You can start investing with little money by using fractional shares, ETFs, and low-minimum brokerage accounts. Today, even £10–£50 can be enough to make a first investment and learn how markets work. The key is not starting big, but starting with structure, low costs, and realistic expectations. Over time, regular small contributions can become more powerful than waiting for the “perfect” large amount.

You can start investing with little money by using fractional shares, ETFs, and low-minimum brokerage accounts. Today, even £10–£50 can be enough to make a first investment and learn how markets work. The key is not starting big, but starting with structure, low costs, and realistic expectations. Over time, regular small contributions can become more powerful than waiting for the “perfect” large amount.

Key takeaways

- Small investments are accessible through tools such as fractional shares and ETFs, but access does not eliminate exposure to market risk.

- The effect of investing small amounts of money depends primarily on time, consistency, and cost control rather than the initial capital.

- Returns are uncertain and typically gradual, and small portfolios can be disproportionately affected by fees and emotional decision-making.

What Does "Investing with Little Money" Actually Mean?

Investing with little money - typically between £10 and £500 is now structurally accessible. Digital brokerages, fractional shares, low-cost ETFs and reduced account minimums have removed the barriers that once limited market participation to wealthy investors.

Small investors carry a structural advantage that institutional players lack: no requirement to deploy large capital, track benchmarks or hit quarterly targets. This creates flexibility in timing, position sizing and strategy selection - though it does not eliminate market risk.

Compound interest amplifies the value of starting early. Returns reinvested over time generate gains not only on original capital but on accumulated previous gains, making consistency and time horizon more important than starting amount.

❓ DID YOU KNOW

Small investors have more possibilities than ever before

For many years, investing with small amounts was difficult because investors often needed higher deposits, had to buy full shares, and paid transaction fees that made small purchases inefficient. Digital platforms, fractional shares, low-cost ETFs, and lower account minimums have changed that structure. This means that starting with £10 and £50 or £500 is now more practical than it used to be.

A smaller portfolio may also offer more flexibility, because it is easier to adjust position sizes or test different approaches without managing large capital commitments. However, easier access does not mean lower risk. Market volatility still affects every investor, regardless of portfolio size. The real advantage of modern tools is that they make it easier to start, learn, and build a structured investment habit over time.

