn) acquisition, implying a 78% premium to the April 2 close. The cash-and-stock structure signals an activist-driven control bid and a significant re-rating via a control premium.

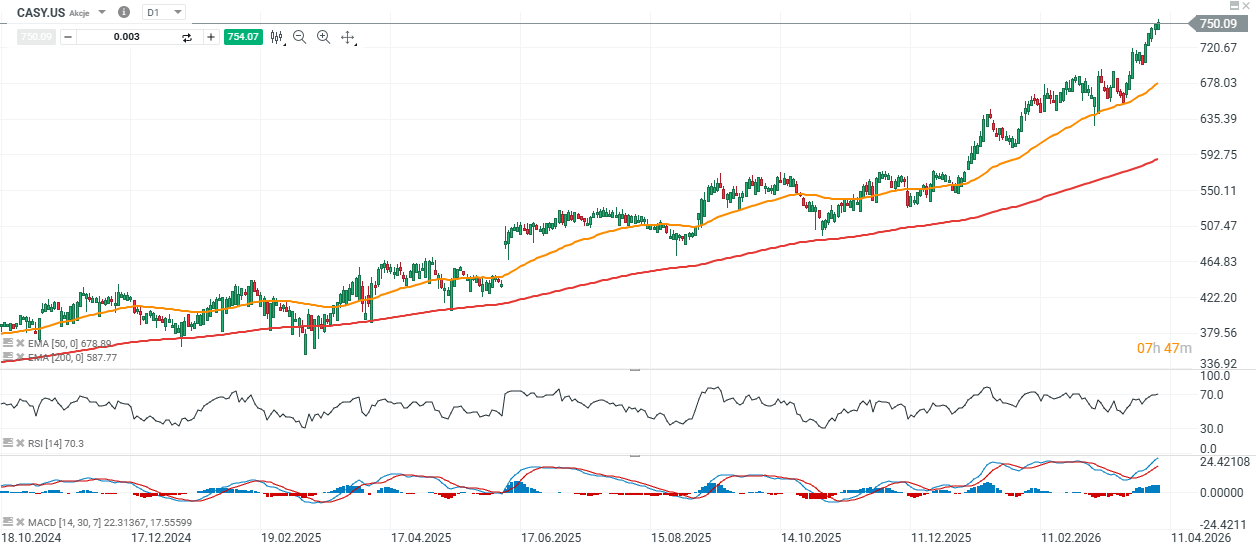

- Casey’s General Stores / Hologic – Casey’s - a US Midwest / Southwest chain of convenience stores, will replace Hologic in the S&P 500 ahead of Thursday’s open following Hologic’s acquisition by Blackstone and TPG. Casey’s shares moved modestly higher, while Hologic trading was halted as the deal was finalized and the company exits public markets.

Casey’s General Stores chart (D1 timeframe)

Source: xStation5

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

General Motors shares down despite solid earnings report 🚩