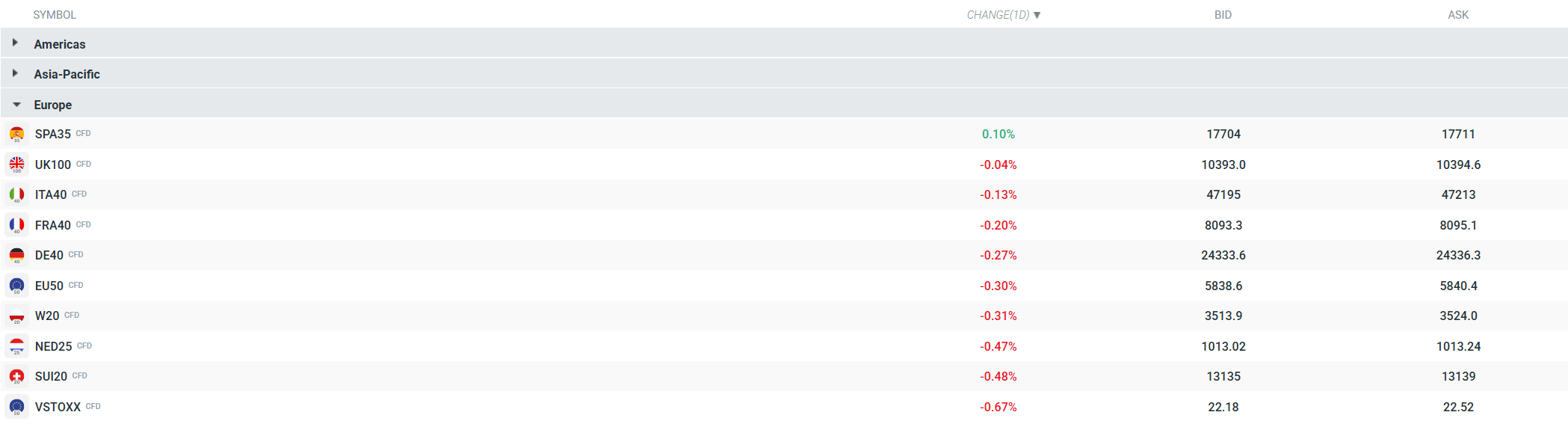

The first few minutes of Monday’s trading session on European markets are seeing moderate gains across most stock indices. Futures, however, are not reflecting this trend. The German DAX is down 0.27%, while the EU50 is down 0.3%. Investors continue to focus their attention on new reports regarding the conflict in the Middle East, which remain highly ambiguous. In the background, the Q1 earnings season is also becoming increasingly prominent, and it will be the main focus on Wednesday and Thursday.

Current prices of European contracts. Source: xStation

WHAT CAN WE EXPECT FROM TODAY'S SESSION AND THE REST OF THE WEEK?

• Trump is convening a Situation Room meeting with top national security advisors to assess the stalemate in negotiations with Iran and consider next steps. Any news coming out of this meeting could send shockwaves through the markets—particularly oil and futures contracts.

• Iran’s peace proposal is the main catalyst of the day – Trump has made it clear that he does not intend to lift sanctions until nuclear concessions are secured. The White House stated that it “will not negotiate through the press” and will accept only an agreement that permanently prevents Iran from obtaining nuclear weapons. The impasse continues.