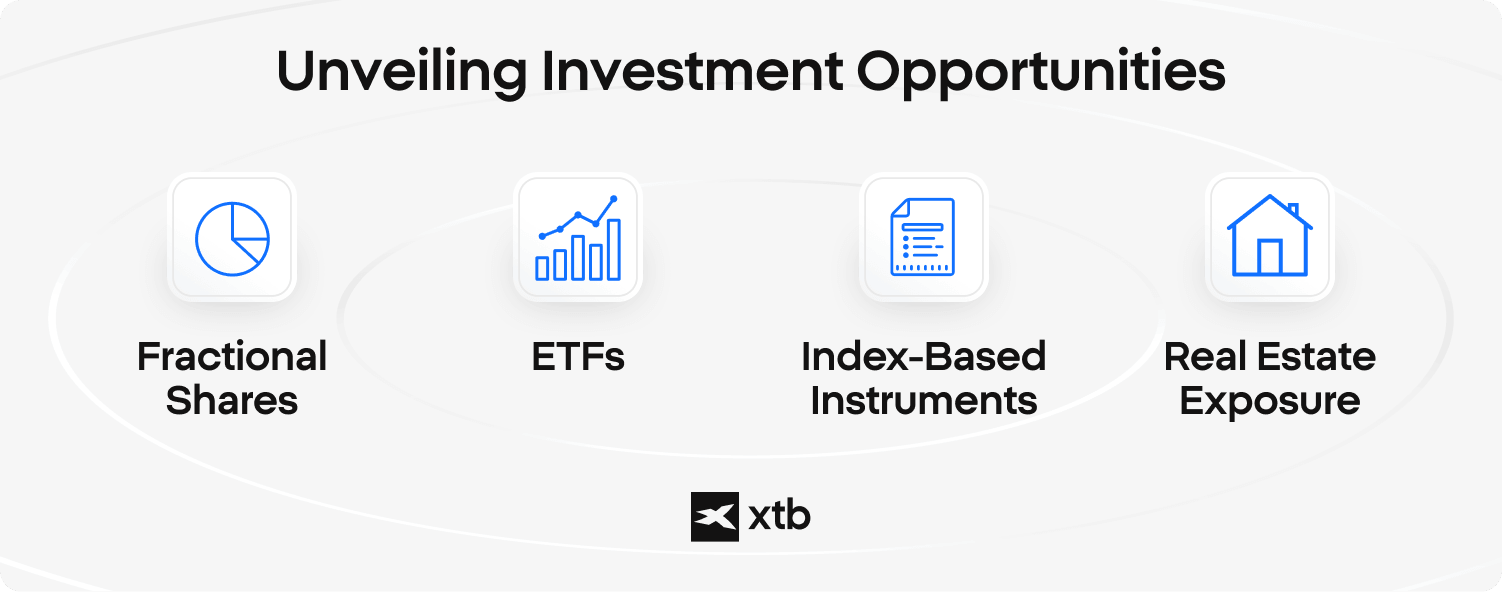

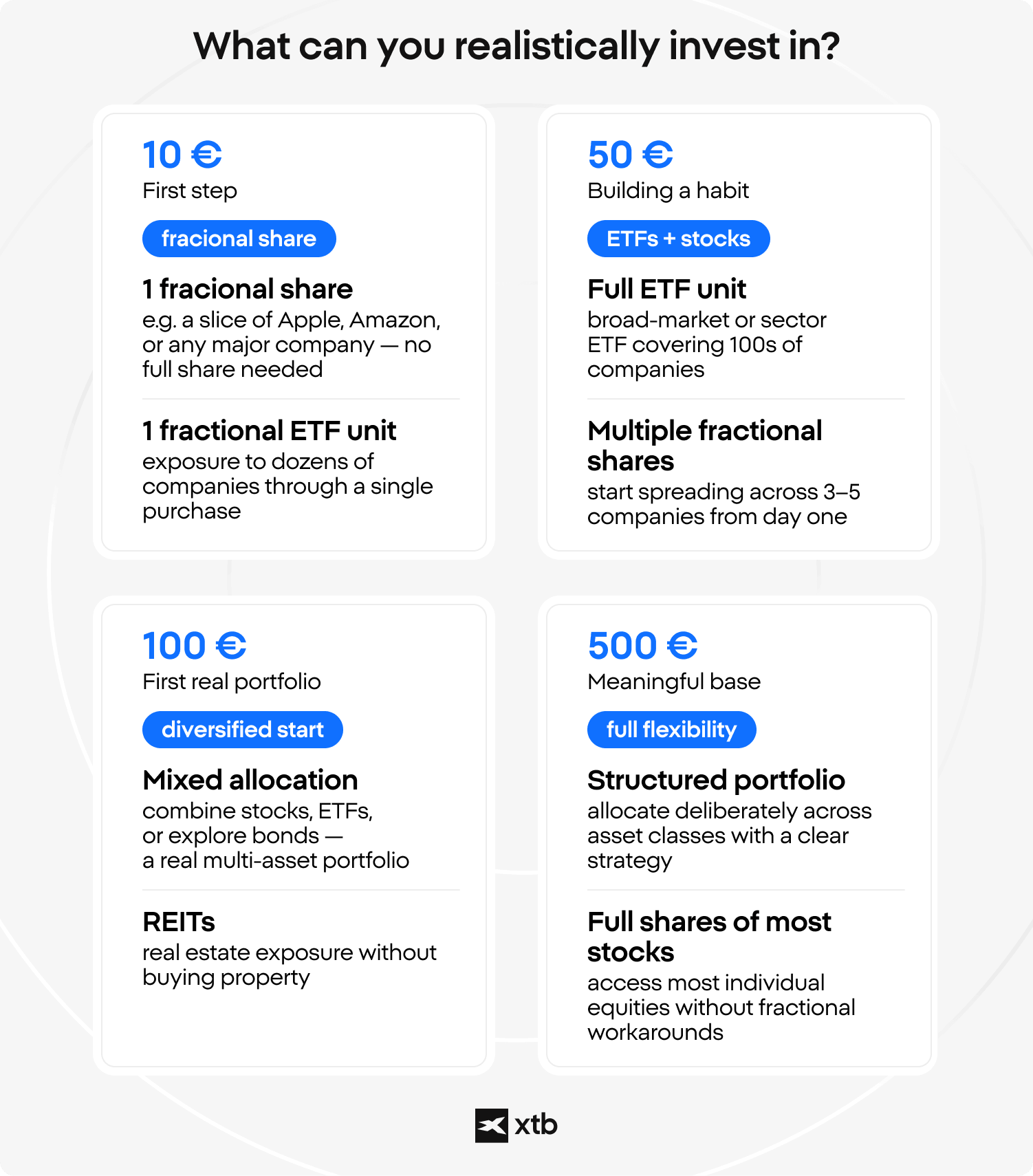

What Can You Realistically Invest In with a Small Budget?

A small budget can still provide access to several major asset classes, but the key is understanding how these instruments are structured. Modern investing is no longer limited to buying whole shares or large blocks of assets. Thanks to fractional shares, ETFs and low minimum deposits, even small amounts of capital can be used to gain market exposure. The most common options include:

Fractional shares - allow investors to buy a portion of a single stock, sometimes from as little as £1. This means that even expensive shares such as Tesla, Microsoft, Apple or Nvidia can be accessed with smaller amounts of money, without buying a full share.

ETFs - provide diversified exposure to a basket of assets, often with entry amounts around £10 - £50, depending on the platform and product structure. They can track broad markets, sectors, bonds, commodities or specific investment themes.

Index-based instruments - give exposure to wider market segments, such as large-cap U.S. stocks or global equity markets. In practice, many investors access them through ETFs that follow major indices.

Real estate exposure - learning how to invest in real estate with little money is crucial because property usually requires much more capital. Investors can gain indirect exposure through REITs or real estate ETFs, which trade like regular market instruments.

These are access formats, not recommendations. Each option has its own costs, volatility and risk profile, so the important question is not only what can be bought with a small budget, but how it fits into a broader investment plan.

What Results Are Realistic When Investing Small Amounts?

Realistic results from small investments are typically gradual and become more visible over longer periods rather than in the short term. When starting with limited capital, early changes in value may appear minimal because the base amount is small. This does not mean growth is absent, but rather that its scale is initially constrained by the size of the investment.

The relationship between time and accumulation plays a central role in shaping outcomes. When investments are made regularly, each contribution adds to the total capital, and any changes in value apply to a growing base. Over time, this creates a cumulative effect, although it does not follow a straight or predictable path.

📌 EXAMPLE

Regular contributions over time

An investor allocates a fixed amount each month into a diversified instrument. In the first years, the total value changes slowly because contributions dominate the portfolio size. As time passes, the accumulated capital becomes larger, and price changes begin to have a more noticeable effect on the overall value.

This illustrates how time influences the visibility of results, even when individual contributions remain small.

Market behavior introduces variability, which means results can differ significantly across periods. Financial markets do not grow at a constant rate, and periods of increases can be followed by stagnation or declines. This variability affects both large and small portfolios, but with smaller amounts, the psychological impact of slow progress may be more noticeable.

What Are the Biggest Risks When Investing Small Amounts?

Small investments face the same market risks as larger portfolios, but some risks can have a stronger proportional impact when the starting amount is limited. This makes cost control, diversification and discipline especially important.

- Fees and currency conversion costs can take a larger percentage of a small portfolio. Fixed transaction fees, spreads or FX charges may reduce returns more visibly when investing £50 or £100 than when investing larger sums.

- Emotional decisions can be more damaging than expected. Small investors may react quickly to short-term price moves, sell during volatility or chase popular stocks without a clear plan.

- Overconcentration in one asset is a common risk. Buying only one stock or one theme can expose the whole portfolio to company-specific or sector-specific shocks.

- Risk management matters at every size. A £100 portfolio and a £100,000 portfolio both require clear rules, realistic expectations and an understanding of possible losses.

⚠️ Caution

Why risks can matter more at a smaller scale

Costs can have a stronger impact on small portfolios because fixed fees, spreads and currency conversion charges represent a larger share of each investment. Limited capital can also increase concentration risk, as spreading money across many assets may not always be practical. Behavioral finance research by Daniel Kahneman and Amos Tversky also shows that investors are prone to loss aversion and short-term reactions, which can lead to inconsistent decisions when portfolio growth feels slow or unclear.