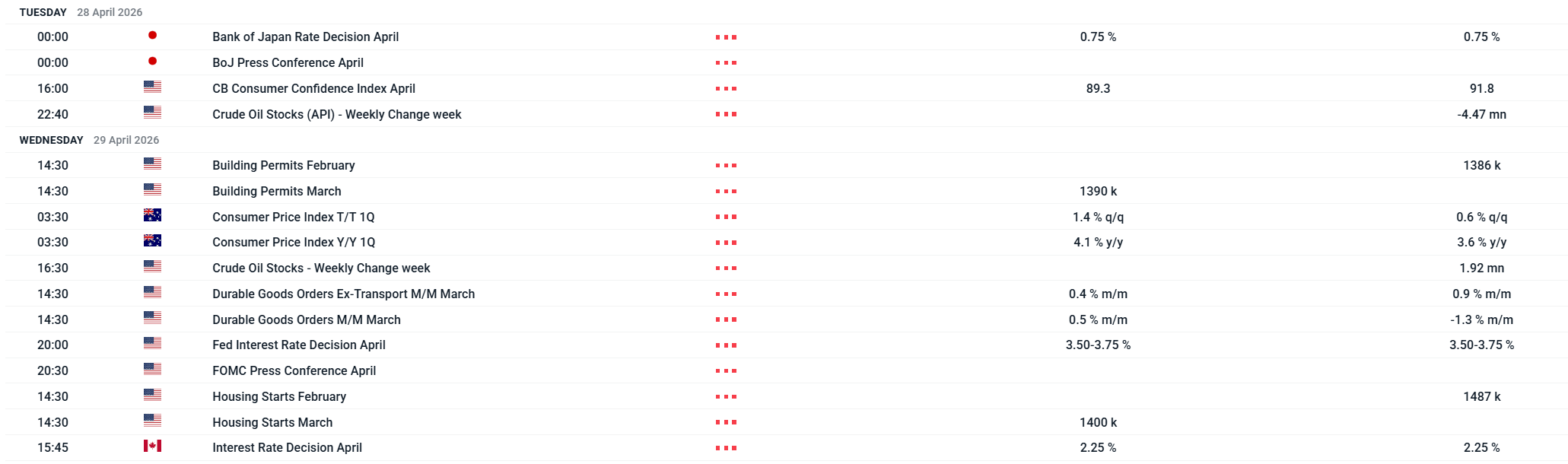

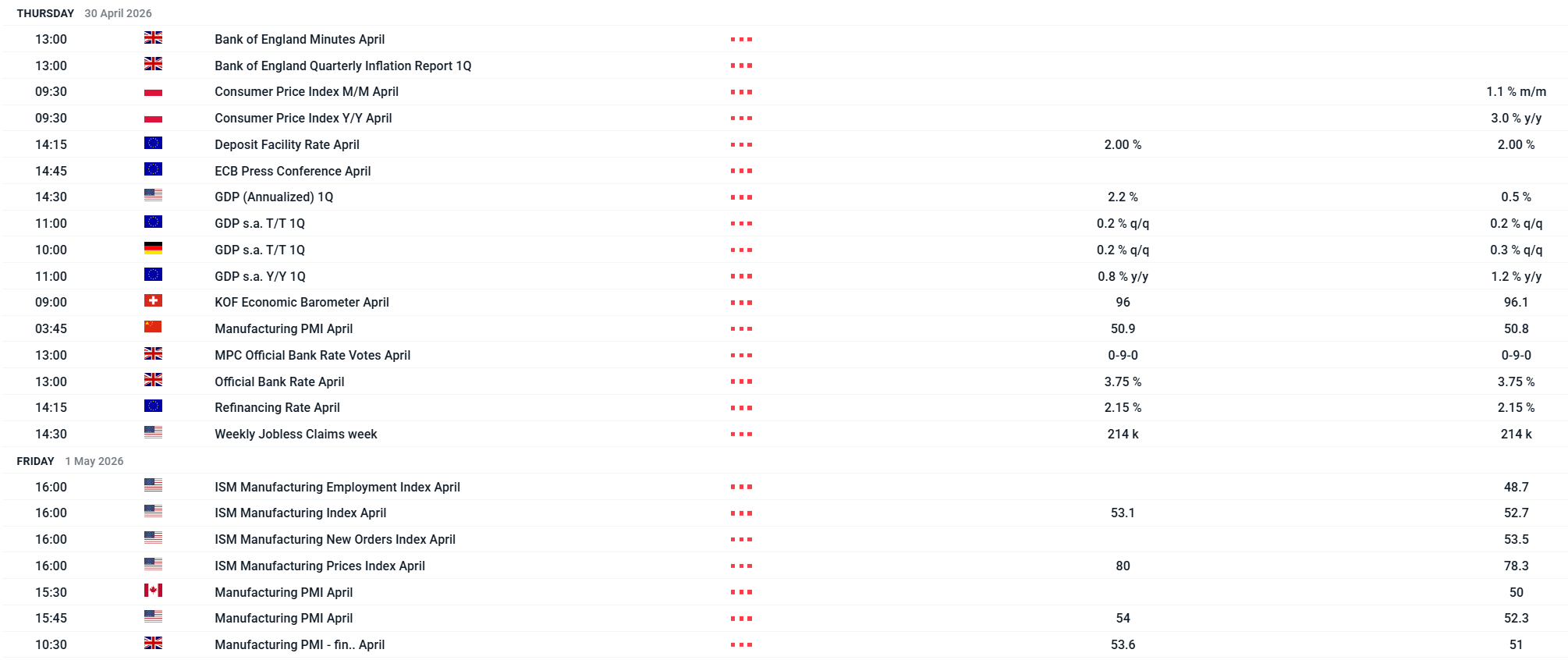

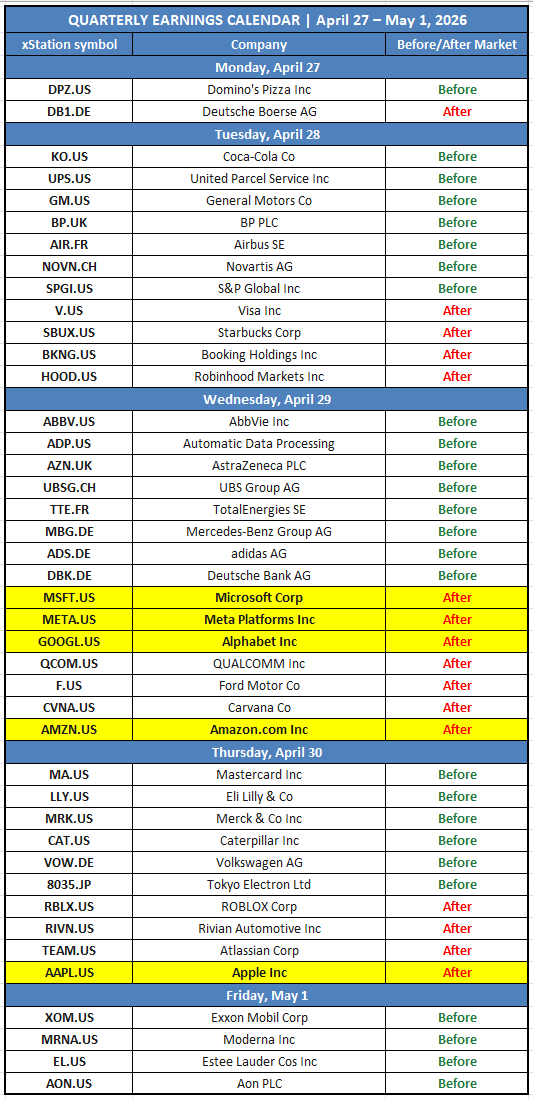

• A key week for macroeconomic and corporate news: Fed (Wednesday), ECB and BoE (Thursday), BoJ, BoC. Data: US PCE, GDP, ISM Manufacturing PMI. Five companies from the “Mag 7” are reporting earnings—any disappointment at current valuations could trigger a sharp correction from historic highs.

The most important macroeconomic reports scheduled for this week are listed below ⬇️

Source: XTB

Company Earnings Calendar

Source: XTB

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market