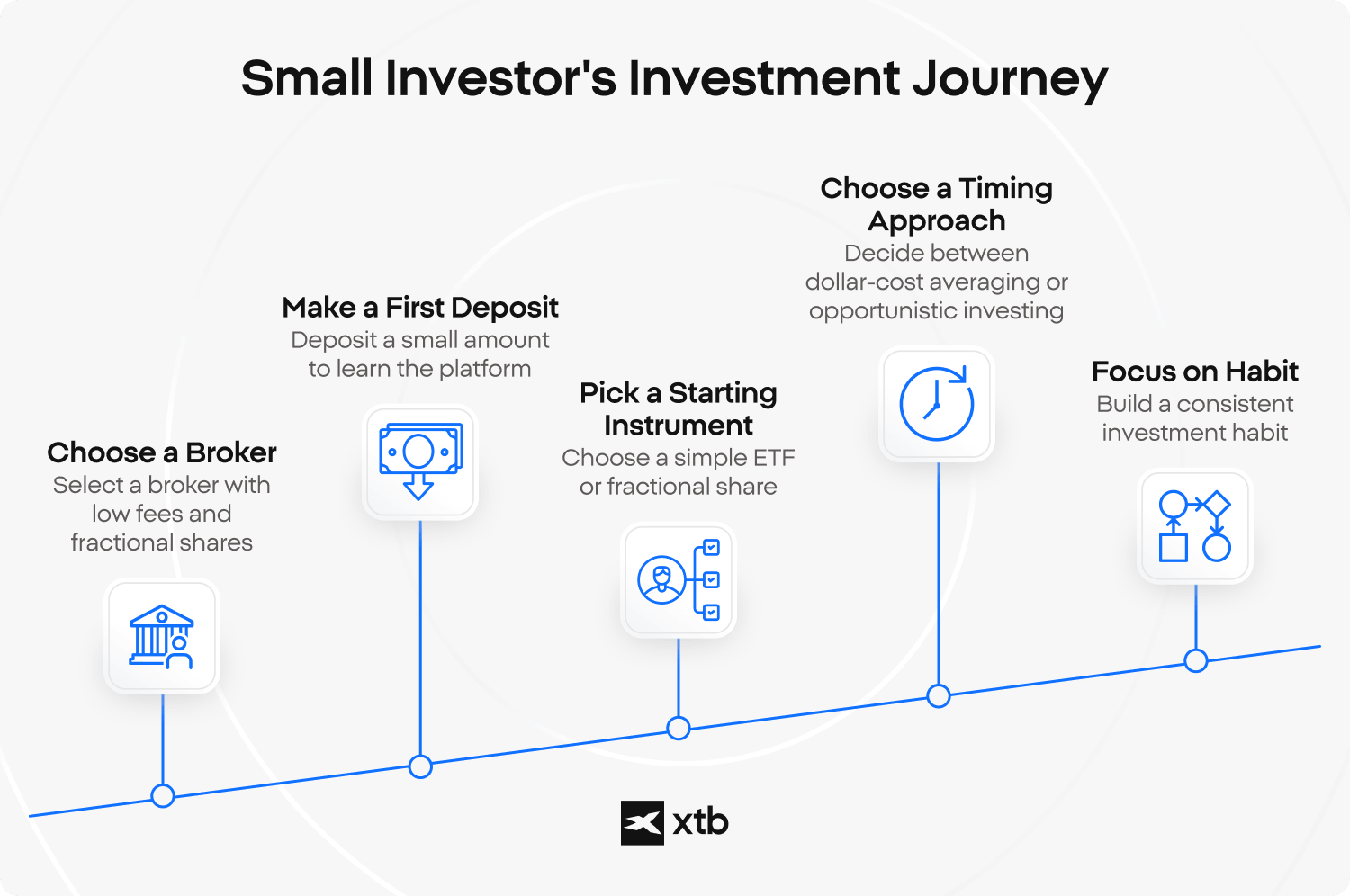

How Do You Actually Start - Step by Step?

Starting with a small amount is less about finding the perfect investment and more about building a repeatable process. The goal at the beginning is not optimization - it’s execution, understanding, and consistency.

Step one: choose a broker that fits small investing.

Focus on regulation, low fees, fractional shares, and access to ETFs. With small portfolios, cost structure matters more than features - even small fees can noticeably affect results over time.

Step two: make a first deposit you won’t overthink.

This can be £10, £50 or £100. The purpose is not performance, but learning how the platform works - placing orders, understanding spreads, and seeing how prices move.

Step three: pick a simple starting instrument.

Many investors begin with broad ETFs for diversification, while others use fractional shares to gain exposure to companies like Apple, Microsoft or Nvidia. At this stage, simplicity is more important than precision.

Step four: choose your approach to timing.

Some investors invest regularly regardless of market conditions (dollar-cost averaging), while others wait for specific opportunities. Both approaches are valid - what matters is consistency and understanding the trade-offs.

Step five: focus on habit, not scale.

From a behavioral standpoint, it is easier to stay consistent with £10 than to commit £1,000 at once. Building the habit early often matters more than the size of the first investment.

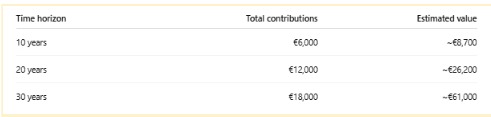

How Can Small, Regular Investments Grow Over Time?

Small amounts can grow into meaningful capital when combined with time and consistency. This is the effect of compound interest: returns generate additional returns, creating a snowball-like dynamic over time. For example, investing 50 EUR per month at an illustrative 7% annual return would result in approximately:

This is not a forecast, but a simplified illustration. Markets are volatile and returns are not linear. However, it highlights a key shift in perspective: long-term outcomes are driven less by the size of individual contributions and more by consistency over time. Remember also that the future remains uncertain and investing success is not guaranteed nor in the short and long term.

This is not a forecast, but a simplified illustration. Markets are volatile and returns are not linear. However, it highlights a key shift in perspective: long-term outcomes are driven less by the size of individual contributions and more by consistency over time. Remember also that the future remains uncertain and investing success is not guaranteed nor in the short and long term.

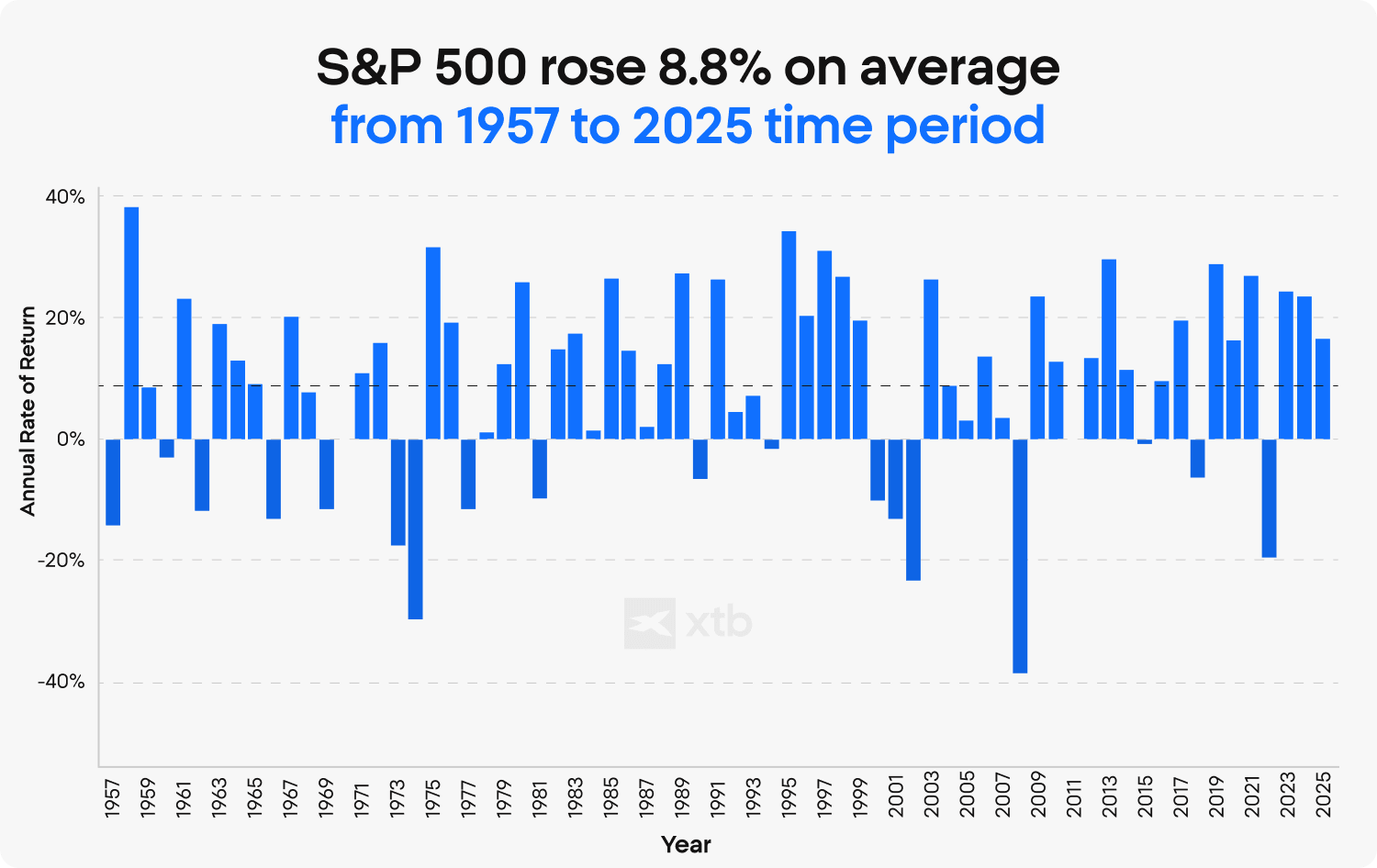

As we can see above, the annual average S&P 500 performance (ex-dividends) from 1957 to 2025 was 8.8% which makes our 7% illustrative return even more conservative. What’s worth noting is that almost never the index reached the ‘average’ yearly performance - numbers were usually much higher, but sometimes deeply negative (1974,1978,2022). The future remains uncertain and historical performance does not guarantee financial success. Source: XTB Research, Macrobond

FAQ

There is no universal minimum. On many modern platforms, investing can begin with as little as €1–€10 through fractional shares or low-cost ETFs. The more relevant question is not the starting amount, but whether contributions can be maintained consistently over time, since long-term outcomes depend more on regularity than on the initial deposit.

The process is straightforward but requires structure. First, open a regulated brokerage account with transparent fees. Second, fund it with a small amount you are comfortable using for learning. Third, choose a simple instrument such as a broad market ETF or a fractional share of a large company. Finally, observe how the investment behaves and build from there. The first transactions are often more educational than financially significant.

Yes. Market risk does not decrease with smaller capital. Prices can move up or down regardless of position size, meaning the percentage risk remains the same. What changes is only the scale of gains and losses in absolute terms. Small investing reduces exposure, not uncertainty.

Regular investing reduces reliance on timing the market. By investing fixed amounts over time, investors spread entry points across different market conditions. This approach, often called dollar-cost averaging, can make the process more predictable and easier to maintain, especially in volatile environments.

Saving typically involves low-risk accounts with stable value but limited returns. Investing, in contrast, exposes money to market fluctuations in exchange for potential growth. The two serve different roles: saving is about capital preservation, while investing is about participating in long-term market performance.

Direct property investment usually requires significant capital. However, exposure to real estate markets is possible through REITs (Real Estate Investment Trusts) or real estate ETFs, which allow investors to participate in property-related income and valuation changes without owning physical assets.

Investing is always risky, even for experienced investors. Lack of experience can increase the likelihood of poor decisions - that’s why study markets and exploring the investment-related knowledge is so important for investors: both experienced and inexperienced. The future remains unknown, but learning basic concepts such as diversification, volatility, and psychology can reduce avoidable mistakes.

Time is a key variable in investing. Starting early allows more time for compound growth, where returns generate additional returns over multiple periods. Even small contributions can accumulate meaningfully if they are sustained over long horizons.

Fees have a proportionally larger impact on smaller portfolios. Fixed transaction costs, spreads, or currency conversion charges can reduce returns more noticeably when capital is limited. Understanding the cost structure is therefore essential before making frequent or small transactions.

Consistency often comes from simplicity. Many investors use fixed schedules, such as monthly contributions, or automated investment plans. Reducing the number of decisions can make the process more manageable and help maintain discipline over time.

Best ETFs to Look Out For

Building Balance: How to Diversify Your Portfolio with XTB

The Importance of Maintaining a Presence in the Financial Markets All Year Round

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.